Mortgage production approached $2.0 trillion at year-end 2018 and credit unions accounted for $142.2 billion of that total. This data was derived from the recently released Home Mortgage Disclosure Act (HMDA). The balances include closed-end purchases, refinances, and home improvement loans, as well as open-end lines of credit – a new category mandated by HMDA for 2018.

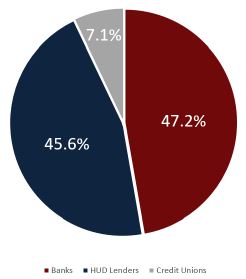

Banks and HUD lenders (mortgage finance companies) held 47.2% and 45.6% of nationwide loan origination balances, respectively. While credit unions originated 7.1% of mortgage origination volume, they captured 12.3% of the market when looking at the total number of loans, showcasing the credit union difference in supporting local members.

As borrowers locked in lower rates throughout last year’s rising-rate environment, purchases made up 61.8% of all mortgages originated in 2018 – over $1.2 trillion. Among credit unions, purchases made up a smaller portion of total loans (51.9%). Credit unions showed strength in the “relationship-based” lending categories of refinances, home improvement, and “other”, comprising 31.6%, 8.7%, and 7.7% of their origination volume, respectively.

“As rates ease in the back half of 2019, credit unions are well positioned to take advantage of shifting demand for these non-purchase loans,” said Sam Taft, AVP of analytics and business development at Callahan & Associates.

Additional data collected during the 2018 HMDA data cycle indicates whether a loan went to purchase a principal residence, secondary residence, or investment property. Principal residence loans made up 79.0% of the national total, with credit unions originating almost 92% of their mortgages for primary residences.

“With the new HMDA rules for open-end loans, more insight was provided for credit union real estate lending and a more complete picture was painted on how credit unions impact the mortgage industry,” Taft said. “These loans are disproportionally weighted towards members with existing relationships, which is a credit union specialty.”

Callahan & Associates analyzes the more than 15 million HMDA data points using Mortgage Analyzer. Callahan scrubs, aggregates, and processes the data delivering an effective, efficient, and contextual platform for understanding mortgage markets and opportunities. Mortgage Analyzer also provides market intelligence on non depository institutions such as online and non-traditional retailers.

For more information about credit union mortgage data or Mortgage Analyzer, contact Nicole Sanders at nsanders@callahan.com.

Market share of $ Organizations.