For decades, credit unions have supported their communities through traditional charitable giving: writing checks, sponsoring events, and quietly funding essential local work. It is admirable, and it is also predictable. Members today expect their credit union (just like they expect ALL their brands) to show up in ways that are visible, engaging, and unmistakably cooperative.

If credit unions want to stand out, it is time to rethink how they give.

The tools already exist. What is missing is a shift in mindset.

CDAs: The most underutilized asset in credit union philanthropy

A Charitable Donation Account (CDA) allows a credit union to invest up to 5% of its net worth in a segregated custodial account or trust. Unlike traditional charitable allocations drawn from operating income, CDA assets can be invested in expanded, higher-yielding instruments not normally permitted under standard investment rules.

The CDA’s defining structure is simple:

- At least 51% of the earnings must be distributed to 501(c)(3) charities.

- Up to 49% may be retained by the credit union.

This means a CDA can generate a renewable pool of charitable dollars without increasing operating expenses. Credit unions can forecast their charitable capacity in advance, enabling proactive planning, multi-year commitments, and faster action without relying on annual budget approvals or operating income.

Yet the tool remains dramatically underutilized with fewer than 400 credit unions participating, and many of them investing far below their allowable cap.

Even among credit unions that have a CDA, most use only the baseline function: distributing earnings as annual gifts.

Necessary? Yes.

Transformative? Not yet.

The real opportunity lies not just in funding charitable dollars, but in deploying them.

When CDAs fuel amplification, giving becomes strategy

The most powerful use of CDA dollars is not writing larger checks. It is amplifying them.

Amplification occurs when a credit union uses its charitable dollars to unlock far more generosity from the community. Matching campaigns are the clearest and most consistently effective model.

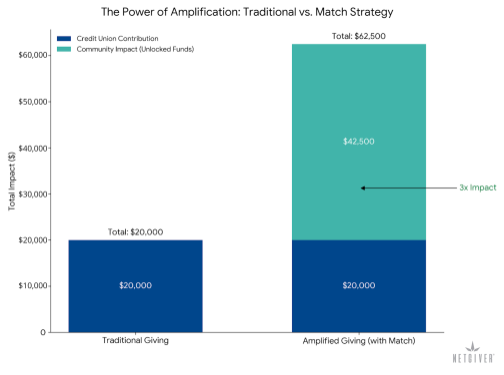

A real-world model: What amplified giving looks like

Consider a recent credit union campaign where a match commitment generated outsized results:

- More than $60,000 raised

- Over 100 nonprofits supported

- More than 1,000 donors engaged

- Hundreds of members participating and hundreds of new members joining

- All driven by a match strategy that multiplied community giving

This example demonstrates the exact type of amplification CDA earnings can fuel—reliably, sustainably, and without drawing from the operating budget.

Now imagine running this kind of campaign every year (or even multiple times a year) funded entirely by a renewable stream of CDA returns. Amplification strategies can be designed with intention and with direct benefit back to the credit union.

That is the opportunity in front of every credit union today.

Why CDA-powered amplification is a strategic advantage

Using CDA earnings to run high-visibility, high-engagement campaigns strengthens a credit union in three strategic ways:

- High-visibility community leadership: Matching campaigns put the credit union at the center of generosity, building trust, goodwill, and brand equity in ways traditional giving simply cannot.

- Stronger, more valuable partnerships: Nonprofits prioritize partners who help them raise more, not just give more. CDA-funded amplification elevates the credit union from donor to catalyst.

- Deeper member loyalty and engagement: Members want alignment with their values. When giving becomes participatory, visible, and multiplied, member affinity increases.

This is philanthropy not as an expense but as a strategy.

Why CDAs are the credit union movement’s hidden advantage

CDAs allow credit unions to:

- Stretch every charitable dollar;

- Generate new, renewable giving capacity;

- Invest in higher-yield assets;

- Drive measurable community outcomes; and

- Create standout visibility in local philanthropy.

The regulatory requirement to distribute at least 51% of earnings every five years is not merely a compliance obligation, it is a built-in opportunity. Credit unions are incentivized to innovate in how they give.

Traditional giving is generous.

CDA-powered giving is generative.

Making CDA strategy practical and accessible

For many credit unions, the biggest barrier to using a CDA more strategically isn’t appetite or intent, it’s uncertainty about execution. Who structures the account? Who manages the investments? And who helps turn earnings into visible, measurable impact?

The good news: credit unions don’t have to do this alone.

Charitable Donation Accounts are already supported by trusted partners deeply embedded in the credit union system. Providers such as Acumen, Earnest Consulting Group, and TruStage work closely with credit unions to structure, invest, and manage CDAs in accordance with regulatory guidelines, helping ensure assets are deployed responsibly while generating renewable returns.

But a CDA alone doesn’t create impact, strategy does.

That’s where strategic partners come in. Organizations like Imagine the Difference design and execute distribution strategies that amplify CDA earnings through matching campaigns, donor engagement, and nonprofit collaboration.

These partners help transform CDA returns from passive distributions into participatory moments of generosity that strengthen community trust and member affinity.

Importantly, neither type of partner requires new out-of-pocket expenses. CDA providers are compensated through the investment structure itself, and amplification strategies can be funded using existing CDA earnings or sponsor support.

The infrastructure exists. The partners are ready. What remains is the decision to move from traditional giving to strategic, amplified impact.

A new path forward

The amplification model shows what becomes possible when a credit union uses its dollars to inspire, multiply, and activate generosity. Now picture that same catalytic effect fueled not by the operating budget, but by a renewable stream of CDA earnings.

That is the future of credit union philanthropy.

Credit unions have the tools.

Communities have the need.

CDAs provide the fuel.

It’s time to use them not just to fund giving—but to transform it.