The financial lives of Millennials--many of whom are now entering their prime earning years--have been shaped by one economic crisis after another. Coming of age during the Great Recession, millions of Millennials- myself included - saw their employment opportunities and, in some cases, their family’s savings and wealth, decimated alongside plummeting assets. The crisis of ‘08-’09 was supposed to be a once-in-a-lifetime economic event to overcome. But here we are ... again. The Covid- 19 pandemic has wreaked havoc on the U.S. economy, destroying millions of jobs, businesses, and livelihoods, and furthering the threat to long-term financial health for many Millennials.

It is easy to bucket us Millennials into one group based on our joint experiences, but it’s essential to understand the nuances within this generation; as employers, as community leaders, and as financial institutions. Millennials are a diverse group with different financial health needs. When disaggregating millennials, you will find that 14% of this generation is Black, 21% Hispanic, 6% Asian American, and 56% is White. We cannot consider Millennials to be a monolithic group.

Even with the growing diversity among this group, we are not immune to the financial health disparities based on race, geography, and gender that have been seen in other generations. For example, our research finds that Black and Latinx young adults have less savings, more debt, and are less confident in their ability to achieve long-term financial goals compared to their White and Asian American peers. Furthermore, the enduring racial wealth gap has denied Black and Latinx families the ability to build long-term opportunities for generations to come.

So how do you approach a group as diverse as Millennials?

See Beyond the Headlines

First, understand what they’re facing. Even amidst a global pandemic, the net worth of the richest Americans continues to climb while the bottom half struggles. The quick recovery from the pandemic- induced stock market plunge in March has benefited the most affluent households, while simultaneously displacing more than 40 million Americans who are currently out of a job. It’s reasonable to assume that the hardest economic fallout - especially for Millennials and people of color - will be realized over the coming months.

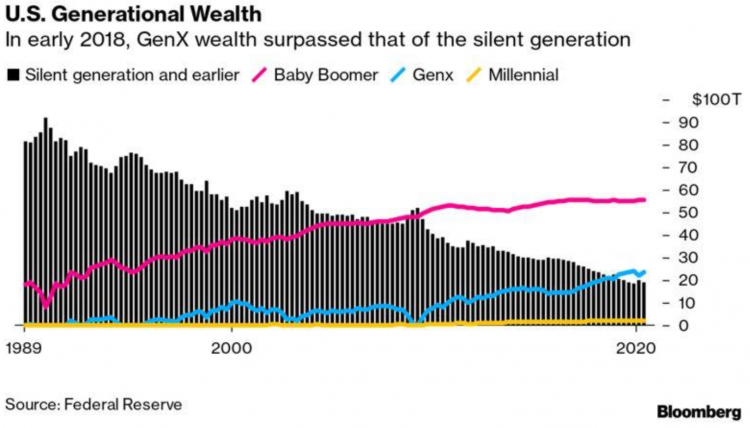

Broadly, Americans’ household wealth and savings rates have reached a record high as the highest- paying one-third of jobs have almost fully recovered from the recession. These topline numbers are misleading, however, as the top is pulling up the bottom, as opposed to the other way around. New data from the Fed takes a comprehensive look at the pandemic’s impact and disparities by age and race. As is often the case, younger people (i.e., Millennials) have less than their elders (i.e., Boomers), and the gap has widened. Given that Millennials are the largest workforce in the country (~72 million people), it is telling that they currently control less than 5% of the U.S. wealth.

Beyond the headlines, Covid-19 has magnified inequality. Job losses and the economic impact of the virus is having a disproportionate impact on younger people and people of color. Furthermore, Black and Latinx Americans are more likely to live in viral hotspots and face other social conditions that increase financial and physical vulnerabilities.

Help Close the Racial Wealth Divide

As noted above, Millennials represent the most racially and ethnically diverse group in the workforce. Decades of systemic racism have left Black and Latinx communities more vulnerable to the effects of crises like Covid-19. We see this vulnerability in the precariousness that characterizes the financial lives of many Black and Latinx young people and prevents these populations from generating sustainable income and building wealth. For example, Black millennial households earn about $0.60 on the dollar compared to their white counterparts. Black college graduates owe more student debt and are more likely to be unemployed. Their financial health needs require a unique approach.

Policymakers, business leaders, and communities across America have turned their attention to addressing issues of systemic racism and racial inequality, rightfully so. To improve Millennial financial health, we must get serious about closing the racial wealth divide.

Take a Stand for Financial Health Equality

We are at a pivotal moment in our country and younger Americans have been at the center of proposing change and driving more equitable opportunities for all. Millennials are accustomed to diversity. We have a heightened sense of connectivity and interrelationships between different kindsof people. We have been afforded the tools necessary to loosen our deep-seated prejudices and biases.

Millennial voices are being heard in all pockets of influence and our concerns with racial and wealth inequality need to be addressed. In addition to what is commonly instituted through DEI classes, this generation is pushing financial health equity forward and we’re drawn to organizations leading this charge. For credit unions, that means it’s time to lead.

Life choices, debt burdens, technology adoption, and expansive connectivity have shaped our lives in different ways. The oldest millennials are nearing 40, traditionally their prime earning years, yet many are struggling financially. Many are resistant to change. Many distrust the financial system.

Credit unions that want to engage Millennials must be cognizant of their diversity. A one-size-fits-all engagement approach will certainly fail. Credit unions that want more millennial members need to understand our unique needs. Segment the market and speak to me, not us. Build greater trust by embracing financial inclusion. Create more opportunities for those historically disenfranchised. And above everything else, be a financial health provider for all.