While many credit union leaders have tried to build organizational profit models, few have succeeded in building a sightline on the real profitability of their member relationships.

Some have generalized, peer-level profitability, or average household profitability based on industry “standards.” Certainly few, if any, know what the “lifetime profitability” of their members truly is. And in fact, some leaders (and boards) have simply determined that it is wrong to identify or even discuss which members are profitable or unprofitable, lest they be treated unfairly.

That lack of relationship profitability insight threatens to hinder leaders during an especially vulnerable time: as margins are squeezed; capital ratios decline and lending is challenged amidst the pandemic and recession. If successful growth in the past decade has been covering this blind spot, we are now in a moment where data gaps like this can no longer be ignored.

A lack of understanding member relationship profitability is a major gap in managing both your product and financial performance. But even more importantly, it’s a lack of knowing much more about who your most engaged, loyal and impactful members are, and what you can learn and act upon to retain them, and move unprofitable members towards more profitable journeys – that help them improve their own financial health.

The data analytics insights in knowing that two members with very similar demographic profiles - and similar products are having vastly different cost and economic impacts to the sustainability of the organization and the overall membership is crucial to making more intelligent decisions ahead.

The reasons that many leaders are missing this key insight are layered and cross departments beyond even finance. Linking and normalizing the right data sets to build a relationship profitability model can indeed be challenging, difficult to analyze customized profit drivers, and even harder to visualize (without a robust Transfer Pricing Model and a business intelligence platform), to understand and act upon it.

But the over-arching context around profitability is also cultural: the subject of member profitability is still taboo within many credit unions. After all, the cooperative mission is not about maximizing profit, but about helping members and mutual benefit.

As a result, many credit union executives are surprised to learn that less than 50% of their members contribute any profit to the organization…often substantially less than half. Yet, managing the health of the membership overall, as well as helping to strengthen each member’s financial health individually (which is where most credit unions can shine), is the only path to fulfilling the cooperative promise of people helping people.

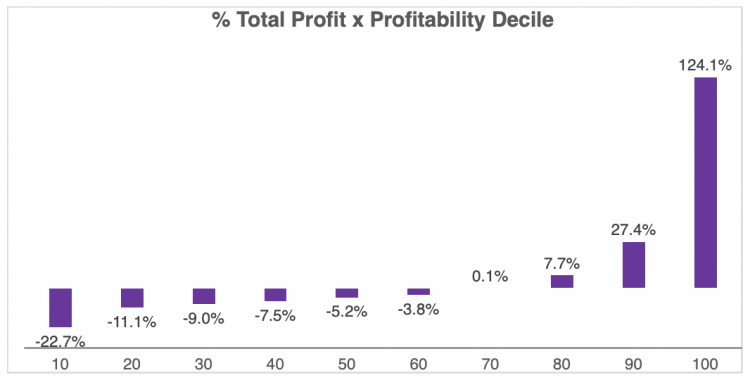

A recent example of this: for one credit union with a membership of just over 100,000, our analysis revealed that only 35% contributed positive profits to the credit union, and the 10% most profitable members were generating 124% of total profits. This, of course, means that about two out of every three members were draining profit away from the credit union – and this was before the pandemic and recession hit. Each institution will have its own unique results of a profit model application like this, of course, but these findings are not outliers by any means.

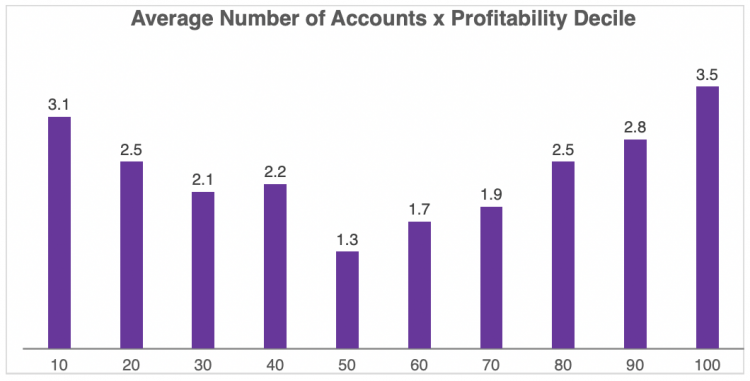

One common misunderstanding across many credit unions is to assume that those profit negative members are likely to be single-service. That leads to the logical response of focusing on adding accounts, any accounts to drive improvements. Yet, in this instance, the lowest profitability decile of members, which drained -23% of profits, had an average of 3.1 accounts, while the second highest decile which contributed 27% of profit had an average of 2.8 accounts. Clearly, adding or cross-selling products alone is not the full solution to improvements.

Indeed, a variety of different strategies for improving member profitability should be developed and deployed appropriately (more depth at “The Rising Need to Understand, Measure & Deploy Relationship Profitability.”) One of the most impactful is intersecting member-level profitability with a lifestyle segmentation growth strategy as well as leveraging insights from data-driven personas. Knowing your most active and growing contributors to product growth and relationship profitability is vital to retention, activation and even acquisition strategies.

Financial institutions have an incredibly high average cost per new member acquired between $200 to $1,200. Credit unions need high confidence, especially right now, that they are spending those precious marketing dollars attracting the right new members - who are most likely to build mutually beneficial and profitable relationships with the credit union in advance (and then immediately onboarding them effectively, but that’s deserving of an article all its own).

Accurate member profitability is an essential strategic business foundation to identifying where future opportunities exist, and how to generate increased revenues and financial results. As competition for your “best” members intensifies, and margins tighten, lacking this clarity – or worse, avoiding the conversation all together – is no longer an option to sustainable growth in 2021 and beyond.

To learn more about modeling and growing member relationship profitability, download Strum’s White Paper titled: The Rising Need to Understand, Measure & Deploy Relationship Profitability.