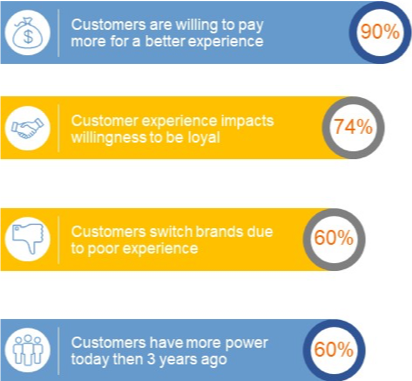

Client experience (CX) matters. It is a predictor of business growth. In the financial services industry, healthy member relationshipsgive businessesstaying power and renewed marketability.Happy members directly impact the bottom line and here are the numbers to prove it:

CX is not only about operational efficiency, emerging technology, user experience design or Net Promotor Scores; rather it is about turning the lens back onto the organization and determining what it feels like to do business with the institution. At its core, CX it is about putting ourselves in the shoes of a member. It is about gathering and analyzing data around what the member is saying. We do this to determine what they truly value, eliminating our biased internal hypothesis or assumptions. It is those biases – often overlooked – that are sometimes baked into the most fundamental assumptions we make as we start out on a CX journey.

In a highly commoditized industry, value does not only reside in the products and services a financial institution offers, but also in the way it delivers those to the consumer too. The effectiveness of the delivery is what defines client experience. CX is the cumulative effect and impression left on the member over time. Each time a member interacts with a CU, their experience may affect the outcome of that relationship. I use the word “may” to describe the effect on the outcome because not all touch points have the same weight or level of importance; they don’t leave the same imprint on the member. The experience related to remote check deposit most likely is not as important or significant in the overall relationship as applying and being approved for a loan. Ultimately when you think about the multitude of touch points with a member, whether it is a call, mobile app, website, or a branch, there are a select few that are known as “Moments of Truth”. These are points in the process that if not conducted to a member’s level of expectation, can lead to deep disappointment. These moments of truth can make the difference between someone continuing with an online process vs. abandoning it, using the CU as their lender or going to a competitor, referring your institution to a friend or not.

Many credit unions are pouring resources into transforming the customer experience. The results are mixed; this is understandable given the complexity of the journey. The good news is that regardless of the institution’s size or goals the elements that help define the CX transformation strategy are as outlined in Figure 2.

In order to devise an effective CX transformation strategy the above six elements need to be analyzed and understood. The insight gained from each element will need to be combined in order to determine major CX gaps, particularly in relation to your competitors and voice of members.

- Workflow Analysis – Get intimate with your processes – the devil will be in the details. On a macro level, all the processes in your CU can be grouped under 4 “journeys”: On-Boarding, Transacting, Administrating & Resolving. Each category of journey is comprised of processes: for example, “Onboarding” has distinct and separate workflow (process) for new accounts vs. loans vs. credit card. Under the journey of “Transacting” wire transfers, ACH, check deposit…all have distinct processes. The first step for workflow analysis is to determine the processes that have the highest impact on client experience. Based on our work with CUs a best practice is to develop an inventory list of all processes for each journey and prioritizing them based on volume, CX impact, and complexity. Once a process has been selected it will have to be documented in detail and critical operational data gathered in order to gauge its effectiveness level both from a member’s perspective as well as operational performance.

- Journey Mapping – While workflow analysis is focused on understanding process performance from an operational perspective, journey mapping is about looking at the process and resulting experience from a member’s perspective. Journey maps are to highlight distinct points in the process that leave deep impressions on the client – either delight or disappoint.

- Operational Data – Data provides context and helps with prioritization. Typical data that should be collected for process analysis includes: volume of transaction/request, cycle time (request initiation to completion), rework/reject rate, conversion % (submitted loans/closed loans), number of member contacts…

- Voice of Customer – Talk to them…they will tell you what they value. With all the data collection, analysis and mapping it is sometimes easy to forget about what the customer actually wants. The only way to really know what they want is by speaking with them. I am not talking about doing surveys, but actually calling them.Ensure that you have a good representation of the members you will interview: young, old, new relationship, long tenured, high net worth, early in career…

- Benchmarking – Go beyond banking for understanding what is shaping customer expectations. Companies like Google and Amazon are driving people’s behavior, so it may be more insightful to understand how other industries are using technology, data and culture to elevate client experience.

- Call Center Efficacy – Sometimes call centers are the closest you can get to understanding client’s level of satisfaction. Collecting and analyzing call center data can help determine why customers are calling in…have we not enabled them to self-serve? Escalations and disappointments – consider these gold. Most people will not tell you if they are unhappy, so if they take the time to call you, know that there is a problem impacting other members too.

In the end how will you measure the effectiveness of your CX transformation? Based on our in-person surveys of bank and credit union customers they are looking for three things: Simplicity, Transparency & Empowerment.

- Simplicity – Make the process easy and intuitive. Let me begin with ease and finish the process with success

- Transparency – Talk to me, let me know where I am in the process. Don’t let days go by without letting me know how my request is being handled.

- Empowerment – Give me the options to do business with you in the ways I want to – branch, mobile, web.

If your credit union collects and analyzes the data we discussed and structures the transformation to deliver to the expectations discussed above then you are on the right path. This is a long journey, with heavy reliance on c-suite support. Your culture will change, for the better. Your processes will become more streamlined, scalable and efficient. In the end you will be in better place both for your members and your employees.