Over the years, our firm has delivered hundreds of presentations to credit union boards. The goal is to provide the board with insights and guidance to support informed decision-making regarding benefits for their executive leadership teams. In the last ten years, our discussions have increasingly centered around split dollar plans—and understandably so. Split dollar plans are one of just a couple of arrows in a credit union’s quiver to retain and reward key executives. While these plans can bring significant economic advantages to both a plan participant and its credit union sponsor, they can create a level of complexity. Aside from choosing the right fit from the variety of available plan designs and product options, having a properly serviced plan is equally, if not more, critical.

For me, the highlight of any education presentation is the interaction driven by board questions. After projections have been reviewed and the pros and cons of various options have been discussed, questions allow us to gauge the board’s understanding of the concepts shared. Knowing we have only scratched the surface of a complex subject, it’s important to know if the key concepts are fully understood or if any gaps need filling.

My absolute favorite question is one that comes up quite often. It is simple, yet profoundly important, and usually comes up at the end of an already long discussion. “Tell us, what questions should we be asking, but haven’t yet?” This question acknowledges an important point: was the meeting just a sales pitch meant to persuade one to buy a certain type of life insurance? Or was it a genuine effort to educate a group of decision makers as they navigate the gauntlet of options and considerations? Our response is that there’s more to the split dollar story than what you just heard. Given the time and setting aside other board meeting agenda items, we’d like to tackle that question comprehensively to reflect its importance.

These five questions are not always asked during a split dollar educational session, but if we were making such an important decision for our credit union, we’d want them answered.

Question #1: What factors help determine the long-term success of an executive benefits program?

- Flexibility—not only in the product itself but in plan payment

- Proper adjustments when interest rates change

- Consistent tracking of actual vs projected performance

- Modifications to behavior during the distribution phase

- Assessing policy loans vs distributions

- Evaluating risks and benefits of loan riders

- As an owner, capability doesn’t equate to necessity

Question #2: What types of insurance policies are available to support the program?

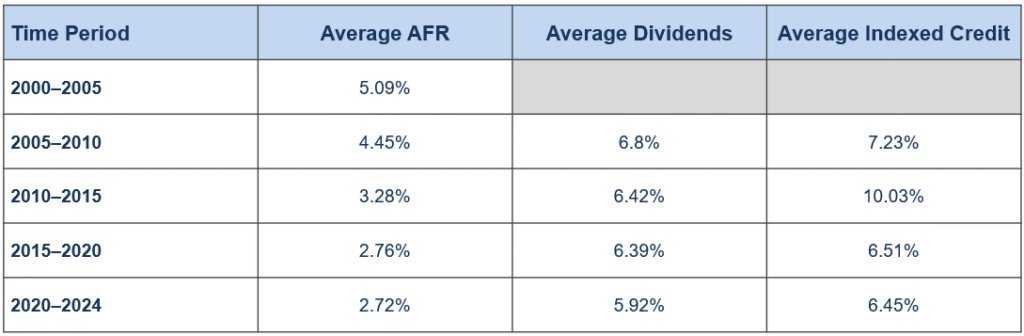

Understanding Index Universal Life (IUL) vs Whole Life (WL) vs Variable Universal Life (VUL)

- IUL = Multi-factor crediting rate determination (comes with pros and cons)

- WL = Consistent returns, expensive internal policy charges, likely longer recovery when dividend rates fall below projected

- VUL = Allows for maximum upside, risk, volatility, flexibility

- The importance of a cushion cannot be understated

CAP Rates from: Securian. Treasury Rates from: https://www.multpl.com/10-year-treasury-rate/table/by-year.

Question #3: As our consultant, can you explain how your compensation is calculated?

What to expect:

- Understanding of the consultant’s total compensation/commissions and payment source

- A comparison of commissions paid on the recommended product versus alternative carriers and products

- Any service, administration, or consulting fees charged to the credit union

- Consultant compensation and firm-retained compensation for ongoing administration

- How compensation is paid over time; does it align with your broker’s long-term service commitments

What should raise concern:

- An unbalanced approach to product recommendations, for example, "Whole life is superior and you don’t need to consider any alternatives,” because Whole life has significantly higher commissions, especially early on

- Excessive front-loaded compensation or compensation schedule that ends after the premium payment is made

- Providing essential plan administration services at no cost

Question #4: Tell me about your service team, carrier relationships, reporting systems, and professional relationships.

What to expect:

- Our firm has a deep bench that is primarily focused on the critical post-sale phases of your executive benefit plan

- A dedicated team annually reviews the plan’s performance and competitiveness. These reviews also provide documentation for regulatory purposes

- A secure, online platform to assist the credit union and executive participant. Ours is housed in a SOC-1 certified online platform

- Our firm is independent, offering clients access to multiple plan types, various life insurance companies, and different plan structures (i.e., whole, indexed universal, and variable life)

- Our firm has decades of experience implementing and administering benefit plans for credit unions, backed by an even longer history as an established organization and an internal succession plan to support the duration of your plan

- We can provide a list of clients and specific references from both board and executive levels

- We provide customized quarterly reports and are available to address day-to-day questions about your benefit plan's compliance, reporting, and accounting needs

- Our experienced team manages the critical phases of plan fulfillment and completion (death) with care—supporting executives, families, credit unions, and insurers through each step

What should raise concern:

- We have a small team, mostly in sales, and a third-party handles administration

- After we put the plan in place, the life insurer will take over

- Our team acts as an agent for a specific life insurance company

- We exclusively provide split dollar plans, only indexed universal life products, or only whole life products

- Staff are 1099 contractors, not employees

- You tell us what your auditors need, and we send Excel files

- We provide the insurer’s 1-800 number for help accessing your funds and death proceeds

Question #5: How likely is the illustration to perform as shown?

What to expect:

- An overview of return assumptions from illustrations versus actual return determination

- A high-level understanding of the insurance product itself and the impact of economic conditions and interest rate changes on policy returns

- Comprehending implications for the executive and organization should the plan's performance fall short of projections

- Knowing how distributions from the policy are made, along with factors that may affect policy values and repayment of the loan

What should raise concern:

- Statements guaranteeing the policy will produce the returns projected

- Looking at the projected rate and history of the dividend/crediting rate as the only thing that matters

For a deeper dive into insurance policy selection, check out our article, https://www.ajg.com/news-and-insights/funding-split-dollar-plans-with-whole-life-or-index-universal-life/.

This material was created to provide information on the subjects covered, but should not be regarded as a complete analysis of these subjects. The information provided cannot take into account all the various factors that may affect your particular situation. The services of an appropriate professional should be sought regarding before acting upon any information or recommendation contained herein to discuss the suitability of the information/recommendation for your specific situation.

Consulting and insurance brokerage services to be provided by Gallagher Benefit Services, Inc. and/or its affiliate Gallagher Benefit Services (Canada) Group Inc. Gallagher Benefit Services, Inc., a non-investment firm and subsidiary of Arthur J. Gallagher & Co., is a licensed insurance agency that does business in California as “Gallagher Benefit Services of California Insurance Services” and in Massachusetts as “Gallagher Benefit Insurance Services.”

Investment advisory services are offered by Gallagher Fiduciary Advisors, LLC (“GFA”), an SEC registered investment advisor that provides retirement, investment advisory, discretionary and independent fiduciary services. Registration as an investment adviser does not imply any specific level of skill or training and does not constitute an endorsement of the firm by the SEC. GFA is a limited liability company with Gallagher Benefit Services, Inc. as its single member. GFA may pay referral fees or other remuneration to employees of Arthur J. Gallagher & Co. or its affiliates or to independent contractors; such payments do not change our fee. Neither Arthur J. Gallagher & Co., GFA, their affiliates nor representatives provide accounting, legal or tax advice.

Securities offered through Osaic Wealth, Inc. member FINRA/SIPC. Osaic Wealth is separately owned and other entities and/or marketing names, products or services referenced here are independent of Osaic Wealth. Neither Osaic Wealth nor their affiliates provide accounting, legal or tax advice. GFA/Osaic CD (8461191)(exp092027)