In today’s world, consumers have a wide array of choices for everything including life insurance policies. In this article we will cover key differences between Whole Life (WL) and Indexed Universal Life (IUL) and understand how they work and further look at the pros and cons.

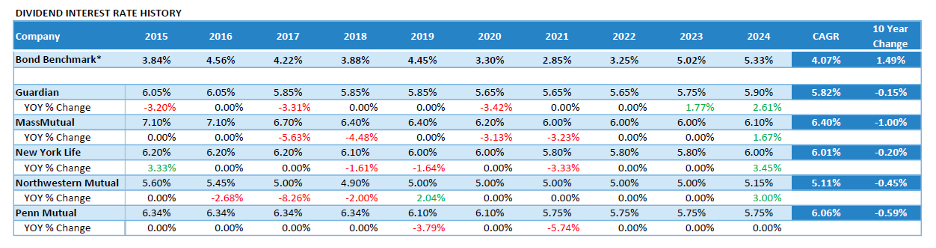

Whole Life (WL) Insurance: WL is considered the safest permanent policy. They are known to provide a guaranteed death benefit provided that the stated premium is paid on time. In retail setting, typically WL policies require premiums for the entire duration of the policy which is life expectancy. However given the need of permanent death benefit coverage in corporate settings, many life insurance companies have structured these policies with premiums over a shorter duration (8 pay, 10 pay, 12 pay, 15 pay). The WL policy has a guaranteed minimum growth (anywhere between 2% to 4% depending on the insurance company). The crediting on the policy’s cash values comes in the form of a dividend declared annually by the insurance carrier.

Below is the dividend interest history for a few top-rated carriers:

Indexed Universal Life (IUL):The policyholder gets an option to allocate all or part of their net premiums to a cash account which provides credits based on the underlying indexes (S&P 500 or another benchmark index). These indexes have a collar, i.e., floor which provides minimum crediting rate (0% or 1%), a cap which provides maximum crediting rate (for example 10%) and participation rate (typically 100%) which dictates how much percentage of the underlying gains you will receive.

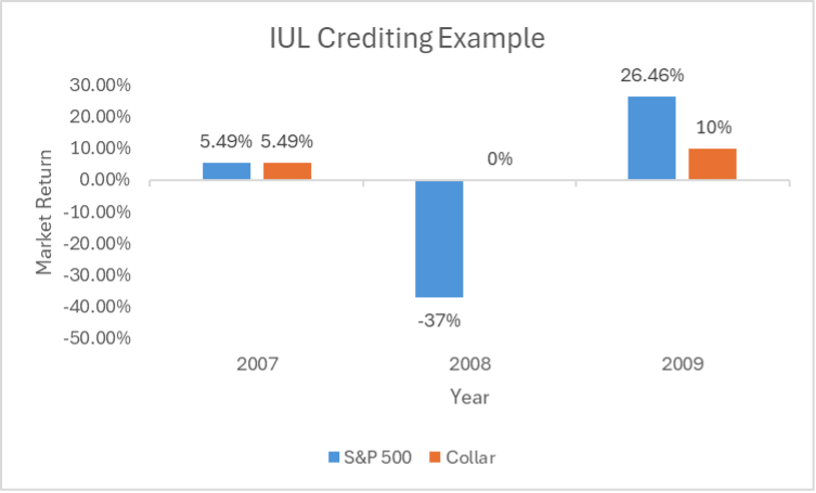

Below is an example of how much IUL policy would have received crediting through calendar years 2007, 2008 and 2009 if the policy had 0% floor, 10% cap and 100% participation rate.

As you can see that in this hypothetical index there will never be any negative returns as your floor is 0%. The trade-off for this guaranteed protection is sacrificing the gains that exceed the cap (10%). Depending upon the risk tolerance of the policy owner, this trade-off could make sense by lowering risk while providing for appealing cash value growth.

Conclusion

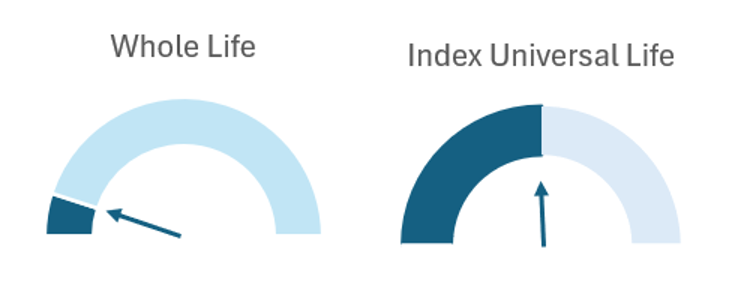

The decision to proceed with either WL or IUL should be based on your risk metrics and should factor in your specific circumstances and should be in consultation with your trusted financial advisor. Below is a risk spectrum for these 2 policies.

Modern Capital Executive Solutions is at your service to help you Recruit, Retain & Reward Top Level Talent. We offer unbiased consultation and extraordinary plan administration services while keeping your objectives and success in mind. Contact us today!