When credit unions think disruption, think beer

That might sound a bit odd, but it’s true. The disruption happening in the financial sector now, with neobanks, fintechs and e-banks – not to mention business development companies and private equity firms and real estate investment trusts on the commercial side – a lot is changing in the staid, conservative world of banking.

That’s where beer comes in.

No, not to drown your worries about being left behind in the fintech movement.

This is about coming to the realization that what is happening in the financial sector with fintech in all its many forms is just the next iteration of the trend toward digital productivity and customization that tech is spreading across all sectors of the economy.

And t’s most analogous to the challenges that CUs are facing moving forward.

The beer industry was run by a handful of large firms that dominated local and national markets. Size mattered. And it chugged along just fine, tweaking recipes to maintain margins and buying out smaller players in local markets – or forcing them out – to increase market share for stockholders.

It was a pretty straightforward model that worked well for decades since antiquated, Prohibition-era regulations created barriers to entry that kept upstarts and smaller players on the opposite side of the moat. The big players had only worry about themselves since none of them were interested in changing the status quo.

Then, craft brewers started popping up. The big players scoffed at them. I remember when the trend started a couple of decades ago, craft brewers represented 1% or 2% market share when Samuel Adams started getting press and broader distribution. Gnats in the grand scheme of things.

The big brewers did nothing about it. ‘Let them have their minuscule niches’ was the view from the boardrooms. As a matter of fact, the big players started to look for growth not downmarket but upmarket, eating their own. Huge mergers consolidated the beer market even more than it already was, now on a global scale.

That left local and regional markets open to smaller breweries who were taking advantage of tech-savvy brewers and more sophisticated logistics and marketing techniques. And more and more customers were being exposed to what beer could be when it wasn’t brewed by the accounting department of a multinational conglomerate. There were new levels of variety, quality, customer attention, and innovation for local customers.

It caught the monolithic masters of the brewing universe by surprise.

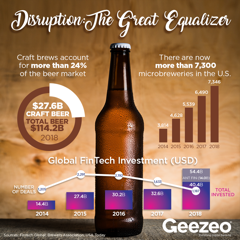

According to USAToday, craft brews now account for more than 24% of the $114 billion market. What’s more, beer sales year over year are relatively flat, yet craft brew sales grew about 5%.

They’re now the growth engine in the sector.

And now the big brewers are scrambling for growth by buying small brewers to get a piece of the action. The hubris of ‘bigger is better’ thinking has been disproven by technology.

Fintech is the same kind of disruptive force. Credit unions in this environment are sweating rising efficiency ratios and dwindling net interest margins as rates drop. But fintech is a way out, where the little guy can outmaneuver the big players.

Fintech provides credit unions with the same powerful tools that the big banks have and allows CUs to leverage their local knowledge and connections to local customers and businesses much better than larger banks.

So, when you read that next article on some new neobank or fintech, think about how you can use it to your advantage, don’t see it as a threat. And remember how craft brew Davids have put the Goliaths on notice.