Better serving your members’ needs by using indirect auto lending research

There’s good news and bad news about auto sales and auto lending.

The good news first, 2014 should be another strong year for auto sales. Black Book Lender Solutions has projected an increase in new auto sales growth of up to 3%. More sales growth means more lending opportunities, and therefore more loan revenue. Now the bad news – the auto lending market is increasingly competitive. Both banks and captive finance companies have grown very aggressive and this trend is only expected to increase in 2014.

According to Informa Research Services’ indirect auto lending research, banks and captive finance companies combined captured nearly 90% of all new auto loan originations in 2013. These two sources combined, acquired 80% of the total auto lending originations, both new and used, in the same year. Banks alone were responsible for over 50% of both new and used auto loan originations in 2013. Credit unions captured less than 12% of new auto financing and only 19% of total auto loan originations last year.

Given the expectation that banks and captive finance companies will continue to act aggressively in this segment, credit unions that want to grow their auto lending revenue must prepare to combat this threat. Credit unions that approach 2014 auto lending with the same strategies as the past are likely to experience a loss of market share and lower auto lending revenues.

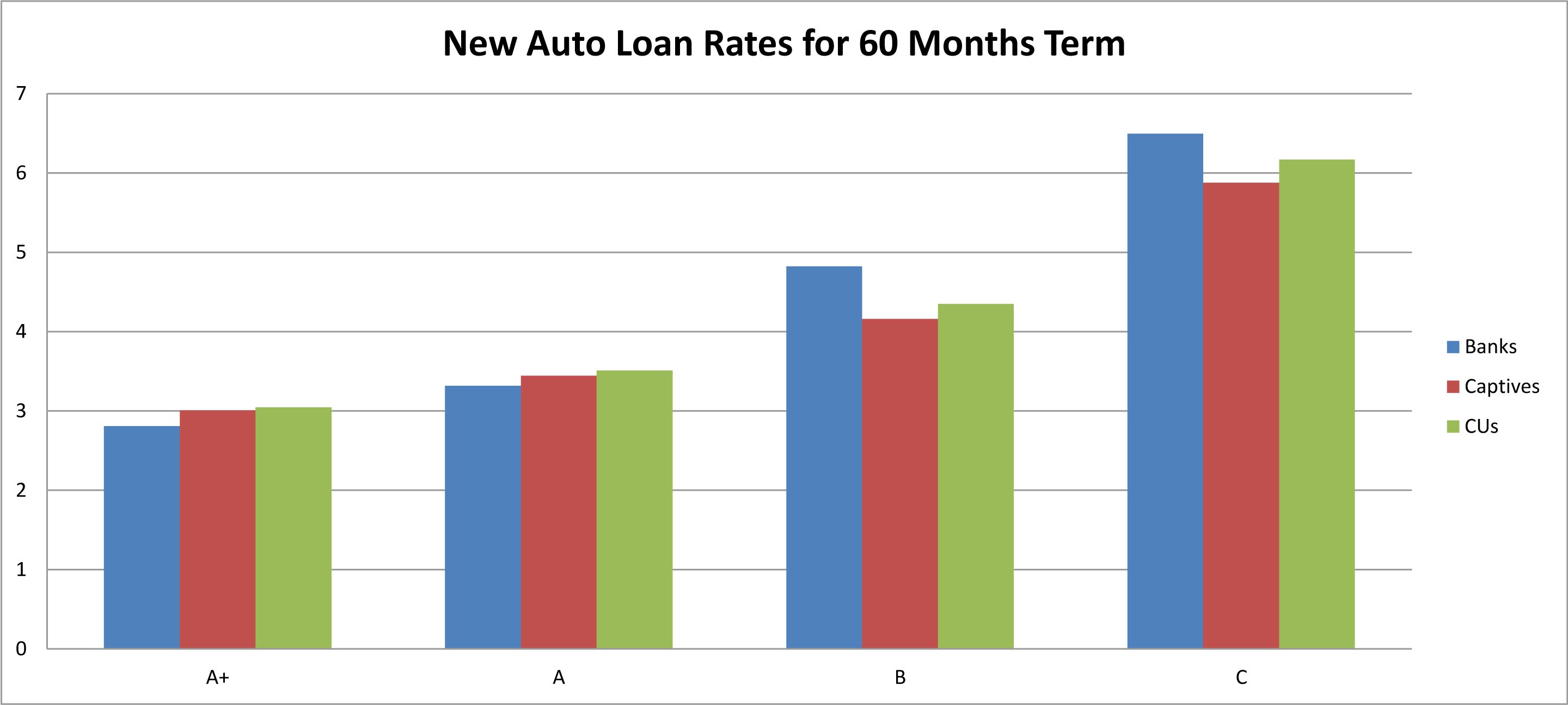

As an example of the hard-line tactics taken by banks in 2013, Informa’s research shows on the accompanying chart (see Figure 1) how banks have offered lower new auto loan rates for 60 month terms on the top two credit tiers. Captive finance companies offered the lowest rates on the lesser credit tiers. The result is that credit unions did not match the offers provided by their competition in any of these credit tiers and therefore did not provide the best auto lending product choices for their members.

Another challenge that the auto lending industry has to face is the impact of the CFPB (Consumer Financial Protection Bureau). The CFPB released a bulletin in March of 2013, explaining its position very clearly regarding rate participation/mark-up programs of indirect lenders. That is, lenders that offer such programs probably are liable under ECOA and Regulation B if such practices result in disparities on a prohibited basis – even if the lender had no reasonable notice of the act, policy, or practice that constituted the violation. According to the CFPB bulletin, the CFPB recommends indirect auto lenders take steps to ensure that they are operating in compliance with fair lending laws as applied to dealer mark-up and compensation policies.

These steps may include, but are not limited to:

- Imposing controls on dealer mark-up, or otherwise revising dealer mark-up policies

- Monitoring and addressing the effects of mark-up policies as part of a robust fair lending compliance program

- Eliminating dealer discretion to mark-up buy rates, and fairly compensating dealers using a different mechanism that does not result in discrimination, such as flat fees per transaction

Notably, Informa’s research shows that banks and captives continue to offer dealer participation/mark-up programs by making changes to their dealer compensation policies despite the CFPB recommendation to eliminate dealer discretion to mark-up the rates.

2014 is going to be a good year for new auto sales. The question is how do you make it a great year for your credit union’s auto lending efforts? To capture a greater share of the auto lending market in 2014, credit unions will need to price more aggressively and market proactively.

Getting more aggressive with your pricing

Both for direct and indirect auto lenders, the key to success is to truly understand what your competing auto lenders are offering. You should understand both their rates and their dealer compensation programs (in the case of indirect lenders). Knowing your competition’s current offerings allows you to price more aggressively and also market your direct auto lending services proactively.

Marketing Proactively

For auto loans through direct channels, reaching members shopping for autos with the right offer before they arrive at the car dealer is a large part of successfully originating their auto loans. Communicating a competitive offer to your members early and often allows you to sell other relationship enhancements beyond just rate. Once your members have arrived at the car dealer, without prior engagement, it is far more likely they will acquire financing through the dealer finance department.

As a credit union, you want to provide your members with the best financial products and services possible. Understanding your market and what the key players are offering enables you to better serve your members in the area of auto lending. You win too! With a better understanding of your market, you will strengthen your member relationships as you price for more profitability.