(February 24, 2014) -- Veteran card consultant R.K. Hammer has been writing about the need for the industry to invest in “value-based” pricing strategies for years. Here is their 2014 version.

While many card issuers are offering special cardholder price discounting – no fees, low interest and balance transfers to raid competitors – while raising the value prop none of these are new initiatives. Given the lowering of outstanding card loans which many have suffered during the recession, nearly $200 Billion total drop off before coming back up, we are surprised only that these and other value strategies weren’t implemented far more aggressively to reboot the card/payments business over the past five or six years.

This current round of price discounting has less to do with the economics, costs and pricing fundamentals of the business than it does with market share strategies by those card issuers who need to rebuild outstandings. That goes for large scale, medium size and small card issuers alike. Banks and CU’s, too. In our experience, which pricing strategy combination one uses determines how effective their marketing will be.

NOTES:

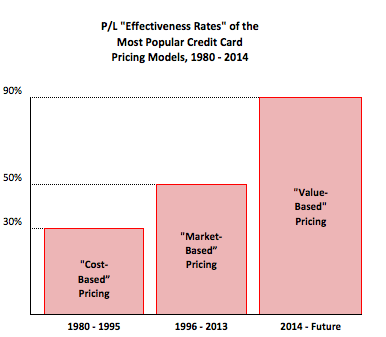

• The industry has gone through three primary pricing cycles in the past three decades: “cost”/”market”/& now “value-based,” each distinctly different from the others, with effectiveness rates equally different.

• Why would you use 1980’s cost-based pricing alone as your model today? It is a self-imposed set-up for outside intervention from regulators and others looking to implement influence on the card business model. Cost-based alone won’t get it. The same with market-based used alone; equally inefficient, compared to a value-based combination cardholder pricing methodology.

• The card industry must use a "Value-Based" pricing model which when combined with cost and competitive market models, is up to three times more effective to the P/L than earlier pricing models alone.

Effectiveness rates are the estimated value added to the card operation P/L as a result of a particular cardholder pricing model. It’s the payments space version of “blocking and tackling” – the basics.

Card ROA Volatile

Due to the high-risk unsecured nature of the credit card product and cautious consumers’ spending patterns, it is clear to many that you can’t make enough money on interest income alone to sustain profitability (which is already under competitive fire). Card profits, which are often described as “hefty” by some outside observers, are really not that high relative to the risk assumed, and in fact have fallen sharply over the past several years, from 4.25% ROA in 2008 to 2.10% in 2010; only in 2011 and 2012 has the card ROA finally risen to more normalized levels: 3.00% and 3.35% respectively, to 3.50% in 2013, and a R.K. Hammer estimate of 3.95% for 2014 Pre-tax ROA.

Twenty years ago, many issuers priced products on what we would call “cost-based” models; and ten years later, market-based pricing models. Cost alone, however, is only one component of establishing price. One reason industry profits have come under the gun lately is precisely due to that blind focus on costs to set prices, some of which have declined (cost of funds, for example, among others). This set up the industry for the recently unleashed attack on cardholder and interchange pricing, often citing lower/falling transaction/operating costs.

Pricing Model - Shifting Again- This Time, Finally, to “Value Based"

It has been our contention for many years that we should focus not only on costs or competition, but on the inherent value that the product delivers – what we term “Value-Based” Pricing. You cannot give away a valuable portion of your product mix and make it up in volume; yet that is what we’ve done for years with grace periods, limited use of transaction fees, enhancements and other un-priced components of the credit card business model.