The card-not-present-chronicles: Assessing the health of your debit authorization and fraud program

In our previous article in this series, we discussed the top five areas that credit unions should consider to drive a positive card-not-present / e-commerce experience for members. This article will take a deeper dive into authorization and fraud programs and the importance of their role in a credit union’s overall card-not-present strategy.

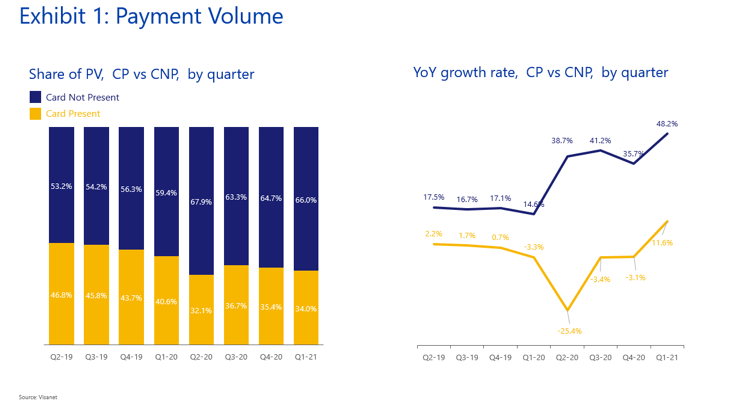

The shift from card present to card-not-present has been accelerated by COVID-19. The data in Exhibit 1 represents debit payment volume in the US beginning Q4 2019. Although card-present in-store payment volume is back to pre-pandemic levels, the COVID-19 recovery has been led by the card-not-present channel. The card-not-present channel now accounts for approximately 60% of all debit payment volume in the US.

In a card-not-present environment, customer experience is critical, particularly around the successful completion of payments. Did you know that the average credit union member gets declined around 12 times for every 100 attempts to use their debit cards online? Almost all of those are opportunities for the member to reach into their wallet to find another card that ‘just works’!

Credit unions typically reject purchases for two main reasons – they suspect fraudulent activity, or there are not enough funds in the linked checking account to cover the purchase. Both are valid decline reasons, but credit unions typically take a conservative approach with suspicious purchases, which may result in higher false positive decline rates and thus hurting customer experience.

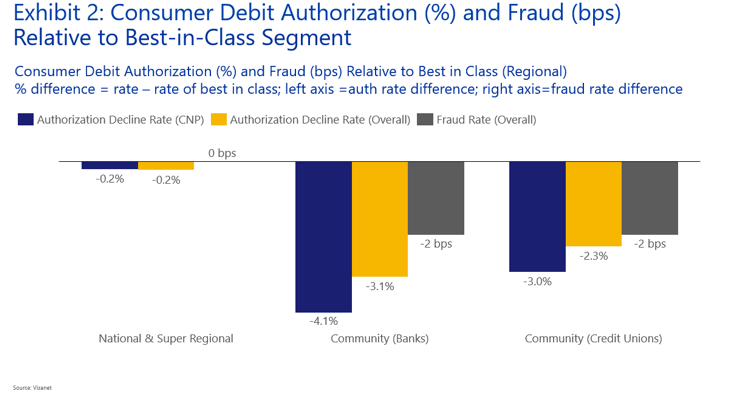

The data in Exhibit 2 shows decline rates compared to fraud rates for various financial institution types. The data is relative to the category of banks that is best-in-class – regional banks in this case. Community banks and credit unions decline many more transaction attempts than their larger peers, with the trend worsening for card-not-present transactions. While the need to prevent fraud is important, these institutions miss the full impact of a false positive decline. In addition to the loss of spend revenue for the credit union, this is also a negative customer experience that can impact cardholder engagement. Some cardholders will reduce their spend on the card, while others will become completely dormant as they opt for a competitor’s card. The worst-case scenario is that the overall membership relationship is compromised, with the customers leaving the credit union (e.g., switch checking account providers, cease debit card or credit card spend) for another financial institution. The data shows that debit cardholders who experience a decline event are 2-7 times more likely to leave the credit union.

On the bright side, as shown in Exhibit 2, community banks and credit unions prevent more fraud than their larger peers. Credit unions should ask themselves whether the negative customer experience and attrition related to false positive declines is worth the 2-basis point improvement in fraud rate (i.e., is the juice worth the squeeze)?

In the next article in this article series, we will explore various strategies that credit unions can use to improve the performance of their authorization and fraud programs. We will discuss a valuation framework that can help credit unions objectively assess the costs and benefits of declining authorizations, an approach to managing the health of your authorization and fraud rules, and a member communication strategy that you can leverage to augment your existing authorization and fraud program.