As financial institutions, we pursue an empowered consumer to be a part of their financial journey. Our key offerings include deposits, loans, and payments. We would like to be the primary or only financial institution for every consumer we serve but the competition we face is stiff.

The challenges we face include the burden of regulation, competition from larger financial institutions, and innovative services being offered via FinTech providers. What can we do to keep up with the innovation? How best can we engage and retain this consumer? How do we make ourselves attractive to new consumers?

Two things are certain -

- We have to design for the future, &

- We have no choice but to support retention and growth with our existing infrastructure.

Typical channels and associated transaction costs

| Channel | Cost/Transaction |

| Traditional Branch | $4-$7 |

| Express/Mini Branch | $3-$5 |

| Contact Center | $2-$6 |

| ATM | $0.75 |

| Kiosk | $0.34 |

| IVR | $0.20 |

| Mobile | $0.18 |

| Online | $0.12 |

Most initiatives in the past have focused on efficiencies where the consumer is being migrated to lower cost channels. This may not be the best solution.

Before we look at solutions keep three things in mind:

1 - Define the core functionality provided by each channel

- Branch – Branded locations to offer full-service to members

- ATM – A means for consumers to complete simpler financial transactions

- Kiosk – A self-service device to complete simpler non-financial transactions

- Online – A method for the consumer to transact from their home/office

- Mobile – A responsive application that caters to the consumer on the go

- IVR – An automated attendant that offers scripted answers

- Contact Center – A group of experts who are available to assist and serve the consumer

2 – Look at consumer experiences from other industries.

A stellar example to learn from is the airline industry. Over 10 years ago, Delta Airlines added a kiosk into their consumer service options. They trained their staff to assist consumers at the kiosk versus service from behind the counter. The idea behind this transparency was to train the consumer on the inherent “simplicity” of the transaction. Just three years ago when Delta introduced their app – the consumer realized the power of the kiosk (and more) within the app. This by itself has been transformative.

3 – Define ideal consumer journeys.

Keep in mind that it may not make sense to migrate certain journeys to lower cost channels. Your key to success is to balance convenience, self-service, and assisted/guided transactions.

The Future of the Transaction

The future will be device centric with the consumer leading the interaction. Transactions will be driven by the following elements:

- Security and Authentication

- Recognition and Personalization

- Machine and Human Cognition

- Simplified Transactions and Transaction Brokers

- Real-time Transactions and Instant Confirmations

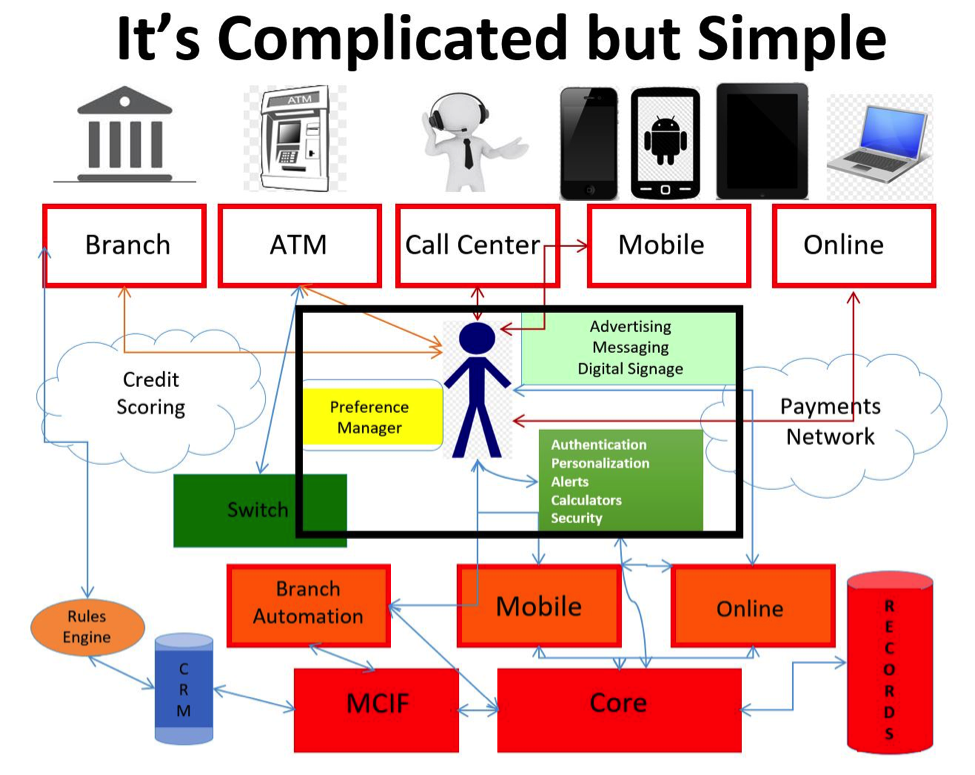

Your current architecture which looks like the image below will get even more consumer centric.

As you design for the future, here are three key takeaways –

- Your financial institution needs employees who are trained in multiple aspects of financial services and have the ability to serve as universal tellers/officers.

- The consumer is attached to their mobile device and your mobile app will be the key to your success – and also serve as a means for the consumer to contact you.

- Your future 2020 blueprint includes an employee whose training you continue to invest in; an employee that can help guide the conversation across channel.

(If you would like a detailed whitepaper on this blueprint strategy please send the author a note.)