2019 mid-year review: Rates, deposits and their effect on financial institutions

The first half of 2019 was interesting on multiple fronts. After growing approximately 3 percent in 2018, GDP entered the first quarter of 2019 at a strong 3.2 percent. However, according to the Atlanta Fed’s GDPNow forecast, second quarter GDP is estimated to be substantially lower at 1.6 percent.

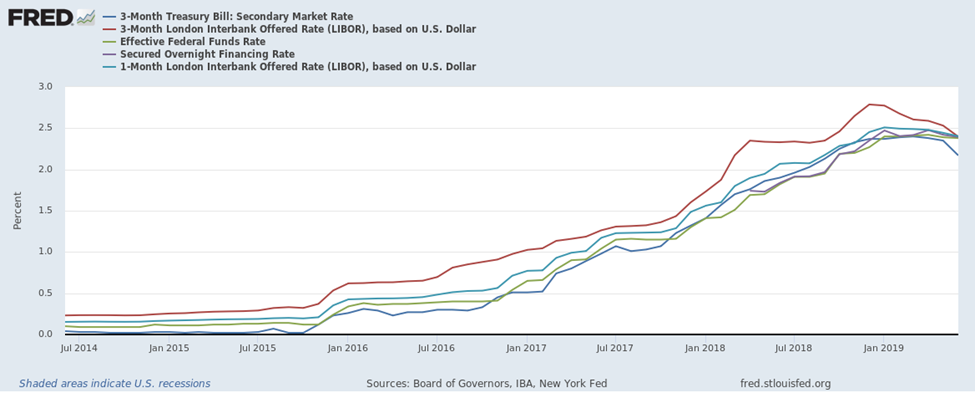

Unemployment and wage gains remain strong, along with consumer spending and business confidence, but headwinds from slowing global economic growth and continued trade tensions are forcing the Fed to change course. After four years of rate increases, the Fed is expected to deviate and cut rates one to two times throughout the remainder of 2019. This would result in the effective fed funds rate at sub 2.00 percent. Figure 1 below provides a historical view of the current rate cycle comparing effective fed funds to other market indicators.

Figure 1

Interest rates remained the hot topic throughout the first half of 2019. Most notably, President Trump (in Trump-ian fashion) tweeted on multiple occasions about his displeasure with the Fed for perceived unnecessary rate hikes. Since 2016, the Fed raised rates eight times in a bid to meet its dual mandate of maximum employment and stable prices (i.e. 2% inflation). With uncertainty about how the Fed may react to pressure from the markets and executive branch, the general interest rate market is experiencing significant volatility. Market rates such as 1 and 3 Month LIBOR have fallen by 10bps and 37bps respectively throughout the first half of the year (see Figure 1). This is due to the perceived notion that the Fed would continue modest rate increases in 2019, but consequently has diverted in a different direction. Volatility in these market rates are making it difficult for financial institutions to effectively price loans and deposits. The result is increased pressure on margins as cost of funds increases, while yields on loans are decreasing (see Figure 2 below).

Figure 2

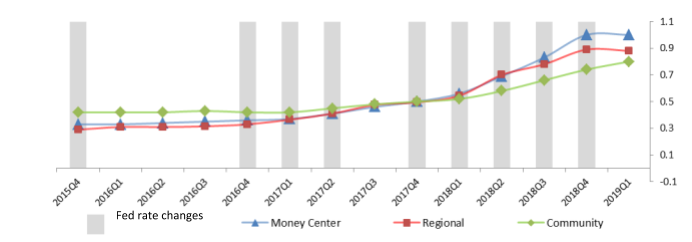

Figure 2

In 2018, a majority of financial institutions experienced an increase in their cost of funds as rate increases incentivized depositors to seek higher returns. However, during the first quarter of 2019, money center and regional institutions began to see marginal decreases in their cost of funds, while community-sized financial institutions experienced increases. This stems from several factors. Larger financial institutions using market based indices like LIBOR experienced a decrease in cost of funds, as those rates began to fall in anticipation of Fed movement. However, most community-sized financial institutions that are utilizing Fed-based pricing are lagging and can continue to experience upward pressure on cost of funds (see Figure 2 above).

Figure 3

Furthermore, time deposits tend to make up a larger share of a community-sized financial institution’s deposit composition. Time deposits have grown across all financial institutions over this recent rate cycle, but have grown most significantly across money centers (see Figure 3 above).

Figure 4

Usage of wholesale funding has varied by size of financial institutions (see figure 4). Most notably, all financial institutions have increased their usage of listing services as a funding source. However, both community and money center institutions have relied more heavily on the brokered market, whereas regional institutions have tapped the FHLB as a means for funding.

Figure 5

As financial institutions gear up for growing deposits, the era of loans outpacing deposits may be coming to an end, at least in the near term. During the first half of this year, loan growth has slowed at all financial institutional sizes. Both community and money center institutions have experienced marginal growth in deposits. This trend may reverse if the Fed does in fact cut rates, which should incentivize borrowing (see Figure 5 above).

In conclusion, the first half of 2019 has been marred with uncertainty, both at home and abroad. The continued signs of global economic slowdown have forced the central banks to change course on monetary policy in anticipation of navigating a potential crisis. Financial institutions are anxiously awaiting central bank outcomes as market-based rates have collapsed onto effective Fed Funds; continually whittling away at margin. Global economic growth and trade tensions will continue to be a headwind, thus directly facing financial institutions through the remainder of 2019.