Data is the key to unlocking a robust member experience. That’s because it enables CUs to learn deeply about members and predict and identify their next best needs. Doing this allows the credit union to demonstrate itself as a partner in their financial journey and conveniently position its products at just the right time.

To succeed with data, credit unions need a strategy to bring data together and use it to drive actionable insights. A well-designed data strategy with a CRM can help credit unions unlock significant value.

Challenges in the banking landscape

The banking industry has gone through a tremendous evolution in the past decade and is changing faster than many could have imagined.

Digitization now offers credit unions more data about their account holders, enabling them to offer new products and services and access new markets anywhere in the country. Growing competition has also influenced how credit unions operate, how they service members, and the types of products they offer.

Credit unions no longer only compete with banks and other credit unions—they now compete with tech companies. And it’s more important than ever to foster loyalty when more than one in three consumers say they are likely to switch banks or credit unions in the coming year.

Events of the past few years, and deteriorating economic conditions, have also led financial institutions to a new operating environment. As a result, many are now reconsidering their long-held strategies. While banks and credit unions have been accustomed to a near-zero rate environment for more than a decade, they are now near 20-year highs.

And while rising rates have generally been a profit driver, that doesn’t necessarily hold true in this environment. Current conditions are pressuring balance sheets and margins for many banks and credit unions, and they can no longer count on generating profits with minimal risk and effort.

Data: A key to unlocking loyalty and account growth

A bright spot in the current situation is that credit unions now have more access to data than ever before, offering insights to optimize operations, find new opportunities, and grow the member base.

However, many credit unions struggle to use this data. One problem is they typically have siloed systems, which leave information-sharing gaps across teams and departments. This makes it difficult to turn raw data into actionable analytics, making it difficult to capitalize on relationships quickly. Many credit unions also lack the talent and infrastructure to manage this data.

Some credit unions are looking to customer relationship management (CRM) tools as a solution. Yet, many of these systems fall short and fail to meet their needs. Big-box CRMs typically have a generic workflow and don’t offer sufficient customization. Additionally, the lack of vendor support leaves financial institutions with shiny new tools that don’t offer the expected return on investment.

Driving CRM with a data strategy

A CRM tool is only as good as the data strategy behind it. Rather than treating CRM as a technology-first, plug-and-play solution, Credit unions must start with a data strategy. This helps guide how to identify what data to use, how to manage it, and apply it to meet their stated goals.

Retailers have used customer data for nearly twenty years to drive loyalty and increase customer spend. Before the internet, retailers tracked consumer behaviors and preferences with loyalty programs and phone numbers at the point of sale. Most retailers now extensively harvest customer data to compete and make personalized recommendations.

However, credit unions have been relatively slow to catch on. While they diligently track member balances, assets, and financials, they haven’t always connected the dots to learn about behaviors and how to improve member experience.

Data can ultimately help credit unions optimize operations, improve the member experience, reduce risk, and increase profitability. A solid data strategy can help financial institutions reduce risk and weather the storm of rate hikes, paycheck-to-paycheck consumers, and rising auto loan defaults.

Triggers in the data can reveal warning signs or opportunities, enabling credit unions to take action. For example, a member who is having trouble paying their auto loan may show several clues in the data, such as a couple of recent late payments, disabling their auto pay, and a transaction at a payday lender. These insights may enable the CU to pre-empt a default by offering a skip-a-pay option.

Data insights can also help credit unions pitch a “next best offer,” such as a mortgage, lower interest rate card, auto loan, or savings account. As consumers now have more options and will quickly go elsewhere, credit unions cannot afford to spend weeks sifting through a spreadsheet to position offers.

There are several steps in formulating a data strategy:

- Identify the goals: The credit union should start by identifying the goals it would like to accomplish, such as growing the member base, increasing deposits, or writing more loans.

- Determine the data needs: Next, the CU needs to identify what data it needs to support these goals, including data sources and how to manage and obtain the data.

- Establish the structure and governance: Credit unions should then connect the needs to use cases and set up the tools and governance to ensure data quality. They should also identify who will use the data and how it will be accessed.

A platform for meaningful credit union insights

A CRM combined with a well-designed data strategy will enable a credit union to turn raw data into actionable insights with the click of a button.

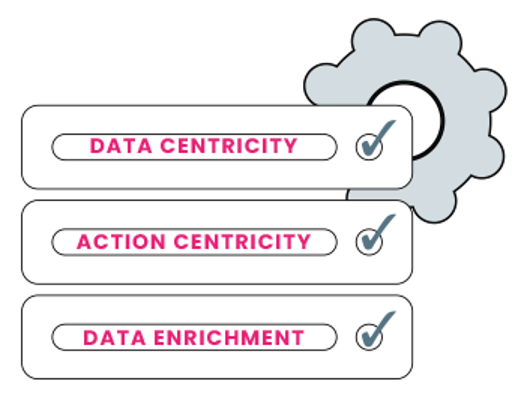

A CRM should offer several core capabilities, including the ability to put all data in one place (data centricity), the ability to assign workflows and actions into a single member data model (action centricity), and the ability to append data with informed aspects of the member (data enrichment).

CRMNEXT is a full stack, big data AI/ML platform that enables credit unions to gain actionable insights from data. It uses the power of data and AI/ML in real-time with real-world results. Eliminate siloes and information-sharing gaps and gain a single view across the entire system that can be accessed across all channels, including in the branches. See the ultimate credit union CRM in action. Watch an interactive demo today.