Inflation rose just 0.4% in September from the prior month, contributing to a slowing trend that has prices just 3.7% higher than a year ago. Core inflation, which removes volatile components like gas and groceries, is up 4.1% over September 2022. The government also announced that Social Security benefits would increase by 3.2% in 2024 to help offset inflationary pressure for seniors on a fixed income.

With price increases moderating, the Fed held its benchmark interest rate steady in September, but left the door open for further increases later in the year.

Meanwhile, the labor market showed remarkable resilience in September, with the U.S. Bureau of Labor Statistics reporting that the economy added 336,000 jobs – much higher than forecasted. The unemployment rate held steady at 3.8% for the month.

In spite of these positive economic indicators, The Conference Board’s Consumer Confidence Index declined for the second straight month in September to 103.0. The Conference Board attributes the lower confidence rate to growing fears among consumers of an impending recession, along with lingering concerns with high prices – especially for gas and groceries – along with a tenuous political situation and high interest rates.

Overall, Co-op credit union portfolio data shows that September transaction volume rose by 4.2% in Credit and 0.6% in Debit on a rolling 12-month basis.

Co-op’s SmartGrowth team members are closely watching the following key spending trends this month:

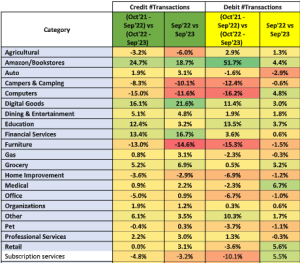

- Strong Year-Over-Year Results in Credit:Whereas September’s month-over-month spending was muted in both the Credit and Debit portfolios, Credit posted strong year-over-year results in several categories, including Amazon, Digital Goods, Education, Financial Services and Travel.

“We are seeing more everyday purchases moving toward eCommerce sites in general, and Amazon specifically,” says Ryan Prentice, Director, Consulting Services at Co-op. “This includes household essentials like groceries, cleaning supplies and toiletries.”

2. Education Spending Jumps in September: Whereas consumers completed much of their higher-education spending – including tuition, housing, textbooks and supplies – by the end of August, September saw a big increase in spending at the elementary level. Per Co-op portfolio data, spending in the Elementary category jumped by 58% in Credit and nearly 80% in Debit for the month.

“Elementary spending really carried the Education category in September,” says John Patton, Co-op Senior Payments Advisor. “Look for such spending to tail off through the remainder of the year, as back to school expenses and fees normalize.”

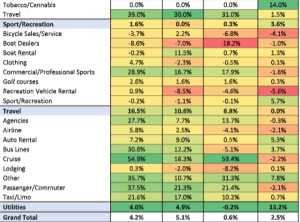

- Pre-recession Spending Shows Uptick:Among the big month-over-month risers in September were categories like Government Lottery Tickets, Government/Postal Services, Convenience Checks, Debt Collection, Employment Agencies and Bus Lines.

The common element among these merchant categories is that they are considered leading indicators of a potential recession – an alarming sign that the American consumer is facing stress. Much of that pressure is stemming from stagnant household income growth, which has lagged inflation over the past year. The result has been an increase in household borrowing, including more consumers dipping into their credit lines.

Of course, not all of these economic worries may come to fruition, as the Fed is betting on achieving an ideal “Goldilocks” scenario, where it is able to maintain higher interest rates over the next few years to moderate inflation, while still seeing steady economic growth in the form of low unemployment and solid consumer spending and GDP growth.

Credit Debt Continues to Grow:Year over year, Credit transaction volume continues apace, with 4.2% growth on a rolling 12-month basis compared with just 0.6% for Debit.Month over month tells a different story, however, as overall Credit transaction volumes declined by -5.7%, and Debit transaction volume fell by -3.3%, reversing a positive trend in both portfolios in August.

Despite this short-term decline, consumers are continuing to rack up credit card debt. Per Co-op portfolio data, credit balances grew by 14.18% from September 2022 to September 2023, including a month-over-month jump of 2.78% from August 2023. Post-COVID, this monthly increase in September balances is on par with prior years – average balance growth month-over-month in 2023 through September is 1.25% against a comparative .99% in 2022.

More telling may be the increase in average total balances through September from 2019 to 2023. In 2023, total average balances through September increased 6% over the same period in 2019, 12% over 2020, 25% over 2021 and 14% over 2022.

The combination of this growth in credit balances and high interest rates has JPMorgan Chase & Co., Citigroup, Wells Fargo and Bank of America preparing to write off large amounts of consumer borrowings in their portfolios. The country’s four largest banks are expected to report total charge offs of $5.3 billion in bad debt, double the charge from a year ago. According to data from Callahan and Associates, credit card loan delinquencies for all U.S. credit unions reached 1.54% in the second quarter of 2023, the highest rate seen in the past 10 years.

“Once consumers reach 35-40% of their credit line usage, their Credit spending tends to tail off dramatically,” said Patton. “They will switch to other lines, shift to using Debit or may curtail their spending completely.”

“The unprecedented combination of COVID stimulus packages that boosted cash-on-hand, double-digit inflation and a year of interest rate hikes has created a whiplash effect on many financial institutions, which are now struggling to adjust to large swings in their payment portfolios,” said Prentice. ”It’s more critical than ever to maintain consistent price and risk management to ensure the health of your program – and support your members’ financial wellness.”

Year-Over-Year Category Level Spending (Rolling Year Average, and Comparing September 2022 to September 2023)

What Credit Unions Should Do Now

With a potential recession on the way, members are growing increasingly concerned with their financial wellness. Credit unios are perfectly positioned to provide them with the help they need.

As credit unions begin preparing for 2024, they should consider updating their credit card program to include risk-based pricing. Also, plan to initiate regular cardholder account reviews and adjust credit lines and pricing as needed.

Considering the high credit balances that many members are struggling under, offering a balance consolidation at a low interest rate to qualified cardholders will create loyalty. And for those who are truly struggling to make ends meet, credit unions may wish to offer debt consolidation services, or a skip-a-pay to help them get ahead on their monthly obligations.

“Credit unions are well positioned to help their members with all of their financial needs,” said Patton. “During a time when purchasing a new home may be a stretch for many, home equity loans and lines can be leveraged to buy a car, finance needed home repairs or perhaps fund larger improvements like a new back deck. Members are also seeking advice on retirement planning, career changes and saving for their children’s college expenses. Credit and Debit are means to an end, but now is the time to focus on assisting members with navigating challenging economic waters and achieving their long- and short-term financial wellness goals.”

More information on the Co-op SmartGrowth Consulting Team can be found here.