The Honorable Rick Metsger, Chairman

The Honorable J. Mark McWatters, Board Member

National Credit Union Administration

1775 Duke Street

Alexandria, VA 22314

RE: Comments on NCUA’s 2017 & 2018 Budgets

On behalf of the National Association of Federal Credit Unions (NAFCU), the only national trade association focusing exclusively on federal issues affecting the nation’s federally insured credit unions, I am writing to you regarding the National Credit Union Administration’s (NCUA) 2017 and 2018 budgets. This letter is in support of NAFCU’s oral comments delivered during the Budget Briefing held October 27, 2016.

First, we believe public briefings and solicitation of comment on proposed budgets are an indispensable opportunity for the industry to provide thoughtful input on the agency’s expenditures. We applaud your efforts to provide such opportunities, and we look forward to this level of transparency and these practices being continued in the future.

This letter first discusses the continued increases in the budget seen in recent years. Next, it will focus on the recommendations contained in the Exam Flexibility report, and how such improvements should further mitigate cost. Finally, the letter concludes with a discussion of the budget planning process, NCUA’s plans to quickly refund the industry from the corporate crisis, and the agency’s plans concerning the equity ratio level.

A Runaway Budget is a Threat to the Safety and Soundness of the Industry

Every dollar spent by the agency begins as a dollar from a credit union and all NCUA expenditures have a direct impact on the daily operations of each credit union, no matter how large or small. Rampant increases in the operating budget not only take away from the viability of individual credit unions, but also will affect individual credit union members as well.

As NAFCU has repeatedly noted, prudent management of the agency’s operating budget is of paramount concern to ensuring a safe and sound credit union system. However, despite the fact that the credit union system is the healthiest it has been since the financial crisis, the agency continues to increase the budget. The proposed 2017 and 2018 budgets consider an increase for the ninth year in a row.

As NAFCU has stressed in previous discussions related to the budget, the entire credit union industry benefits by NCUA conducting its operations in a manner that is both efficient and expedient. While NAFCU cannot step in the shoes of the NCUA and is not critiquing the budget line-by-line, there are, however, some items that we believe require more scrutiny.

Budget has Nearly Doubled in less than 10-years

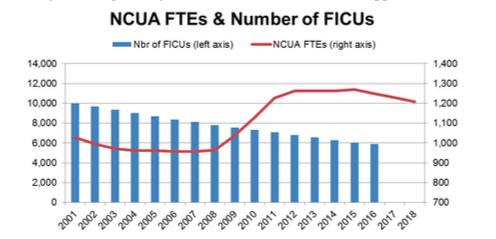

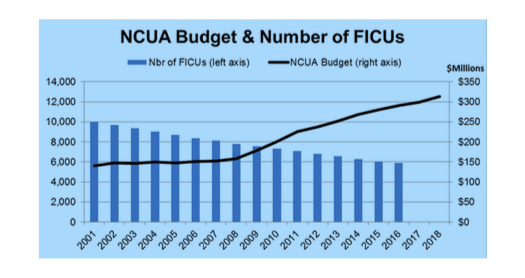

Most apparent, NCUA has increased its budget year-over-year since 2008, the biggest component of which has been pay and benefits. As the agency grew its FTEs1 to unprecedented levels during turbulent times, the budget rose in lock-step. This first started with the 2009 budget, where the agency authorized nearly 60 additional positions, including 50 additional examiners, bringing the total number of NCUA FTEs to approximately 1,020, the first time in history the agency crossed the 1,000 FTE mark.2 Also in 2009, the Board approved the 2010 budget which crossed the $200 million mark for the first time. It provided for an additional 75 positions, including 57 examiners. Perhaps most disconcerting, the annual budget hearing was suspended around that time, when stakeholder input was likely needed most.

For some context, the 2008 budget was $158.6 million, whereas the 2018 proposed budget is $313.1 million, nearly doubling in only a decade.3 While NAFCU can appreciate that NCUA had to build up its ‘war-chest’ during the financial crisis, the industry is no longer in that situation; the industry is healthy and in a time of relative calm. As such, NCUA should be winding-down expenditures rather than merely decreasing their rate of growth.

NCUA Expenses should Decrease as the Industry Continues to Consolidate

Over the last 10 years, the same time that the agency was doubling its budget, credit unions continued to suffer. First, they shared the financial pain of their members during the financial crisis, forcing many credit unions to merge or close outright. Then, in the immediate aftermath, a deluge of rules and regulations drowned many credit unions in red-tape, causing a further number to disappear. This has resulted in the loss of 1,900 credit unions, 25 percent of the industry.

Logically, it would seem the budget allocated toward supervising and examining credit unions would generally keep pace with the number of credit unions: the fewer credit unions around, the fewer examiners, and therefore, the smaller the budget required. Yet a reduction has not in fact occurred.

The agency has justified the increase in recent budgets with the industry’s asset growth, but it should not be entirely dependent on that factor. There should be economies of scale and cost- savings found from having fewer credit unions to examine, and more assets concentrated in fewer places.

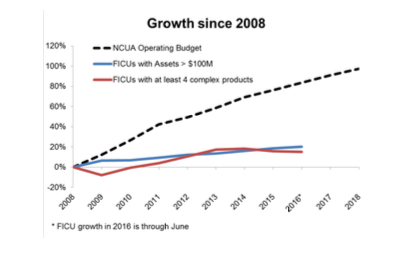

Further, size does not equate to complexity as the chart below shows.

Policy Issues, such as cybersecurity, should be addressed within current Budget Parameters

NAFCU recognizes that cybersecurity is an important concern for all prudential regulators; however, NCUA should update its cybersecurity examination procedures within the parameters of its existing budget. NCUA staff has testified that the current priority for enabling enhanced cybersecurity review is capacity building. NAFCU does not think that NCUA should attempt to retool itself as an expert cybersecurity regulator- in particular as to third parties- and working with other agencies has worked well to date. There are other agencies that already have the expertise and training to work with credit unions to improve cybersecurity practices, such as the Department of Homeland Security (DHS) and the National Institute for Standards and Technology (NIST), and NAFCU appreciates the NCUA participating in numerous interagency working groups. Working with other agencies is both cost effective and efficient.

Benefits from the Exam Flexibility Initiative Should be More Robust

The 2018 budget request for authorized FTEs will reflect a decline of 61 positions from a peak of 1,269 in 2015. The budget narrative explains that this reduction is due, in part, to the fact that examiners will spend less time at credit unions as a result of increased remote monitoring and pre-exam consultation. Clearly this is a move in the right direction, but these time-saving efforts do not appear to directly correlate or pass-through to budget reductions.

Additionally, while individual regional offices of examination are curbing their travel costs, these reductions are being offset by other offices that are substantially increasing their travel costs.4 For example, four offices budgeted more than double digit increases to their travel costs without clear explanation.5

Extended Exam Cycle

NAFCU continues to believe that an extended exam cycle for all well-run, low-risk credit unions would allow NCUA to better prioritize staff and resources, while still balancing risk factors and maintaining safety and soundness. The beneficial effects of an at least 18-month budget are already evident, as the agency’s 2017 and 2018 budgets contemplate a reduction in agency staff. Accordingly, the cost savings of extending an exam cycle to all well-run, low-risk credit unions above $1 billion should be examined and reported upon as it could materially decrease the agency’s operating budget.

Clearer and More Objective Exam Appeals

4 Although the FTE reduction for the 2018 requested budget from the 2017 approved budget decreases by 3.1 percent, the reduction in travel costs only decreases by 0.6 percent.

5 In the case of the Office of the Executive Director, the budget will increase over 200 percent in both the 2017 and 2018 budgets, going from $33,500 in 2016 to over $100,000 in 2018. While the absolute number of an increase is not significant, the rate of increase certainly raises questions.

When the exam flexibility working group solicited comments about the current exam process, one of the most common complaints submitted regarded lack of exam consistency. While the report recommended the implementation of an “optional exam survey,” NAFCU believes more needs to be done to correct for one of the biggest grievance our members are sharing about

NAFCU believes that an independent appeals process will help ensure timeliness, clear guidance and fairness, free of examiner retaliation, whether perceived or real. In its 2012 report, NCUA OIG7 recommended that NCUA establish a national reporting requirement requiring each regional office to regularly provide to E&I8 specific details on disputed examination issues elevated by credit unions to the Regional Director for a regional determination. The report stated that such a requirement could “include providing information on the number of elevated disputed examination issues, details about the disputed issue and the level of effort needed to resolve it at the examiner level, the outcome of the regional determination, and the length of time it took to close the disputed issue.” An independent review by a third party would help create an environment where a credit union feels it can raise an issue without fear of retaliation or affecting its examiner relationship. A third party review would also help provide a quality assurance check on examination results, and subsequently, hold examiners accountable for their findings. Most importantly, NAFCU believes that this process would lead to more efficient and less costly exams.

Cost Mitigation Efforts

NAFCU believes that the NCUA Board and staff are in a position to identify potential cost- saving measures that are not identified or explored in the budget, despite the fact that they may have been internally contemplated or considered. Though the final budget decision lies with the Board, a robust public discussion and industry feedback of major budget decisions is necessary.

Streamlined FOM Application process

As a potential cost-saving measure, NAFCU believes the agency should institute a streamlined FOM amendment application process, as we have repeatedly urged. Dozens of our members have expressed a latent desire to take advantage of modernized FOM rules, and in light of the agency’s actions during the October Board meeting, NAFCU anticipates a surge of FOM charter amendment applications. A streamlined and semi-automated approval process will be the only way for the agency to keep pace while keeping costs down.

Increase Collaboration with other Federal Regulators

NAFCU urges NCUA to take a more proactive role in collaborating with other federal regulators during the rulemaking process on regulations that are likely to affect credit unions. For example, just over the past year, the CFPB, DoD, and the FASB9 have each moved forward in promulgating rules that significantly impact our members. Unfortunately, many of these rules are redundant to other directives from the agency, or worse, improperly infringe on rulemaking authority congressionally granted to NCUA.

Relatedly, NAFCU commends NCUA’s recent letter to the CFPB in response to its payday rule. As proposed, the payday loan rule would alter important provisions in the agency’s PAL program, which was designed specifically to combat the types of loans and bad practices that the Bureau is trying to eliminate. We support NCUA’s resistance to unnecessary encroachment from other federal regulators, and encourage the agency to continue to take strong positions during subsequent interagency negotiations and rulemakings.

Cost Avoidance

Related to mitigating costs that are already present in the agency’s budget, NAFCU urges the NCUA to exhaust all efforts to avoid implementing any new costs that otherwise are not needed. For example, NAFCU believes that expanding the NCUA Board to five members, as has recently been discussed in other venues, would actually create more bureaucracy and costs for the industry. Moving to a five member board could pose challenges and create uncertainties. Recently introduced “Board Briefings” should help foster better communication between the existing board members, without warranting extra seats or costs.

Further Transparency on Planning and other Matters affecting the Budget

Regarding the agency’s move to a two-year budget process, NAFCU believes the burdens outweigh the benefits and the process is unwieldy. While a two-year perspective grants stakeholders a view of what might be on the horizon, NAFCU firmly believes that the Board should only vote to approve the immediately following year’s budget, and merely discuss or consider the subsequent year’s for context.

Reviewing two-years, but only voting on a one-year budget gives the Board more flexibility to quickly adopt to changing environments, and to not be held hostage to a budget that potentially was developed more than 14 months in the past.

Additionally, while NAFCU appreciates the opportunity to provide comment and input on NCUA’s strategic plan, we believe the plan would be better considered in tandem and concurrently with the agency’s operating budget. Because the strategic plan sets the agency’s goals, and the budget lays out what resources are used to achieve those goals, the two are intertwined, and should be treated as such.

Refund from the Corporate Crisis

NAFCU and our members would like to commend the NCUA Board on the final and full payment to the Treasury. Given this development and in light of the continued improvement of the U.S. economy and credit union industry, NAFCU believes it is imperative that the agency develop a concrete plan for the years leading up to the dissolution of the TCCUSF10. During this planning process, we strongly urge the agency to be fully transparent in its management of the TCCUSF, with the goal being an expeditious refund to credit unions.

No Share Insurance Fund Premium

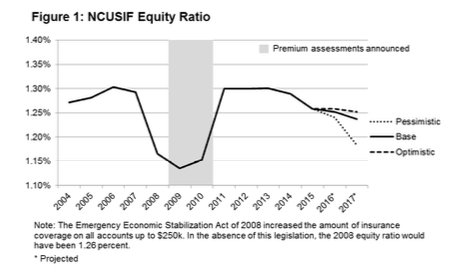

Directly related to the agency’s budget and operating fund, NAFCU restates our call for the agency to maintain the Fund’s current equity ratio for 2017. As shown in the chart below, NAFCU’s analysis has indicated that the Fund’s Equity Ratio will remain above 1.2 percent under base-level and optimistic predictions for 2017. Only under economic conditions mirroring the last economic recession would the Fund fall below the 1.2 percent threshold. While NCUA has the discretion to charge a premium to raise the equity ratio to the normal operating level, NAFCU believes that the NCUA should provide assurances as soon as possible to credit unions that it will not charge a premium unnecessarily.

Conclusion

Budget transparency has been a top issue for NAFCU and our members for nearly a decade, and returning to this budget hearing format is welcome. Ultimately, the NCUA Board still has the final authority to approve a budget and NAFCU and our members may disagree with how the NCUA is spending resources. NAFCU does believe in a strong independent regulator for credit unions and it is our hope and expectation that our perspective will provide the NCUA with helpful information. We believe new perspectives will lead to an even more effective use of resources. NAFCU looks forward to meeting with NCUA staff to discuss this letter’s recommendations.

Should you have any questions, please do not hesitate to contact me, or Carrie Hunt, Executive Vice President of Government Affairs and General Counsel at (703) 842-2234 or chunt@nafcu.org.

Sincerely,

B. Dan Berger

President and CEO

1 Full-time employees.

2 This is also around the time when NCUA moved from an 18-month to a 12-month exam cycle.

3 This is a 97 percent increase over 10 years.

4 Although the FTE reduction for the 2018 requested budget from the 2017 approved budget decreases by 3.1 percent, the reduction in travel costs only decreases by 0.6 percent.

5 In the case of the Office of the Executive Director, the budget will increase over 200 percent in both the 2017 and 2018 budgets, going from $33,500 in 2016 to over $100,000 in 2018. While the absolute number of an increase is not significant, the rate of increase certainly raises questions.

6 Although NCUA already has an appeals process in place, NAFCU has found that not many of our members use it. For example, our most recent annual survey found that although two-thirds of respondents believed their Documents of Resolution (DOR) were unjustified, only 9.1 percent of respondents reported that they had contested the results in the last five years.

7 Office of Inspector General

8 Office of Examination and Insurance

9 Consumer Financial Protection Bureau, Department of Defense, and Financial Accounting Standards Board, respectively.

10 Temporary Corporate Credit Union Stabilization Fund