For years, the payments industry has focused on detecting fraud after it happens. We invest in analytics, monitoring tools, and transaction scoring to identify suspicious activity as quickly as possible.

But there is another perspective worth considering: understanding the marketplace where stolen payment credentials are bought and sold.

Most people imagine cybercriminals as lone hackers operating in isolation. The reality is far more organized. Payment card data is collected through merchant breaches, phishing attacks, malware, info-stealers, skimming devices, and other techniques before being aggregated and offered for sale through underground marketplaces, carding forums, and encrypted messaging platforms.

In many ways, these markets operate like legitimate e-commerce sites. Buyers can search for cards based on characteristics that fit their intended fraud schemes, compare listings, and purchase stolen credentials from multiple sources. Entire ecosystems exist to validate data, establish seller reputations, and facilitate transactions.

For credit unions, understanding that ecosystem can provide valuable context.

When a member reports fraudulent activity, the compromise may have occurred weeks or even months earlier. By the time stolen credentials appear in an underground marketplace, criminals have often packaged, categorized, and distributed the information to potential buyers. The fraudulent transaction that eventually reaches the credit union may simply be the final step in a much longer chain of events.

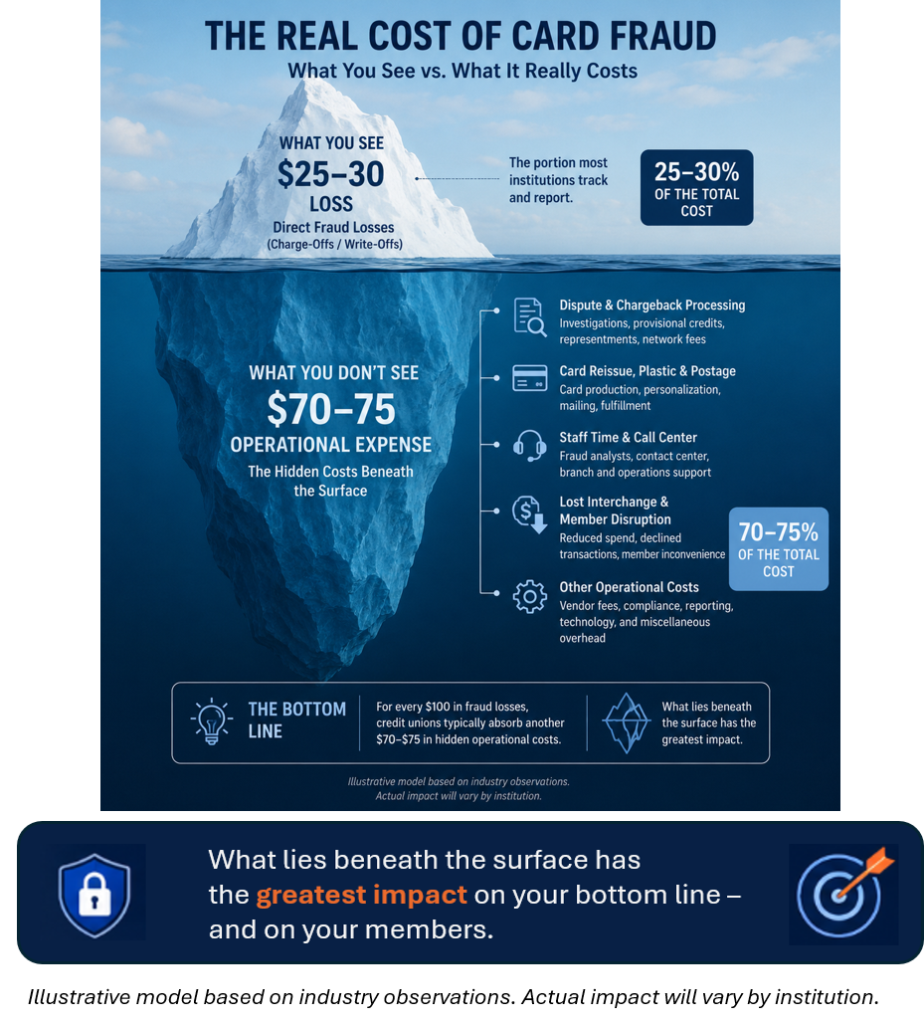

That perspective also changes how we think about fraud metrics. Charge-offs and reimbursement losses are certainly important, but they represent only one part of the operational impact. Card reissuance, dispute processing, member service calls, staff time, lost interchange revenue, and reputational damage all contribute to the overall cost borne by the institution.

Perhaps more importantly, understanding how payment credentials are acquired and monetized helps leadership ask better questions. How are our members' cards most likely being compromised? Which attack vectors present the greatest risk? Do we have visibility into emerging trends? Are we measuring success only by dollars recovered, or also by opportunities to reduce exposure in the first place?

Fraudsters continue to adapt their methods as payment technology evolves. Credit unions should be equally committed to understanding the environment in which those criminals operate. The better we understand the underground economy, the better equipped we are to make informed decisions that protect our members and strengthen the cooperative movement.

I'll be discussing these topics in greater detail during my presentation, "The Underground Marketplace: What Dark Web Intelligence Reveals About Credit Union Fraud Exposure," at the DCUC Annual Conference on August 4 in Aventura, Florida. If you'll be there, I hope you'll join the conversation. If not, I'm always happy to connect with fellow credit union professionals interested in better understanding today's evolving fraud landscape.

The fraud landscape continues to evolve rapidly, making ongoing education and information sharing more important than ever. To stay informed about emerging payment fraud trends and related industry insights, visit https://www.ariesfraudsolutions.com or follow Aries Fraud Solutions on LinkedIn at https://www.linkedin.com/company/aries-fraud-solutions/.