As the impact of COVID-19 continues to spread, it’s natural to feel anxious and concerned about your financial situation. In times like these, being proactive and smart about your money can make a big difference to your wallet.

While there are a number of precautions you can and should take, one of the best things you can do to prop up your finances (in addition to an emergency fund) is to lower your debt overhang - especially on credit cards. In turn, this could provide some much needed flexibility in the event you or a family member loses their job or has a medical emergency.

One of the most effective ways to do this is through the debt-snowball method, in which you pay off your smallest loan first, then roll that amount into paying off bigger loans — similar to a snowball gathering more snow as it rolls down a hill. This is a great method for families or individuals with multiple credit cards and loans, who may need quick access to funds.

What’s more, by taking advantage of the optimal interest rates on student loans, your recent government stimulus check, and reduced spending due to staying at home, you can quickly and easily start paying off your credit cards and loans. Here’s a breakdown of how the debt-snowball method works:

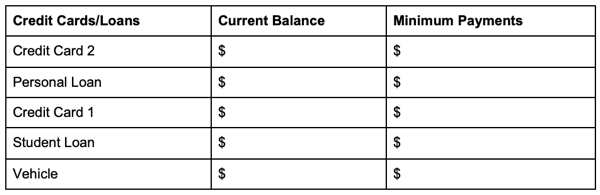

- Start by writing down all of your credit cards and loans (excluding your mortgage), including your current balance and minimum monthly payments, in the chart below:

- Now, arrange your credit cards and loans by current balance, from smallest to largest.

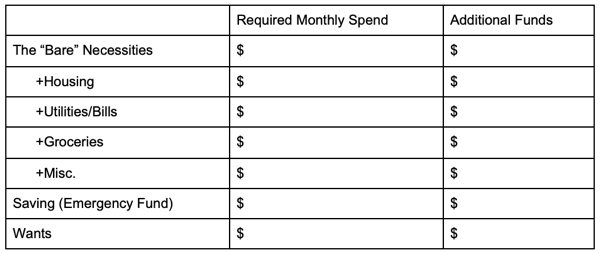

- Next, make a monthly budget to see how much extra money you can put toward your loans and credit card payments over the next few pay periods. We like the 50/20/30 method; although you should closely examine the “wants” section. Be sure to include any extra funds, like your government stimulus check or reductions in spending. Additionally, don’t forget to include a contribution to your emergency savings fund!

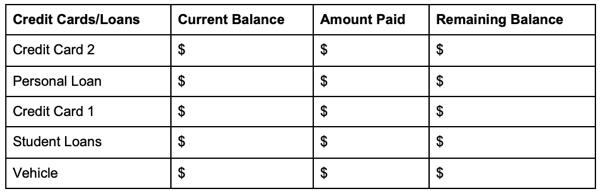

- This month, pay the minimum payment on all loans except the smallest. Put the extra money you budgeted for getting rid of debt toward your smallest debt — even if you are paying more interest on a different one. Calculate your remaining balance in the chart below:

- Once the smallest debt is repaid, take the entire amount you were paying toward it (monthly minimum, plus any extra money) and target the next-smallest debt. As you pay off each debt, divert all the freed-up money toward the next debt in line.

By front-loading your payoff plan, you can quickly free up your credit, while also giving you and your family some much needed peace of mind during this crisis. Plus, by tackling the smallest amount first it’s easy to stay motivated and on track.