Credit union mobile banking: Leading edge or the latest example of marketing myopia?

What mobile banking enhancements should come next?

Credit unions will need to do more than just “keep up” with large FI innovation in mobile banking. The basic five or six features in a typical mobile banking app are a must for consumers. However, members may soon be looking for added functionality for big life decisions like home and auto purchase and maintenance, P2P money transfers, external A2A transfers and even voice-activated services.

I feel really old now when I think of my first marketing class and that 1960s article on Marketing Myopia by Theodore Levitt. It seemed so cutting edge back in the 80s, but what does it mean some 40 years later?

Every credit union executive is surely aware of those concepts that I’ll summarize in an elevator pitch here: Focusing on “customer satisfying” processes vs. products will help keep credit unions from failing like railroads (which failed because they were “railroad oriented instead of transportation oriented; they were product oriented instead of customer oriented.”).

Railroads declined not because of cars, trucks, airplanes, and even telephones, but because of their own myopia.

Could credit unions and banks fail for the same reasons? If they focus too much on checking accounts, loans, plastic cards, ATMs, and “five-featured” mobile banking, are they at risk of missing key opportunities to help members and customers with their important life decisions more holistically? And if this happens, abruptly or gradually, which fintech companies will step in to fill the void?

And even as credit unions scurry to keep up with larger FI innovation on basic features like P2P, alerts and card controls, banking voice technology is becoming more mainstream. Some banks, like Barclays and HSBC, have replaced passwords with voice recognition for identity verification. And a little over a year ago, Wells Fargo announced voice-activated balance checks and funds transfer, as well as plans to offer personal financial advice through a blend of AI and its voice-driven assistant.

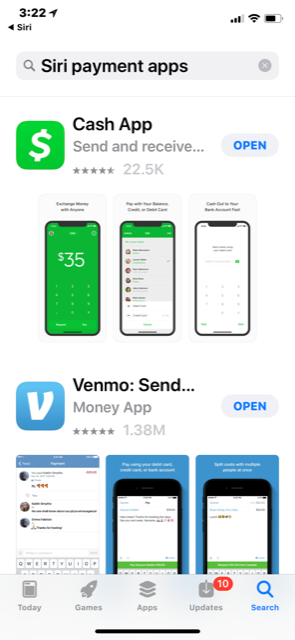

Try this experiment like I did recently. I went into my credit union mobile banking app and prompted Siri on my iPhone, “pay bills.” The reply came back, “You’ll need an app for me to help you with that. You could try searching the App Store.” And when I clicked on the app store link, up came this visual:

My credit union app didn’t recognize my request. Instead, my iPhone sent me to the app store and asked me to download or open either Square’s Cash app, or PayPal’s Venmo. Of course, we now know that one third of all credit union members already have a PayPal account, and something like two thirds of their millennial members already use Venmo.

So, are credit unions ready to be revolutionary in their approach to mobile banking by giving members what they are looking for, or will they focus on their existing products and features?

Isn’t that what the railroad industry did by being too product centric? And what did Netflix see that the cable companies did not? The list of myopic companies, of course, is endless; many businesses fail to understand the basic marketing principle taught by Levitt almost six decades ago: “Selling focuses on the needs of the seller, marketing, on the needs of the buyer.”

The Royal Bank of Canada will soon allow customers to pay bills on their Apple iPhone by simply asking Siri, and USAA and Capital One customers can conduct banking activities with Amazon’s Alexa. It appears that banks are using voice recognition either for identification and security or for customer service. A recent Accenture poll said that 76 percent of bankers believe that AI will soon become the primary point of contact between banks and customers.

A recent study by the Federal Reserve Bank of Boston, published in December of 2017, surveyed financial institutions about their mobile banking and payment practices and plans. This was done in seven federal reserve districts across the country. Some of the findings were not surprising, but others give credit union leaders a potential roadmap for a strong mobile strategy moving forward.

Not so surprisingly, mobile banking services are becoming ubiquitous and all financial institutions are now focused on driving usage and ongoing engagement. The challenge, of course, is that it is very difficult to differentiate financial services … even mobile banking. All players seem to want to focus on six (or so) rather boring, or “expected”, features: balances, transfers, history, bill pay, ATM/branch locators, remote deposit capture and mobile enrollment.

The challenge here is two-fold. First, if all FIs are doing the same things, how do credit unions stand out and differentiate? Second, in stark contrast to Levitt’s guidance, these same tired features appear to reshuffle the same deck of services rather than evolving to meet the customer’s growing needs. Or at least in the second case, they may not be going far enough to identify and serve those needs.

The starkest example of modern-day mobile myopia may be that most credit unions don’t yet have a good P2P solution embedded in their mobile app, at least not one that is widely recognized or already used by members. And PayPal and its Venmo product are meeting those needs outside of the traditional mobile banking experience.

Key Findings from 2017 Federal Reserve Research and Next Step Considerations for Mobile

In addition to reinforcing the obvious points that all FIs want to offer an affordable and high-quality mobile banking experience, and that most consumers now expect that from their FI, the Fed report also suggests:

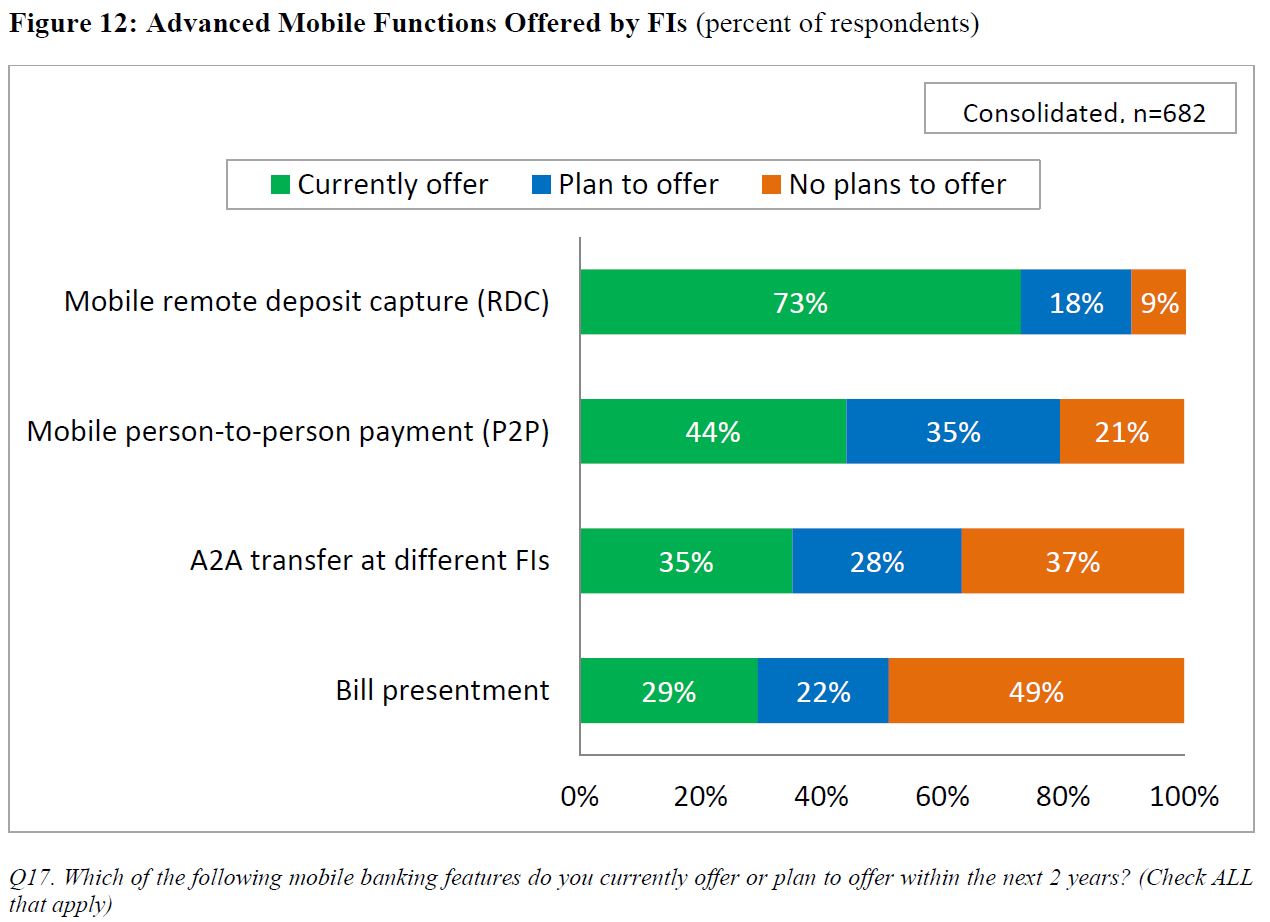

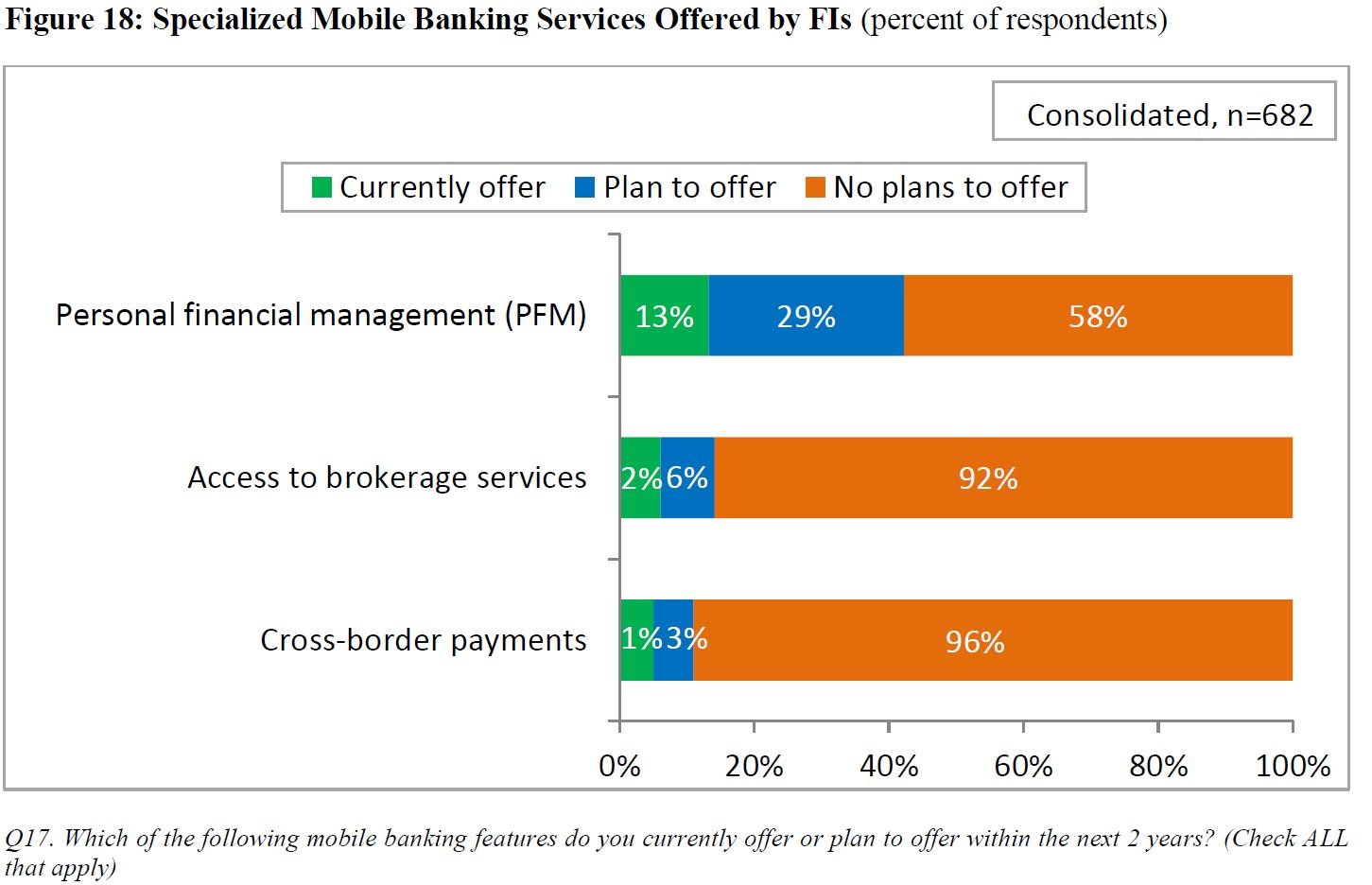

- Standardization makes mobile banking another commodity: FIs have standardized their mobile banking around five or six features: balances, transfers, history, bill pay, ATM/office locators, remote deposit capture and mobile enrollment.

- Features coming soon: Most progressive FIs are working on P2P, external A2A (account-to-account) transfers, alerts, card controls, member education and security features. There is a growing realization that the mobile app should educate and inform as well as enable transactions.

- Partnering for mobile payments: Financial Institutions remain interested in pursuing mobile payments through partnerships, and more than half are considering NFC contactless solutions as one of their wallets. However, this strategy remains elusive and uncertain as Apple Pay, Android Pay, Samsung Pay and large retailers appear best positioned to capture payment transactions through their own apps. An “if you can’t beat ‘em, join ‘em” approach seems most in vogue now, and member education should be the focus.

- Security and education go together: For consumers not yet using mobile banking, security concerns are the main impediment. This is driving FIs to realize the importance of consumer education regarding security, as well as implementing alerts, biometric authentication, voice recognition, tokenization and card control features.

- It’s not easy being small: No huge surprise here for credit unions … smaller FIs find it difficult to afford the enabling technologies that help meet consumer needs. Credit union collaboration and partnering are more critical than ever.

- Payment speed matters: As Zelle attempts to kill Venmo, real-time money transfers will become the norm and the expectation of consumers.

- Comprehensive mobile strategies: No credit union or bank, regardless of size, can afford to be without a comprehensive mobile banking and payments strategy. Offering these services is no longer an option. The focus is now on usage/engagement and education. Solutions for small businesses are growing in importance as well. And all FIs should want to differentiate by adding more robust service features to their mobile app. In fact, lest we want to play “catch up,” this may be the time to look at AI and voice recognition integrated within the mobile banking app.

- Marketing and education intersect: If you build it, they won’t necessarily come. Marketing and education messaging must overcome consumer misperceptions about security, data breaches, identity protection and the biggest one: that my bank or credit union lacks the sophistication to help me with my life’s big decisions.

– 2017 Federal Reserve Bank of Boston Study

– 2017 Federal Reserve Bank of Boston Study

Future Mobile Banking Enhancements by Financial Institutions

What Should Come Next for Credit Unions’ Mobile Banking Strategies?

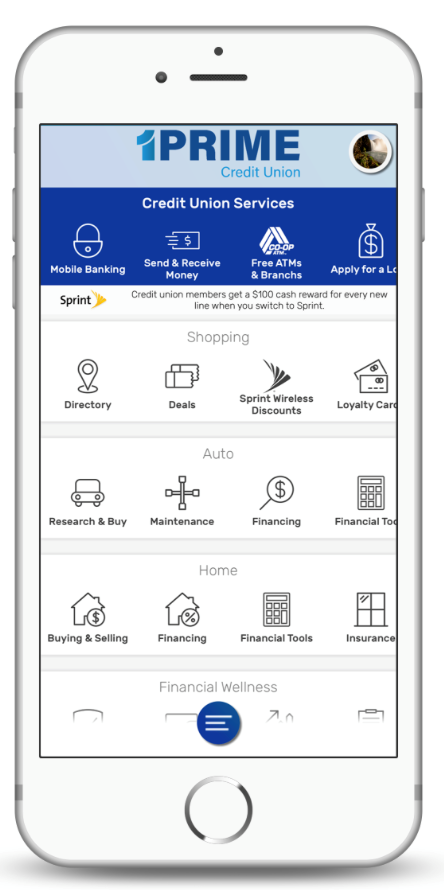

CU Solutions Group (CUSG) has hundreds of credit union clients for its web-based and mobile banking solutions. Its most current product, LifeSteps Wallet, will help credit unions with their two most important marketing challenges: how to differentiate mobile banking, and how to focus on the needs of the member versus the credit union’s own products.

Let’s just admit it. Most people think banking is boring. It’s a necessity, but it isn’t sexy. Consumers expect the basics, but they’re wowed by features that don’t look like banking. The same is becoming true of mobile banking. Keeping an app pure, secure and uncluttered is a noble goal, but taken to the extreme, all mobile banking apps just look the same.

CUSG’s LifeSteps Wallet creates a custom mobile banking app that wraps around the core mobile banking features, those five or six standard functions, but then expands resources into areas of shopping, auto and home ownership/maintenance and financial wellness needs that include identity protection, card protection and financial education.

Credit unions should approach mobile banking like Maslow’s hierarchy of needs. Consumers expect the bare minimum five or six features, but won’t be wowed into doing business with the credit union or bragging about their mobile banking app until the credit union truly helps them reach that next level: P2P (peer-to-peer money transfers), external A2A (account-to-account money transfers) and access to tiles in the app that help research, shop, buy and maintain big purchases, all aided by their credit union products.

Reaching for an even higher level in the hierarchy, the integration of voice recognition and AI seem to be the next big thing in remote banking. It may be a long time before even a small number of credit unions can rival the voice recognition/chatbox capability of Bank of America’s Erika product, or American Express’s voice integration with Alexa, but what they can do is innovate in other ways that differentiate them in the market.

LifeSteps Wallet is an example of one CUSO (CUSG) investing millions of dollars in a truly different mobile banking strategy that will help credit unions of all sizes stand out from the pack and focus on consumers’ highest-priority mobile buying needs. Credit union financial services can be an important driver for satisfying those needs. But putting the needs of the buyer (members) ahead of the seller (credit unions and their products), will help credit unions grow and prosper in the age of Apple’s Siri, Amazon’s Alexa and Samsung’s Viv.