Editor's Note: CUInsight is hosting a free webinar Wednesday, December 3, 2025 titled, “From engagement to growth: How credit unions can win the P2P game”. We hope you’ll join us! Register here.

Today, members expect to move money in seconds, not days. Consumers are abandoning checks and cash in favor of digital payments at a rapid rate, with digital wallet usage soaring from 56% in 2022 to 85% in 2024, according to the Accenture Technology Reinvention Survey.

This growing expectation has fueled the rise of fintech wallets such as Venmo, PayPal, and Cash App. While convenient, each transaction routed outside of a credit union’s ecosystem represents more than a loss of interchange or fee income. It’s a missed opportunity to strengthen loyalty, deepen relationships, and retain deposits.

Fintech wallets have built success on frictionless design and social familiarity—instant onboarding, transparent confirmations, and effortless contact-based transfers. But what draws users in can also push them out: fragmented experiences, limited support, and disconnection from their primary financial relationships. Credit unions can combine the same convenience with something fintechs can’t replicate: personal trust and member advocacy.

The impact of P2P

P2P drives engagement, protects deposits, and positions credit unions to deliver value beyond basic transactions.

- Member engagement rises: A Curinos study found that members who use Zelle® conducted, on average, five more monthly debit transactions year-over-year vs. non-users.

- Revenue impact is measurable: The same study showed new P2P users generate an average of $25 more in annual revenue and make 3.2 additional interchange transactions per month than non-users.

- Deposits stay local: Financial institutions offering P2P report stronger balances and reduced deposit leakage to third-party wallets.1

- Businesses are adopting too: Datos Insights’ survey of mid and large businesses Q3 2025 reports that one-third of U.S. businesses—even those with $20M+ in revenue—are already using Zelle® for disbursements, signaling an untapped opportunity for credit unions to serve small business members.

Small businesses are also reshaping the P2P landscape. For many SMBs, instant payments are a lifeline for cash-flow management and customer satisfaction. Credit unions that extend P2P services to their business members can capture new revenue, reduce deposit leakage to fintechs, and position themselves as trusted partners in everyday business operations.

Unlike fintech apps, credit unions can also offer something most P2P users crave but rarely get: accessible human support. If a transaction issue arises, members know who to call, and that familiarity builds trust. With P2P integrated into the credit union’s own digital experience, members gain the same speed and ease as third-party wallets, plus the reassurance of real accountability and resolution.

The risk of falling behind

For many members, especially younger generations and SMBs, the availability of modern payment alternatives is now a deciding factor in where they bank. Datos Insights found that 42% of businesses have already switched financial institutions to gain access to faster payments. And Cornerstone Advisors estimates that more than $2 trillion in deposits have already flowed to fintechs providing digital savings and payments services. These shifts are a clear indication that credit unions need to pay close attention to their payments strategy.

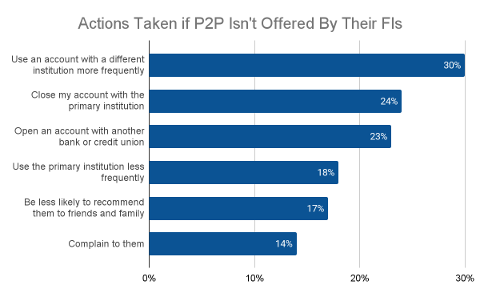

P2P is also a strategic defense. As fintechs and wallets compete for attention, not offering a seamless P2P experience creates real churn risk. In one survey, three-quarters of consumers said they would take action—open an account elsewhere, reduce usage, or switch providers—if their primary financial institution did not offer P2P. The actions included:

P2P opportunities

P2P is not just about money movement. It’s about relationships. Each time a member uses their credit union’s app instead of a third-party wallet, they reaffirm trust in their institution. Beyond member convenience, P2P offers credit unions measurable business upside. Research shows that members who use Zelle tend to have higher engagement and higher deposit balances than non-users.

Because every P2P transaction happens inside the credit union’s environment, there is a greater opportunity to cross-sell loans, cards, or other services when members are interacting frequently. Credit unions that embrace P2P not only protect deposits but also position themselves as the center of their members’ financial lives.

For a deeper discussion on how credit unions can win the P2P game, join the upcoming webinar:

From engagement to growth: How credit unions can win the P2P game

December 3, 2:00 PM ET

Hosted by CUInsight, featuring Matt Kinne (Zelle Network®, Early Warning) and Mark Majeske (SVP, Faster Payments, Alacriti).

1. Source: Curinos, “Zelle® Usage Drives Customer Engagement,” Dec 2022; Early Warning, “Zelle® CMA Sunset Brief,” Q1 2025.

Zelle® and the Zelle® related marks are wholly owned by Early Warning Services, LLC and are used herein under license.