The lending environment for credit unions in 2025 has been defined by rapid change, competitive pressures, and evolving member needs.

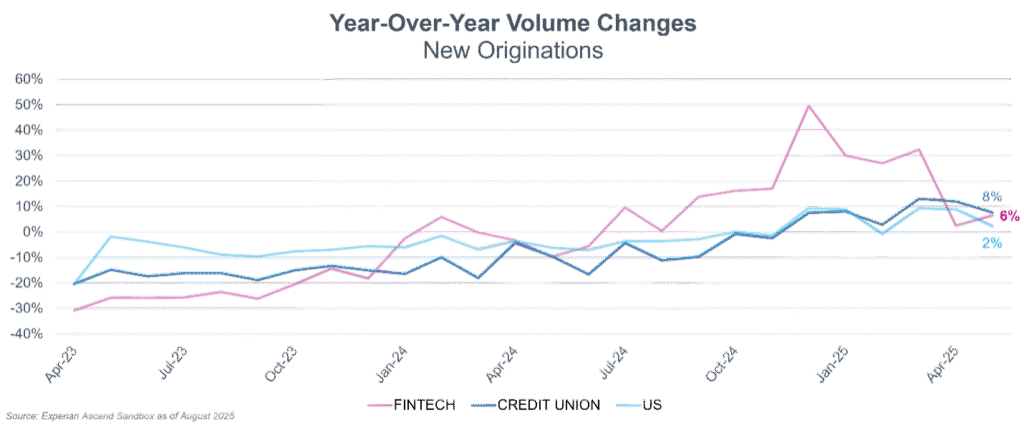

Over the past few years, credit union loan originations have experienced significant volatility. Early 2022 saw unusually high origination volumes, followed by a notable 16% year-over-year decline in August 2023. Despite this dip, August marked the highest origination volume in the period, suggesting that the market was recalibrating after a surge. By late 2024 and into 2025, originations stabilized, with consistent year-over-year growth since December 2024. This stabilization is a positive sign for credit unions, indicating that lending activity is returning to more predictable patterns after a period of disruption.

Several factors are influencing the recent origination trends. Consumer spending was higher in 2024 than what has been seen so far in 2025, although a seasonal dip in lending this year mirrored previous years. Post-Q1 caution remains, yet the overall trajectory is upward. Fintech companies have become increasingly aggressive in the lending space, focusing on secured cards and unsecured personal loans, and expanding into auto financing. Their marketing budgets are substantial, averaging 8.5% of non-interest expense, compared to less than 3% for traditional banks1. This investment is paying off, as Fintechs continue to capture market share, particularly among younger borrowers.

One of the most significant shifts in consumer lending behavior is the rise of Buy Now, Pay Later (BNPL) products. Usage of BNPL services has increased by nearly 6% year-over-year, with Gen Z and Millennials accounting for the vast majority of users2. However, this growth comes with risks: late payments among BNPL users have risen from 18% in 2023 to 24% in 2025. Credit unions must be mindful of these trends, as they reflect broader changes in how consumers manage credit and debt.

Credit tier dynamics are also evolving. The majority of new originations within the credit union industry—about 67%—occur in the Prime or Super Prime segments. This reflects a tightening trend nationally, as lenders become more cautious in their underwriting. At the same time, Fintechs are experiencing significant growth in subprime and deep subprime originations, with nearly 45% of their originations falling into these categories. This shift is particularly pronounced for secured card products, which are increasingly targeted at borrowers with lower credit scores.

Mortgage market conditions have changed dramatically in recent years. Interest rates are now hovering near 7%, a stark contrast to the rates that prevailed for much of the previous decade. As a result, two-thirds of mortgages are locked in below 4%, creating a market freeze and limiting new activity. Despite these challenges, credit access has improved in some segments. The Cox Automotive Dealertrack Index reports three consecutive months of increased approval rates within auto finance, with a 210 basis point jump from June to July 2025. This loosening of credit is benefiting auto-focused finance companies, captives, and banks, and may present opportunities for credit unions to expand their lending portfolios.

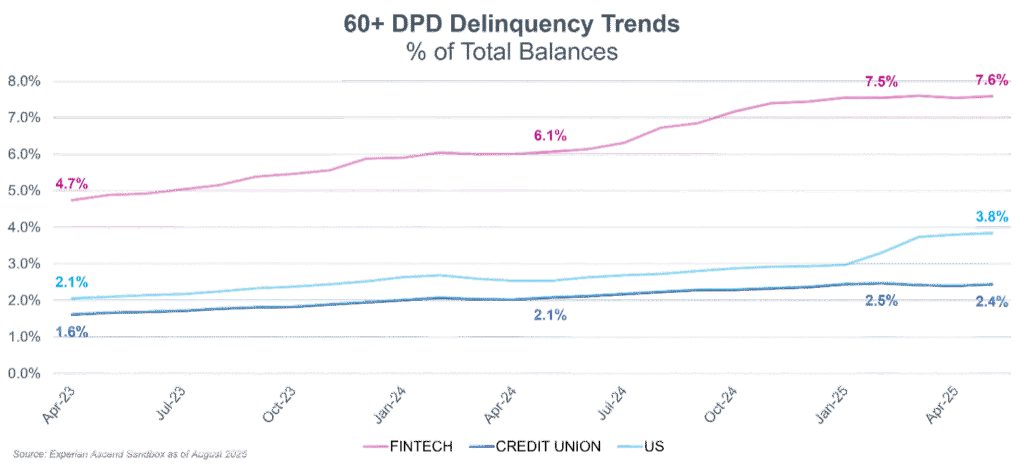

Delinquency trends offer a mixed picture. For credit unions, delinquency rates have remained relatively flat since December 2024, suggesting stability in member repayment behavior. However, financial stress is evident across many segments, and fintech portfolios show higher delinquency rates due to their greater exposure to subprime borrowers. Student loan repayment is a particular area of concern. Of the 26.6 million consumers with non-deferred student loans, 21% were 90-180 days past due in July 2025. While student loan delinquency has plateaued, there is a slight uptick in revolving and auto loan delinquency, indicating continued risk in these portfolios.

Key trends for Gen Z

Generational shifts are reshaping the lending landscape. Gen Z is emerging as the next wave of borrowers, with all members of this generation expected to be credit-eligible by 2031. The largest cohorts of Gen Z are aging into credit eligibility in the next one to two years, but declining birth rates mean that the outlook will eventually taper off. Young Gen Z (16-19 years) are joining the labor force at a decreasing rate, and financial behaviors of Gen Z, as a whole, differ from older generations. They tend to interact with more financial institutions, making it easier to lose track of financial products and services. Their first borrowing experience is increasingly with credit cards, while retail cards are becoming less common.

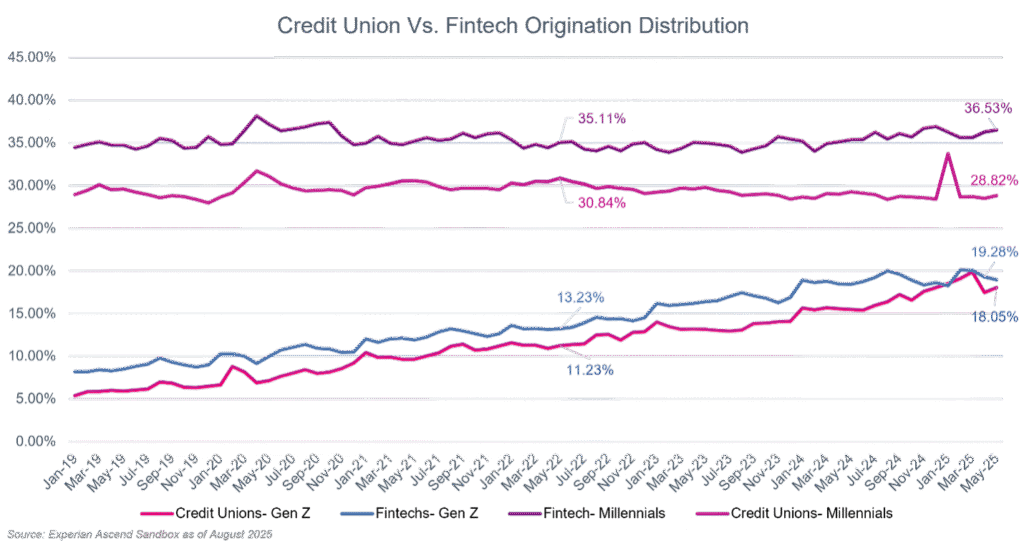

Credit unions and Fintechs are seeing a growing share of Gen Z members within their portfolios.

A ten-year study (2014 – 2024) among Gen Zers born in 1996 found that by 2024 (28 years old):

- Over 91% had a credit card (up from 58% in 2014 at 18 years old)

- 25% had achieved Super Prime status

- 21% had a mortgage

- 63% had an auto trade.

These figures highlight the growing importance of Gen Z as a target market for credit unions.

Understanding Gen Z’s preferences is crucial for credit unions seeking to attract and retain younger members. When it comes to buying banking products or services based solely on brand trust, Gen Z has a higher affinity for digital brands like Google, Venmo and Apple than their primary bank or credit union. They value mobile banking, incentives, fraud prevention, and a convenient account opening process.3

A snapshot of Gen Z’s credit profile reveals notable changes over the past six years. The average Vantage Score has increased from 644 in December 2019 to 668 in September 2025, and the median score has risen from 663 to 684. The average number of credit cards per Gen Z member has grown from 1.63 to 1.99, and the average credit card balance has jumped from $2,572 to $3,744. Mortgage debt and student loan balances have also increased, reflecting broader economic trends.4

Student loan repayment impact

Nearly 27 million consumers had non-deferred student loans as of July 2025:

- More than half of these consumers have made payments in the last three months and are not 90-180 days past due

- ~19% have not had a payment reported in the last three months but are not yet 90-180 days past due

- ~21% were reportedly 90-180 days past due in July 2025

- Consumers who are currently past due have seen a sizable decrease in average VantageScore® since December 2024

While student loan delinquency has plateaued and there’s only been a minimal increase in delinquency on non-student loans among these consumers, upcoming wage garnishments could soon impact the ability to pay these facilities. Ninety five percent of delinquent loans reported are federal student loans, which become eligible for wage garnishment at 270 days past due.

Actionable strategies for credit unions

- Embrace digital transformation: Compete with Fintechs by investing in digital account opening, mobile banking, and fraud prevention capabilities.

- Target Gen Z and millennials: Develop products and marketing strategies tailored to younger generations’ preferences, including incentives, mobile-first experiences, and financial education.

- Monitor credit tier trends: Stay vigilant on shifts in prime, subprime, and super prime segments, and adjust risk management strategies accordingly.

- Support student loan borrowers: Offer resources and flexible repayment options to members with student debt and prepare for potential impacts from wage garnishments.

- Leverage data analytics: Use portfolio analytics to identify emerging risks and opportunities, especially as market conditions and consumer behaviors evolve.

In conclusion, current market conditions present both challenges and opportunities for credit unions. By understanding the latest trends in originations, credit tiers, generational shifts, and delinquency, credit unions can position themselves for sustainable growth and member success. Staying member-driven and market-ready will be key to navigating the evolving financial landscape.

For additional information, visit Experian’s credit union website or our Thought Leadership Hub where you’ll gain insights into the fast-changing world of consumer and business data.

3 E-Marketer, Experian Economic Strategy Group

4 Experian State of Credit