Early in my career, an Air Force Colonel once told me: “There are few lessons learned and many that are merely observed. If you want to succeed in our Air Force, you need to apply what you learn and ensure you never repeat your mistakes again.” He was 100% correct. Years later, as a senior officer, I found myself passing on the same wisdom to junior officers under my command. Today I see the same principle in the credit union industry.

Here is the distinction between lessons learned and lessons observed:

Lessons learned imply that people will apply knowledge gained from experiences that will improve future actions by making the necessary changes.

Lessons observed are insights noted from past events that have not necessarily been acted upon or implemented and often lead to the same mistakes or results.

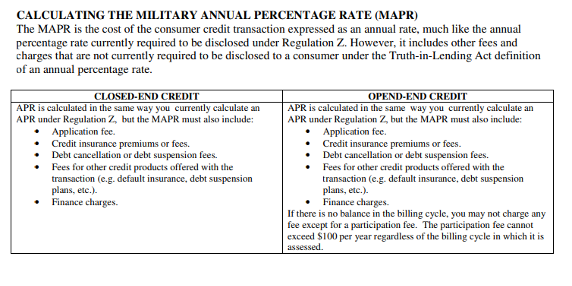

Hold that thought. The Military Lending Act (MLA) was enacted in 2006 to protect military personnel from predatory lending practices. It was the first federal law to impose a cap on interest rates for certain types of consumer loans to active duty servicemembers and their dependents. It significantly differs from interest rate calculations under Regulation Z and established a Military Annual Percentage Rate (MAPR) that was capped at 36% with fees and finance charges in the formula.

For example, using MAPR calculations, even the NCUA’s Payday Alternative Loan is off limits to military borrowers for small dollar lending unless you increase the loan amount or length of the loan. This essentially wiped-out small dollar lending for military borrowers.

Where do you think military members obtained small, short-term loans for emergency situations? Look outside the gate and you will find an abundance of payday or title loan companies and pawn shops ready to loan in excess of the amount needed or find innovative ways to secure the loan.

To be honest, I have never been a fan of the Military Lending Act for this reason. Making things worse—the law only applies to military members who are systematically discriminated against when seeking to obtain any loan products for small dollar requirements.

However, the MLA did not apply to credit cards. So, for those who qualified at higher interest rates, using a credit card to pay for emergencies and other expenses became the norm.

In 2015, the Department of Defense (DoD) issued a final rule that expanded the protections under the MLA which included credit cards and other types of loans. This forced credit card issuers to revamp fees, terms, and other conditions for a credit card offered to military members or many cases, disqualifying a covered borrower from opening a credit card account.

DCUC expressed its concerns in a 2017 letter to the Department of Defense as they were issuing the implementing guidance at the time. That was when the rate was capped at 36% for banks (temporarily capped at 18% for credit unions per the Federal Credit Union Act).

Fast forward to today.

Many people are jumping on the bandwagon in response to the President’s statement that he will impose a 10% cap on all credit cards on January 20, 2026. While it remains to be seen whether the courts will allow this to happen, Congress has already started to work on legislation to back the President’s desire. Did we learn anything from the MLA or are we okay with high-risk borrowers being disqualified from opening a credit card account?

In December 2025, the Federal Reserve Bank of New York released results from their study and found that states that enacted low-rate caps ended up restricting access to credit for high-risk consumers while also failing to reduce credit stress. So, if the intent was to reduce credit stress, all those efforts to institute low-rate caps accomplished ended up forcing people out of the market. Are we learning anything yet?

Another finding was that those with risky credit were unable to find lower cost loans from banks and credit unions, as proponents of rate caps may have expected (whoops!). This indicates that high-risk borrowers sought loans elsewhere. It is easy to see why payday loan or title loan companies and pawnshops are located right outside the gate near military installations across the country.

Here is another quote: “The definition of insanity is doing the same thing over and over again and expecting different results.”

Remember, loan companies and pawn shops do not issue credit cards. So, perhaps we will see these types of lenders expand their operations at a place near you.

It is not enough to “admire the problem” and then “haul off and do nothing about it.” Credit unions and banks will need to speak up sooner rather than later.

If we cannot convince Congress this is a bad idea, then I guess Congressional leaders will end up fooling around with federally imposed interest rates while the rest of us find out “if the juice is worth the squeeze.”