Press

Credit unions boost lending, cut long-term investments in first quarter

NCUA Reports Loan Delinquencies Fall to Lowest Level in Eight Years.

ALEXANDRIA, VA (June 2, 2015) — Federally insured credit unions relied more on lending and less on investments to generate income during the first quarter of 2015, the National Credit Union Administration reported today.

“Credit unions are continuing to make the loans needed to grow local economies,” NCUA Board Chairman Debbie Matz said. “As a result, their members are buying houses and cars, and they’re paying for college to give young people a better start in life. At the same time, credit unions are curbing long-term investments. The switch from long-term investments to loans is decreasing interest-rate risk, a positive development for the credit union system as a whole.”

Auto lending was a major factor in the overall loan growth during the first quarter of 2015, while total investments declined from the first quarter of 2014. Membership, assets, deposits and net worth all continued to rise. Net interest margins held steady.

NCUA released the new figures today based on Call Report data submitted to and compiled by the agency for the quarter ending March 31, 2015.

Loan Balances Rise Nearly 11 Percent from First Quarter of 2014

Total loans at federally insured credit unions reached $721.9 billion in the first quarter of 2015, an increase of 1.3 percent from the previous quarter and 10.6 percent from the first quarter of 2014.

Over the year ending in the first quarter of 2015, loans grew across asset sizes and in every major category, including:

- New auto loans grew to $89.3 billion, up 3.4 percent from the previous quarter and up 21.5 percent from the first quarter of 2014.

- Used auto loans increased to $147.3 billion, up 2.5 percent from the previous quarter and up 13.2 percent from the first quarter of 2014.

- Total first mortgage loans outstanding reached $297 billion, up 1.6 percent from the previous quarter and up 8.9 percent from the first quarter of 2014. Fixed-rate first mortgage loans made up 59.3 percent of first mortgage loans outstanding at the end of the first quarter of 2015.

- Second mortgage loans were $71.6 billion, down 0.5 percent from the previous quarter and up 2.5 percent from the first quarter of 2014.

- Net member business loan balances grew to $52.9 billion, up 2.1 percent from the previous quarter and up 11.6 percent from the first quarter of 2014.

- Non-federally guaranteed student loans grew to $3.3 billion, up 4.3 percent from the previous quarter and up 15.2 percent from the first quarter of 2014.

- Payday alternative loans outstanding at federal credit unions were $30 million, down 18.2 percent from the previous quarter but up 29.9 percent from the first quarter of 2014.

The loans-to-shares ratio at the end of the first quarter was 73.3 percent, a slight decline from the previous quarter but 4.1 percentage points higher than the end of the first quarter of 2014.

Credit Unions Continue Shedding Long-Term Investments

Federally insured credit unions continued to move away from long-term investments in the first quarter of 2015.

Total investments were $280.4 billion at the end of the first quarter, a decline of 3.7 percent from the end of the first quarter of 2014. Compared to a year earlier, investments declined in all categories except those with maturities of one to three years, which increased 20 percent from a year earlier, to $107 billion. Investments with maturities greater than 10 years dropped 29 percent from the first quarter of 2014 to $5.3 billion.

Delinquencies, Charge-Offs at Lowest Levels Since 2007

Delinquency and net charge-off ratios for federally insured credit unions declined to their lowest first-quarter levels in eight years. The delinquency ratio fell to 69 basis points from 81 basis points at the end of the first quarter of 2014. The net charge-off ratio declined to an annualized 47 basis points year-to-date from 50 basis points at the end of the first quarter of 2014.

The percentage of loan charge-offs due to bankruptcy in the first quarter was 16.9, 137 basis points below the end of the first quarter of 2014.

Credit Union Membership Nears 100 Million as Consolidation Trend Continues

Membership in federally insured credit unions grew to 99,969,794 at the end of the first quarter of 2015, an increase of more than 2.8 million from the end of the first quarter of 2014.

The number of federally insured credit unions fell to 6,206 at the end of the first quarter, 285 fewer than at the end of the first quarter of 2014, a decline of 4.4 percent. The decline is consistent with longstanding trends in the financial services industry.

Credit Unions Post 21 Consecutive Quarters of Positive Net Income

Year-to-date net income for federally insured credit unions was $2.2 billion in the first quarter, an increase of $119 million, or 5.7 percent, from the first quarter of 2014. As a whole, federally insured credit unions have recorded positive net income for 21 straight quarters.

Return on Average Assets Steady

Federally insured credit unions’ return on average assets ratio stood at an annualized 78 basis points at the end of the first quarter, a decline of two basis points from the previous quarter but the same level as the first quarter of 2014.

Net Worth Ratio Up for the Year

The aggregate net worth ratio was 10.81 percent at the end of the first quarter, up 20 basis points from a year earlier. The ratio declined 15 basis points from the end of the fourth quarter of 2014, consistent with first-quarter trends.

Credit Unions Remain Well-Capitalized

The vast majority of federally insured credit unions remain well-capitalized, with 97.5 percent reporting a net worth ratio at or above the statutorily required 7.0 percent. At the end of the first quarter of 2014, 97.0 percent of credit unions were well-capitalized. As of March 31, 2015, less than one percent of federally insured credit unions were undercapitalized.

Assets and Shares Grow for the Quarter

Total assets in federally insured credit unions grew to $1.16 trillion at the end of the first quarter, an increase of $60.6 billion, or 5.5 percent, from the end of the first quarter of 2014.

Overall, share and deposit accounts at federally insured credit unions rose $41.3 billion from the end of the first quarter of 2014 to $984.4 billion. Rate-sensitive money market accounts rose by $7.4 billion from the first quarter of 2014.

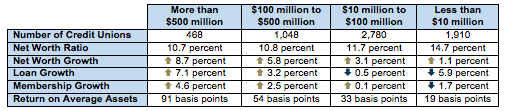

Larger Credit Unions Continue Strong Performance

Federally insured credit unions with more than $500 million in assets continued to lead in most performance measures in the first quarter of 2015. With $817.1 billion in combined assets, these 468 credit unions held more than 70 percent of total assets at the end of the quarter. They also reported a higher return on average assets than credit unions below $500 million.

Credit unions with assets of less than $10 million recorded a slightly higher net worth ratio overall, but loan and membership growth were both negative in the first quarter.

The table below provides a summary of federally insured credit unions’ current ratios and growth during the first quarter of 2015 by asset size for selected metrics:

For more information about the performance of federally insured credit unions, NCUA makes the complete details of the March 2015 Call Report available online here. A summary of first-quarter performance is available here, and financial trends data for federally insured credit unions are available here.

For more information about the performance of federally insured credit unions, NCUA makes the complete details of the March 2015 Call Report available online here. A summary of first-quarter performance is available here, and financial trends data for federally insured credit unions are available here.

NCUA is the independent federal agency created by the U.S. Congress to regulate, charter and supervise federal credit unions. With the backing of the full faith and credit of the United States, NCUA operates and manages the National Credit Union Share Insurance Fund, insuring the deposits of nearly 100 million account holders in all federal credit unions and the overwhelming majority of state-chartered credit unions. At MyCreditUnion.gov and Pocket Cents, NCUA also educates the public on consumer protection and financial literacy issues.