Many markets go through cycles and the loan participation market is no exception. When execution is favorable for sellers, it attracts more sellers to the market, which ultimately ends up lowering pricing. The same can be said for buyers, as more buyers enter the market, pricing goes up due to supply and demand dynamics. These cycles are mostly driven by interest rates which have cascading effects on the decisions institutions make when it comes to loan participations.

At a time when rates are coming off of their peaks, loans originated during the peak period will often be priced at relatively high premiums simply because they offer better returns than other current alternatives. The challenge we frequently run into is that buyers set arbitrary caps on the premium they are willing to pay, limiting their options on the buy-side. To be sure, high premium pools do come with their own risks, mainly prepayment risk, but it’s key for participants to look at the entire picture, not just a single number when making their purchase decision.

Price/yield relationship

We will first start with a basic concept in fixed income which is the relationship between yield and price. As yields go down, prices go up, and vice versa. As an example, let’s say you own a 8% fixed rate auto loan. That loan will be worth a lot more in an environment when benchmark yields (alternative investments) are offering yields of 3% than when the benchmark is at 6%. Assuming the loan carries an annual loss assumption of 50bps and loss-adjusted spreads are at 150bps, the price in the 3% environment would be roughly 106% while you would only get 100% in the 6% environment. The rough back of the envelope math is that you take the difference in the benchmark rates and multiply it by the duration of the product, roughly 2 for auto loans. This of course assumes that credit risk and loan spreads have remained the same while benchmark yields have changed, which is unlikely.

In the scenario outlined above, if you are able to purchase the 8% auto loan at a price of 105%, when benchmark yields are at 3%, your relative value is greater than buying the loan at 100% when benchmark yields are at 6%, despite the difference in premium.

Prepayment risk

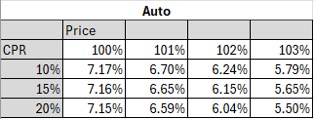

One of the main concerns with paying a high premium, is the risk associated with higher than expected prepayment rates. The higher the premium, the larger the impact of higher prepayment rates on the yield. Below is a table which shows the yield on a given auto pool across different prices and prepayment rates.

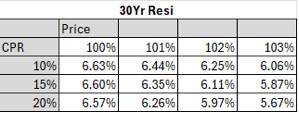

As can be seen, the impact on the yield between a 10% and 20% CPR on a 101% premium pool is .11%, while the impact at a 103% price is .29%. Further, as the CPR increased, the impact of the premium on the yield is magnified. For example, the impact on the yield between a 101% and 103% price at 10% CPR is .91%, while the impact at a 20% CPR is 1.09%. This is because the higher prepayment rate shortens the WAL. Taking that concept one step further, we will look at the same table but for a longer term pool such as a mortgage.

Given the longer term of the mortgage pool, it is less sensitive to changes in premium but more sensitive to changes in prepayment rates than the auto pool.

Convexity

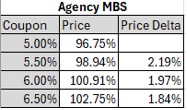

The relationship between price and yield is not always linear, which is where convexity comes into play. This is easiest to see with a mortgage pool where the borrower has the option to refinance their mortgage and is likely to do so should rates drop. As a buyer of a mortgage pool, you are taking on asymmetric risk, since the loan will likely prepay when rates fall, capping your income potential. Because of this, as the coupon on a given pool increases, the margin increase in premium decreases. As an example, let’s take a look at the pricing for agency MBS.

Putting it all together

What this means for you depends on if you are a buyer or a seller.

As a buyer, we often see buyers with sticker shock at a high premium pool, a 104% price as an example, without considering the yield at which those assets are being offered. Generally, a high premium pool will be offered at a higher yield than an equivalent pool with a lower premium but a higher servicing fee. The reason for the high premium might be related to the origination cost of a given product. Relatedly, some buyers push back when a pool is offered at a relatively high servicing fee, 250bps as an example. Generally the reason for the high servicing fee is because we are minimizing the premium, and therefore prepayment risk, in order to improve marketability. With the higher servicing fee, the seller is sharing in the prepayment risk. Further, as with the premium a higher servicing fee might be related to the high servicing cost for a given product.

As a seller, it’s important to note that better execution is generally had when premiums are lower. This does not mean that the total return needs to be muted, rather some of the gain should be moved to servicing spread. As an example, instead of listing a pool at a 106% price with 25bps of servicing, it can be listed at 103% with 175bps of servicing, for an asset with a 2 year WAL, those will be roughly equivalent returns to the buyer. Pricing with the lower premium and higher servicing, still allows you to generate a higher total return and improve marketability as it will ease the buyer's concerns over prepayment risk.

The big picture is that both buyers and sellers should not simply focus on the premium of a given pool but look at the total return. For a buyer, a higher premium pool might make sense if the yield compensates you for the prepayment risk. As a seller, selling at a lower premium might end up in a better total return as you will be able to make up the loss in premium with a higher servicing fee and better overall execution.

LoanStreet Inc. is the leading platform for loan sharing, reporting and analysis. To see where the latest deals are trading, register for the LoanStreet marketplace.