Among the emerging risks that The Rochdale Group monitors are geopolitical threats. These include things like last year’s worries over Russia’s annexation of the Crimea and its forays into Ukraine; the potential threat of a nuclear Iran; and the re-emergent fears over a Greek exit from the European Union (EU), which has been labeled the “Grexit.”

On February 4, the stock market reacted in sharply negative fashion to the Grexit threat. The Dow Jones Industrial Average was up more than 100 points within a half hour of the closing bell, before the European Central Bank (ECB) announced that it could no longer assume a successful outcome from the new Greek government’s bailout negotiations with its lenders, and thus it would no longer accept Greek debt as collateral for ECB loans. By the market’s close, the Dow had shed the day’s gains, dipping into negative territory before closing virtually flat on the day.

Following the closing bell, one market pundit posed the question, “Does Europe matter?” followed by her own reply: “Today’s market reaction proves it does.”

From a global risk perspective, Europe certainly matters, to its own nations, to the U.S. and to emerging markets. But the ECB announcement regarding Greek debt begs the more pertinent question: does Greece matter?

From our perspective, it does not. In spite of the recent election of an anti-austerity leader, we view the risk of a Grexit as less than in 2009, when the Greek crisis reached its zenith and the world’s economies were in a much more fragile state than they are today. And in the end, the new government is likely to capitulate after some re-negotiation of the austerity terms posed on Greece by the EU, for a very simple reason: Greece needs the EU more than the EU needs Greece.

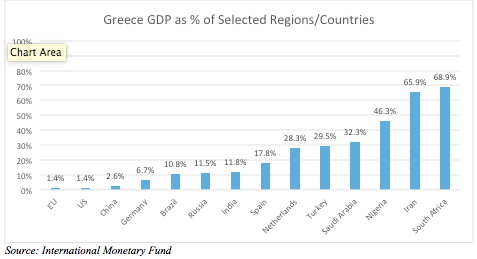

Figure 1 below depicts Greece’s GDP as a percent of selected other nations, as well as the EU. Greek GDP represents 1.4% of the aggregate GDP of the EU, according to the IMF. Clearly, Greece matters little to the EU. Its GDP is 6.7% of the EU’s largest member (Germany) and 17.8% of that of Spain, another beleaguered EU economy that has largely overcome its Great Recession struggles.

Does Greece matter to the U.S.? No. Its GDP is also about 1.4% of ours. Does it matter to the emerging markets – the so-called BRICs (Brazil, Russia, India and China)? Its GDP ranges from 6.7% to 11.8% of those countries’ – again, no. Greek GDP is less than that of relatively small countries like the Netherlands, Turkey, Nigeria, Iran and Saudi Arabia. Do we hear anyone claiming that the Netherlands “matters,” in terms of a global economic threat? No. If anything, given the recent plunge in oil prices, countries like Saudi Arabia, Iran and Nigeria matter more than Greece, given their dependence on oil and their larger total output.

If Greece were a U.S. state, it would rank 25th in terms of gross output. Among the states with higher output than Greece are Louisiana, Connecticut, Colorado, Indiana and Missouri. Arguably, those states matter more to the health of the U.S. and global economy than does Greece.

Figure 1 – Greek GDP as a Percent of Selected Countries and the EU

What about the risk to holders of Greek sovereign debt? The EU owns about 10% of Greece’s outstanding debt, spread across its 28 member nations. Greece’s public sector holds about 8%, while world governments hold about 7%. The IMF holds about 4%, and EU member central banks, in aggregate, hold less than 4%. The three largest non-Greek private bank holders of Greek debt own about another 4%. Even if Greece were to outright default on all its debt – an unlikely scenario – none of these owners of its debt would likely experience a catastrophic loss. A default would surely crush Greece’s own banking system, but that wouldn’t significantly worsen the scenario of a sovereign default, and it makes such a scenario all the less likely.

In short, while we love olives, ouzo and souvlakis, in terms of global risk, Greece doesn’t matter – in spite of what a jittery stock market may try to convince us. What does that mean to your credit union? In spite of the headlines or market reaction, a Grexit – even if it were to occur – would have minimal impact on the U.S. economy and interest rates. What happens here at home – the price of oil, the job growth trend, the strength of the dollar – will have far greater implications for the future path of interest rates, and for consumer trends, than what happens in Greece.