The Uberized credit union

So many recent articles have talked about our need to “Uberize” credit unions. But how?

How can we disrupt an industry that has traditionally had little competition by facilitating mutually beneficial exchanges between people with existing assets and people who need them?

(Pauses for dramatic effect.)

(Waits for the stragglers to catch on.)

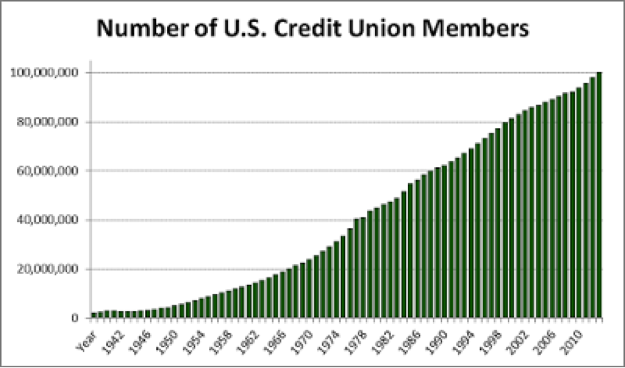

Credit unions were disruptive long before Uber was a sparkle in Garrett Camp’s eye. In fact, this chart in Google’s NGram viewer makes it seem as if the term “disruptors” was invented just for us.

Beginning in 1934, when the government finally allowed credit unions to compete with banks, it took credit unions just over 30 years to reach 50 million members. In today’s world this may seem slow, but consider it took the telephone 75 years to reach 50 million users, just over 50 years to reach 50 million US air travelers, and about 40 years to reach 50 million US car owners. For a modern reference, Uber has yet to eclipse even 10 million users worldwide in its 7 years of existence.

(Graph courtesy of Credit Union Resouces Inc.)

Credit unions were once the disrupter to banks what Uber is now to taxis, but our collective hustle to “Uberize” banking shows how far removed our industry is from those grassroots beginnings. In so many ways, we have become just another taxi brand waiting in line at the airport with the other assorted national and community brands, waiting for our turn to be called forward, and watching Simple, Venmo, Ally, Square, Lending Club, Credit Karma etc. bypass the line repeatedly to pick up fares.

The best way for credit unions to “Uberize” is to stop looking like the rest of the cabs. When is the last time someone passed on a taxi for a different brand of taxi? It happens all the time with Uber because the company is remarkably different in convenience and cost. In the same way, credit unions must present a remarkably different value proposition to bypass the line of banks. And while we may not be able to become more convenient than these newcomers due to the costs and risks inherent in doing so, we already offer better rates, and we’ve got a value proposition in our cooperative structure which cannot be emulated by competitors.

A differentiated credit union industry pays dividends, emphasizes member participation in annual meetings and other activities, provides personalized service, and participates meaningfully in the communities it serves. It delivers better rates, charges fewer fees, and conducts business in transparency. Most importantly, a differentiated credit union industry highlights member ownership as the primary point of differentiation.

When we repeatedly hear the myth that “nobody cares about the credit union difference,” it’s tempting to believe it and start to look for success in faster delivery channels, sexier apps, etc. And while emulating the quick growth of Uber by developing technology is enticing, we shouldn’t ignore the successful strategies used by one of the most powerfully disruptive movements in history: our own.