When credit unions evaluate digital asset programs, the conversation usually centers on regulatory clarity, member demand and competitive pressure. Those are the right topics. But there’s one that doesn’t come up nearly enough: custody.

Where do your members’ digital assets sit? Who controls them? And what happens to those assets if something goes wrong with the custodian?

The NCUA’s proposed rule under the GENIUS Act requires qualified custody infrastructure for any credit union subsidiary seeking a stablecoin issuer license. The interagency guidance on crypto-asset safekeeping warns against commingling custodial assets. The regulatory direction here is not ambiguous. But most credit unions haven’t dug into how custody works under the hood of the platforms they’re evaluating.

Two models, very different risk profiles

There are two primary custody structures in the market right now for credit unions (CUs) offering digital asset services.

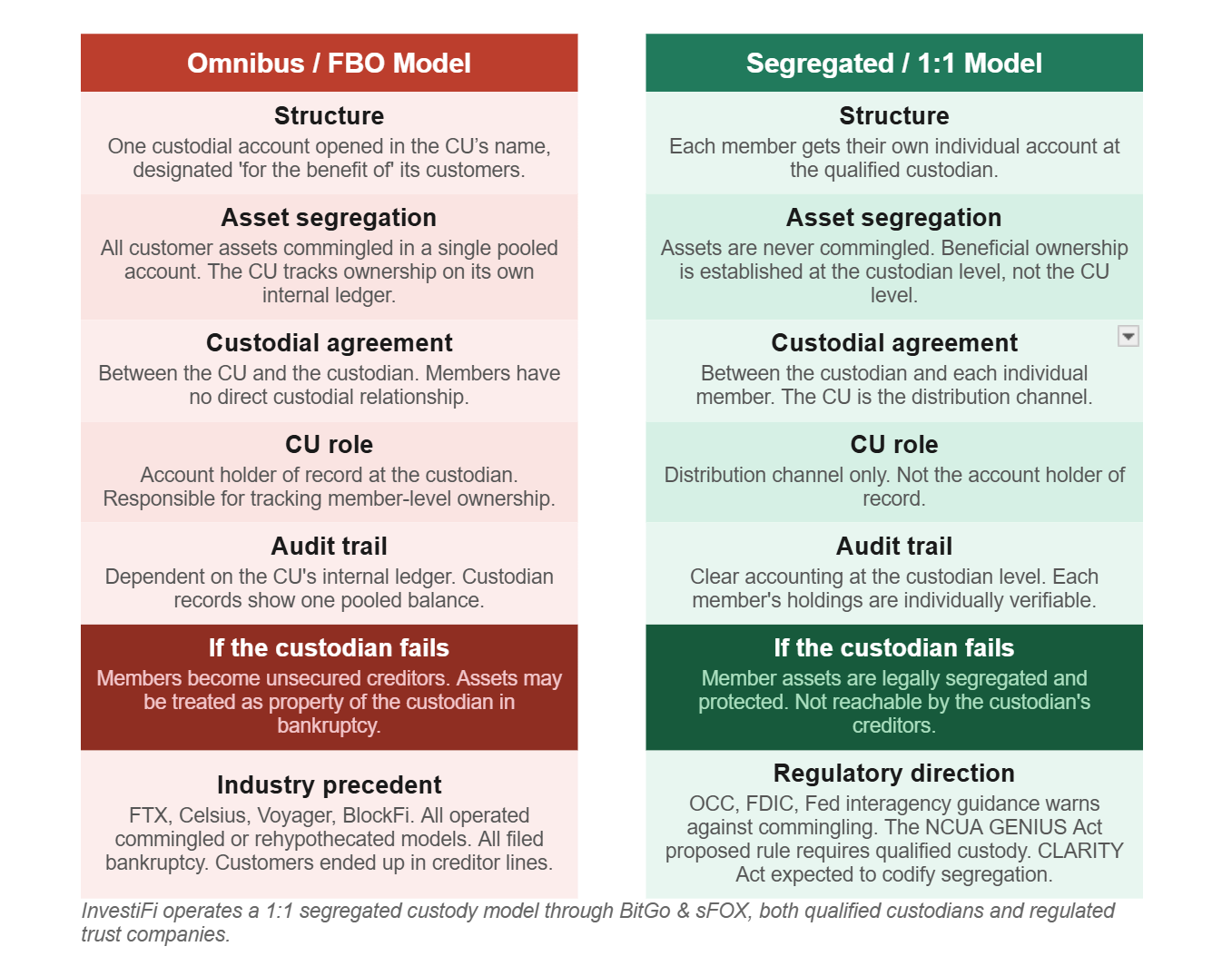

Omnibus/FBO model

One custodial account opened in the credit union’s name, designated “for the benefit of” its members. All member assets sit in that single account, commingled. The custodial agreement is between the institution and the custodian. The CU tracks who owns what on its own ledger.

Segregated/1:1 model

Each member has their own account with the custodian. Assets are never commingled. Beneficial ownership is established at the custodian level. The CU is the distribution channel, not the account holder of record.

Both models are being offered to credit unions today, but they are not the same.

Digital asset custody models: A side-by-side comparison

We’ve already seen how this plays out

FTX held customer funds in pooled accounts. When the firm collapsed in 2022, there was no clear asset segregation at the custodial level. Customers became unsecured creditors in a bankruptcy proceeding. Celsius, Voyager, BlockFi. Same pattern. Customer assets were commingled or rehypothecated, all three filed for bankruptcy, and customers ended up in a creditor line.

The through line is consistent. When assets are held in omnibus accounts at the institution level rather than segregated at the custodian level, customers bear the institution's credit and operational risks in addition to the market risk of their assets.

What regulators are saying

The interagency guidance on crypto-asset safekeeping, issued by the OCC, FDIC, and Fed, states directly that it would be inconsistent with appropriate risk management for a sub-custodian to commingle its own assets with those held on behalf of a banking organization. The concern is that commingled assets could be treated as property of the sub-custodian in a bankruptcy scenario.

The OCC reaffirmed crypto custody as a permissible banking activity and dropped prior-approval requirements. But the expectation around account segregation, vendor oversight, and recordkeeping has gone up, not down. The NCUA’s proposed rule under the GENIUS Act requires qualified custody as part of the licensing framework. The CLARITY Act, still in Congress, is expected to further codify segregation requirements.

Regulators are heading in one direction on this. Segregated, individually titled accounts.

What your compliance team should be looking at

If you’re evaluating a digital asset provider, these are the questions that matter:

- How are member assets held at the custodian? Individual segregated accounts, or a single omnibus account in your credit union’s name? If it’s FBO, understand what that means for your members’ legal claim to those assets in an adverse event.

- Who is the custodial agreement between? The custodian and each member? Or the custodian and your credit union? That distinction matters in insolvency scenarios.

- What happens if the custodian fails? Are member assets legally segregated from the custodian’s own holdings? Can they be reached by the custodian’s creditors?

- What’s the audit trail? Can you produce a clear accounting of which member owns what, at any point in time, directly from the custodian’s records? Or are you dependent on your own internal ledger for that?

- How does this hold up under examination? The NCUA is updating examination policies for digital asset activities. Your examiner is going to ask about custody. A clear answer backed by segregated accounts at a qualified custodian is a stronger position than explaining why you went with a commingled model.

How we handle this at InvestiFi

At InvestiFi, we use a 1:1 segregated custody model through a qualified custodian and regulated trust company. Each member gets their own individual custodial account. Assets are never commingled. That’s a compliance decision based on where the regulatory landscape is heading and what we believe is the right standard for credit union members.

The credit unions we work with don’t have to explain an FBO structure to their examiner. The custody question is answered before it gets asked.

Where this is going

The NCUA’s proposed stablecoin licensing framework, the interagency safekeeping guidance, and the pending CLARITY Act all point in the same direction. Regulators expect segregation. They expect qualified custodians. They expect clear documentation of beneficial ownership.

Credit unions building their digital asset programs on that foundation are in a strong position. Those that went with a commingled model because it was easier or cheaper to stand up may find themselves having a different conversation with their examiner down the road.

Custody isn’t a back-office detail. It’s the compliance question that will determine which digital asset programs hold up under scrutiny and which don’t.