Credit unions are always looking for ways to grow membership, expand lending, and better serve their communities. Yet one of the fastest growing segments of potential homebuyers in the United States remains largely overlooked: Muslim Americans.

For many Muslim families, the barrier to homeownership is not creditworthiness or income. The barrier is access to financing that aligns with their faith.

Islamic principles prohibit the payment or receipt of interest, commonly referred to as riba. Because of this, many Muslims avoid conventional mortgages entirely.

The result is a significant gap in the housing market.

Thousands of financially qualified families are ready to buy homes but cannot use traditional mortgage products.

At the same time, the Muslim American population continues to grow and many households are reaching prime homebuying age, making homeownership an increasingly important goal.

Understanding Islamic home financing

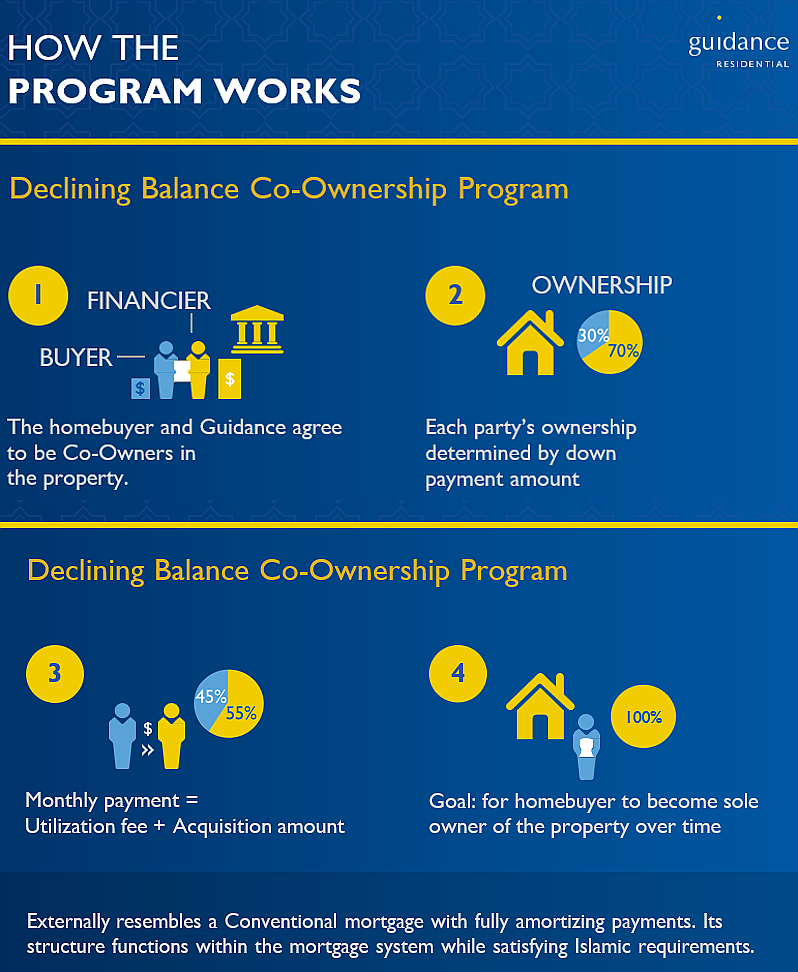

Guidance Residential offers a Declining Balance Co-Ownership model, where the financial institution and the homebuyer purchase the property together and the homeowner gradually increases their ownership share over time.

Unlike a conventional mortgage where a bank lends money with interest, this model is based on shared ownership of the property.

A practical opportunity for credit unions

Through Guidance TPO (Third Party Originations) partnerships, credit unions can offer Islamic home financing while leveraging established expertise and infrastructure. For credit unions committed to financial inclusion and community service, serving Muslim homebuyers represents both a mission driven opportunity and a growing market.