Credit unions derive income from revenues generated by two primary sources: interest income and fee income. Interest income is revenue earned by lending money, and fee revenue is earned from account-based charges. Typically, interest income is associated with higher risks because it is subject to potential margin compressions, the risk of negative effects from internal or external forces on profitability margins when interest rates rise. Fee income is associated with lower risk because it is thought to be more consistent, predictable, and free from margin compression impacts.

When it comes to credit card programs, however, this rule of thumb is not always the case, and the risk associated with fee income could be higher than expected if the credit card program is not optimized. Many of the fee income lines, such as interchange or late fees, within the credit card Profit & Loss statement are tied directly to variable expenses. These variable expenses may move in unpredictable ways and can increase profit margin compression risks.

Credit unions must carefully weigh the options of choosing either a credit card program run in-house vs. one outsourced to a third-party agent provider and take into account the impacts of profit margins and variability of fee and interest income. Many seeking to minimize risk while still offering a competitive credit card product suite may choose outsourcing as the preferred method.

Interest Income

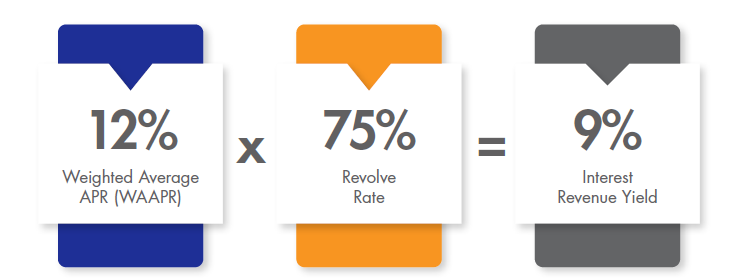

In the case of a credit card program, interest income is earned as a result of cardmembers borrowing money from the issuer to fund purchases. A credit card program’s interest income yield, or percentage of interest revenue on total balances, is determined by taking the weighted average APR (WAAPR), which is affected by whether the rate is fixed or varied based on an index, such as the published Prime Rate, and multiplying it by the Revolve Rate. The product of this calculation tells a credit union how much interest income yield they will earn based on any given amount of balances outstanding across all of the APRs within the credit card program.

Credit card portfolio balances are divided into two groups of cardmembers: those who pay down card balances in full each month (“transactors”) and those who do not (“revolvers”).The Revolve Rate is the percentage of total balances of cardmembers who are revolvers vs. transactors. The higher the Revolve Rate for the card portfolio, the higher the Interest Income Yield. A lower Revolve Rate will in turn result in a lower Interest Income Yield.

In addition, the WAAPR has a parallel impact on the Interest Income Yield. The higher the average APR within the portfolio, the higher the Interest Income Yield. The lower the average APR within the portfolio, the lower the Interest Income Yield.

Costs of Interest Income

Naturally, there are costs associated with collecting interest income that comes from a credit card program. Credit unions would be remiss to not consider the costs associated and how that may affect their program’s profitability in the short and long term. The two primary costs associated with interest income are the cost of funds and charge off reversals.

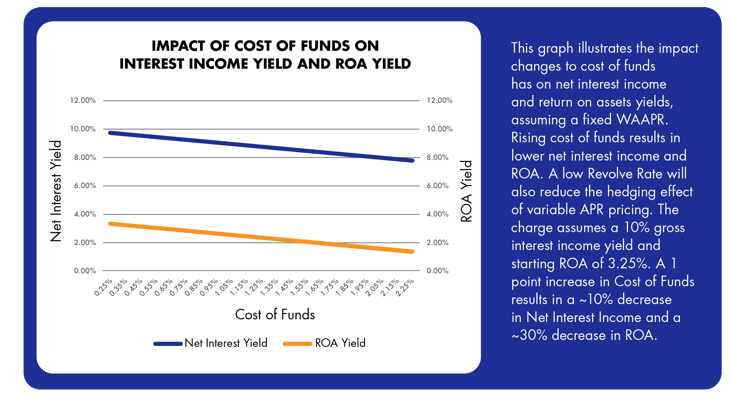

1) Cost of Funds: A credit card program’s cost of funds refers to the risk associated with the cost of funds. The risk is related to the average life/duration of the funding source and the relative movement of the cost in relation to the Revolve Rate. As alluded to previously, cost of funds for a credit card program also depends on whether the portfolio has a fixed or variable APR structure.

2) Charge-Off Reversals (Losses): Another cost related to interest income is charge-off reversals, which are balances unlikely to be collected due to the borrower becoming substantially delinquent. These balances must be accounted for as they may eventually become permanent losses for the credit card program.

Fee Income

Fee income is income earned by a credit union from account-related charges. It can be divided into two primary components within a credit card program: Direct fees and interchange fees.

1) Direct Fees: Direct fees are charged directly to the cardmember for a service, convenience, or to make up for a missed payment.

2) Interchange Fees: Interchange fees are paid by the merchant at which the credit card is being used. Interchange income is determined by the transaction volume and is often viewed as a low risk source of revenue. However, there are investments and expenses that are required to grow this revenue stream, so it may not be as low risk as it initially appears.

The most obvious investment to credit unions associated with products within the credit card program are the rewards offerings. Stronger rewards propositions within a credit card program result in more value to the cardmember, higher level of spend on the card, and higher portfolio growth over time (new account growth). In theory, offering higher rewards values on a credit card program results in higher spend and portfolio growth. The tradeoff is that rewards have a direct variable cost linked to the same driver as the interchange income: purchase volume. High value rewards programs such as a 2% cash back reward, will single handedly offset all interchange fees earned. Many cardmembers nowadays expect robust rewards from a credit card program, however that doesn’t change the fact that such rewards are costly for issuers.

Credit card issuing is a complexity of variable revenues and expenses that are driven by the overall card program’s product designs. More than one calculation must go into measuring card profitability. Whether it is interest income earned or fee income earned, many factors and assumptions introduce some form of risk to the bottom line. If the credit union does not get the card program’s formula right, profitability is lost and any value of card issuing becomes a burden to the overall enterprise.

How Elan Can Help

Elan recommends credit unions take a critical look at calculating their credit card program’s overall profitability. Credit unions should consider using third party resources to dive deeper into factoring in all expenses tied to managing the card program as they may be more extensive than the obvious costs. Also, it is important to weigh the risks of unsecure credit card lending by comparing the true income to other loan assets. Many credit unions find that the profits of self-issuing may not outweigh the inherent risks and hidden costs.

Partnering with Elan allows credit unions to optimize their credit card programs while mitigating risk and the various costs associated with running a credit card program, including those that may be not so straightforward.

At Elan, we take a two-pronged approach by delivering a high-value, digital-centric cardmember experience, while delivering to our partner a low risk, true income stream driven by a sound management style and proven growth strategy.

Learn more and read the full whitepaper“Evaluating a Credit Card Program’s Profitability: Fee vs. Interest Income.”