Wouldn’t it be fair to say that making decisions based on emotion can get you into trouble? You might make a purchase that you otherwise wouldn’t, after listening to a subtle car salesperson paint a picture of how you’ll feel behind the wheel of a new car. And while most people truly believe no salesperson is slick enough to sway their emotions into buying, you might be surprised to look back and see your decision was influenced by a seasoned and tactful sales veteran.

One of the reasons consultants are popular when a credit union is shopping for a new core system is because a third-party agency can quickly take the emotion out of play. They typically aren’t present during system demonstrations and have minimal interaction with the salespeople. Consultants level the playing field which sales reps often tip in their favor using emotion.

Does this mean that every credit union should bring in a consultant when shopping core? Absolutely not! Many credit unions aren’t flush with capital, ready to give a sizeable cut to the consulting agency after they negotiate a contract and price the credit union leadership likely would have been able to get. Consultants can also muddy the water, prolong the core review process and end up selecting a system that doesn’t fit your credit union’s culture.

Removing the emotion from a buying situation and making a decision logically can also be accomplished by looking at the numbers. Who hasn’t been to a sporting event where the losing team is talking trash only to hear an opponent or fan bark back, “Scoreboard! Scoreboard!” The numbers don’t lie. Actually, what numbers do, is tell a story. A story about what the credit union industry, as a whole, wants. You simply have to know how to read the story.

Here are 5 tips and key numbers to consider when shopping for a new core provider:

-

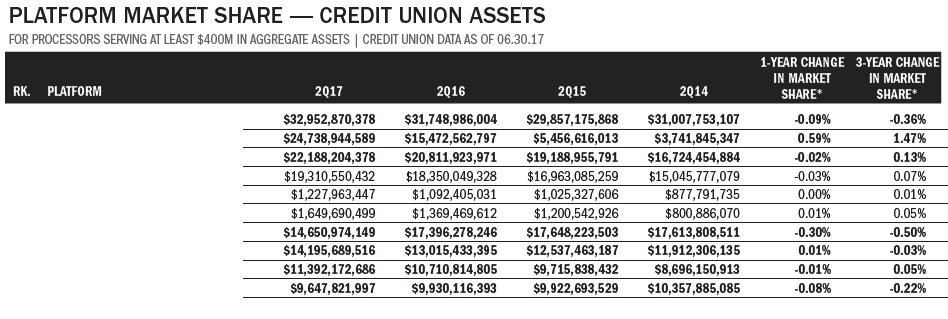

Define your peer group. The first thing a credit union should do when looking at data is define the numbers that matter to them. This is typically done by looking at an asset range (<$20M, $20M-$50M, $50-$100, $100M-$250M, $250-$500, $500M-$1B, etc) but it can also be measured by membership. The core system which credit unions over $1 billion in assets are using doesn’t apply to the credit union that has $55 million in assets. Consequently, when looking at the core market share data, don’t be fooled by a provider that boasts a large market share when their clients are mostly credit unions that aren’t similar to you in size.

*

* -

Some core providers have more than one platform. Breaking down the market share by platforms rather than core companies will shed light on some vendors strengths as well as weaknesses. Be aware of parent companies that have a strong foothold in the market when the platform they are pitching to you doesn’t.

*

-

Review growth and decline trends. It’s important to look at the total client base growth but don’t ignore the other metrics that indicate how healthy a core processor’s clients are. The credit union industry is a shrinking market. It’s possible to have a lower net customer count and still gain ground in overall market share. Also, consider the growth or decline in total assets as well as membership.

-

Sniff out the small players. Look at the total core processor market share of credit union clients over $20 million in assets.

*

You might be surprised to find that many of the leaders in total market share drop down the list because most of their customer base consists of small credit unions. Core processors with a large portion of their clients being smaller in asset size can be concerning. More than 200 mergers are approved by the NCUA every year and likely retain the core system of the larger surviving entity. If the core provider is losing clients to mergers, they may not have the capital to drive new development. Take a look at the numbers and asset ranges of the credit unions involved in recent mergers: -

Client performance. While there are too many factors that contribute to a credit unions success for failure, a core system can be one of the larger variables in play. Looking at the average client performance statistics, as well as the high and low, will give you a good idea of what is possible and common for credit unions leveraging that vendors technology.

*

At the end of the day, many buying decisions are based on a mixture of logic and emotion. The average buyer is sold on emotion and justifies the purchase/decision with “logic” that was provided by the salesperson. Don’t be average! Base your core system decision on logic and then confirm that decision with emotion.

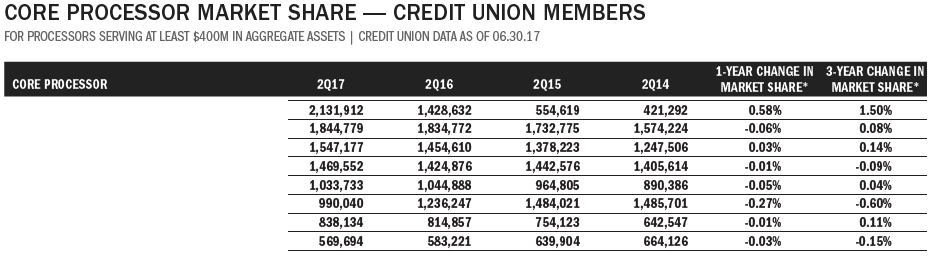

* These charts and graphs are the property of Callahan & Associates and their 2018 Supplier Market Share Guide of Credit Union Core Processors. The images have been edited to omit all core vendors names and rankings.