Credit unions play a pivotal role in today’s dynamic and competitive financial landscape, offering attractive rates and personalized services. As consumer credit behaviors change in a fluctuating economy, the market must balance risk management with growth opportunities. Understanding emerging trends across the financial services landscape is paramount for credit unions to thrive.

Experian’s latest report* offers valuable insights into the consumer credit landscape and highlights how credit unions compare to other financial institutions in three key areas: delinquency trends, origination volumes and VantageScore® distribution across auto loans, unsecured personal loans and unsecured credit cards.

Delinquency trends across loan types

Auto loans

Delinquency levels have gradually increased since mid-2022 for credit unions. Smaller credit unions (<$10 billion in assets) saw a 12% YoY increase in 30 DPD delinquencies, while larger institutions (>$10 billion in assets) experienced a 6% rise. Fintech lenders experienced significantly higher delinquency rates compared to credit unions, with regional banks showing moderate but steady increases.

Unsecured personal loans

Delinquencies have risen across the board over the past two years for unsecured personal loans. Smaller credit unions maintained lower 30 DPD delinquencies than fintech lenders, while larger credit unions saw a sharp uptick in early 2023, leveling off in 2024. Regional banks experienced a 22% decrease in early-stage delinquencies from January to May 2024, stabilizing thereafter.

Unsecured credit cards

Credit unions experienced a slight uptick in 30 and 90-120 DPD rates in the second half of 2024, with 60 DPD rates normalizing. Fintech lenders' delinquency rates began to stabilize towards the end of 2024, with regional banks showing a moderate increase.

Market opportunities for credit unions

The steady upward trend in 30 DPD delinquencies across all loan types underscores the importance of early intervention. Credit unions should consider incorporating advanced analytics, including expanded datasets, predictive modeling, and machine learning, into their portfolio management and collections strategies to proactively monitor and mitigate risk.

Origination volume by product type

Auto loans

Smaller credit unions consistently maintained the largest share of auto loan originations, peaking at over $1.7 billion in July 2022. Despite a slight 5% dip between January and March 2024, they sustained steady loan activity throughout the year. Although larger credit unions held noticeably higher market share than regional banks from mid-2022 to early 2024, regional banks began outpacing larger credit unions thereafter.

Unsecured personal loans

Originations fell subtly YoY for most lenders in 2024. Since 2022, Fintech lenders consistently held the most significant share, while both smaller and larger credit unions outpaced regional banks.

Unsecured credit cards

All lenders experienced a YoY decline in origination volume, with minor fluctuations. Like unsecured personal loans, fintech lenders saw the highest origination volumes compared to the other groups. Credit unions and regional banks all maintained similar volumes YoY.

Market opportunities for credit unions

Credit unions, particularly smaller ones, have made notable gains in auto loan originations, a sign that members value their competitive rates and personalized service. To sustain this momentum, credit unions could benefit from enhancing their marketing and retention strategies. Tactics like automating the lending process and using data-driven insights to deliver targeted offers can help boost efficiency and engagement.

While unsecured personal loan and credit card originations have remained steady, there’s untapped potential in these areas. By modernizing underwriting practices, such as incorporating alternative credit data, credit unions can better identify creditworthy borrowers who might be overlooked by traditional models, opening the door to new growth opportunities.

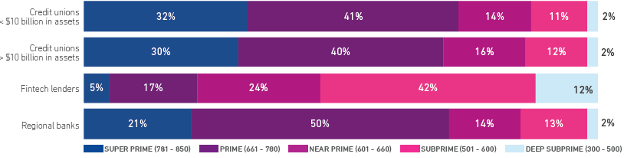

VantageScore distribution

In the current lending landscape, credit unions and regional banks continue to prioritize lower-risk borrowers, particularly in auto loans and credit cards. Their auto portfolios are largely composed of super prime and prime borrowers, reflecting a conservative lending strategy. In contrast, fintech lenders are taking on more risk, with over half of their auto loan portfolios consisting of subprime and deep subprime borrowers.

For unsecured personal loans, all lender types, including credit unions, regional banks, and fintechs, show a broader distribution across prime, near prime, and subprime categories, indicating a more inclusive approach.

When it comes to unsecured credit cards, credit unions again lead in conservative lending, with 74% of their portfolios in the super prime and prime tiers. Fintechs, however, maintain a higher share of subprime borrowers, while regional banks align more closely with credit unions in targeting lower-risk segments.

Market opportunities for credit unions

Smaller credit unions have maintained the largest share of auto loan originations, indicating that members are increasingly seeking out these institutions for their competitive rates and personalized services. To sustain this volume, credit unions might consider enhancing their marketing and retention strategies, which could include looking for opportunities for automation to increase efficiency or using data-rich insights to create highly targeted offers.

While unsecured personal loan and credit card originations have remained relatively stable for credit unions, there is potential for growth. By leveling up underwriting strategies, credit unions can attract more borrowers in these areas. For instance, incorporating alternative credit data alongside traditional credit data can help identify creditworthy consumers who might be overlooked by other lenders.

Navigating 2025 and beyond

As credit unions navigate 2025, notably in a shrinking environment, leveraging the right data and solutions will be crucial for sustainable growth and risk reduction. Key strategies include:

- Comprehensive data sources: Utilize fresh and accurate data for marketing and portfolio management. Having a holistic view of prospective and existing members better enables personalized offers and early identification of payment stress.

- Advanced analytics and machine learning: Employ predictive analytics and machine learning models to uncover behavior patterns of your members to better anticipate potential risks.

- Accelerated decisioning: Streamline operations and enhance member experiences with automation, from loan decisioning to digital lending.

- Credit education: Engage Gen Z consumers with comprehensive credit education resources, which can serve as a spring board for building valuable and long-lasting relationships.

- Fraud management: Mitigate fraud with robust identity protection and fraud prevention solutions, including behavioral biometrics and advanced analytics.

By adopting these strategies, credit unions can position themselves for success in 2025 and beyond, ensuring they remain competitive and responsive to member needs. For a deeper dive into these insights, access the full report.

*This report was created using Experian data from January 2022 to October 2024. Note: the term “all lenders” in this article specifically refers to the four groups analyzed (smaller credit unions, larger credit unions, fintech lenders and regional banks). This article defines smaller credit unions as institutions with less than $10 billion in assets and larger credit unions as those with more than $10 billion in assets.