Since much of the country shut down to minimize the spread of COVID-19, businesses of all kinds have transitioned to “curbside delivery” as a way to keep their doors open and continue meeting consumer demand during the crisis.

Examples include restaurants offering takeout, breweries packaging their product in cans to-go, and brick-and-mortar retailers offering online ordering with contact-free pickup service. In fact, curbside pickup surged 208% between April 1st and 20th, as compared with the same time period a year prior[1].

But what does a “curbside delivery” service model for credit union members look like? In one example, as a response to the shutdown of school districts across Kentucky, Abound Credit Union shifted its VAULT financial education program to a fully online distance learning model, supporting teachers as they transitioned to non-traditional instruction[2]. Meanwhile, Affinity Plus FCU (St. Paul, MN) has begun offering car-side assistance, and representatives will even hand-deliver a new debit card to a member in need[3].

As conditions evolve, here are some key areas to consider on as you transition to a “curbside delivery” model:

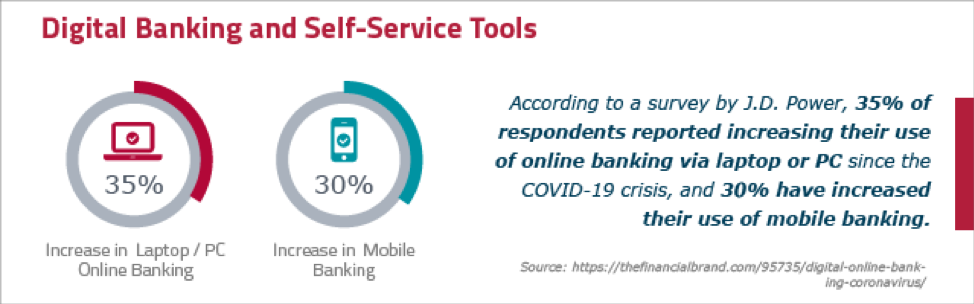

- Digital banking and self-service tools: As long as branches are closed to foot traffic, credit unions need to promote easy access to remote self-service delivery. Services like online and mobile banking, mobile check deposit, and online membership and loan applications are particularly important right now.

For some credit unions, a high tech/high touch approach is nothing new. Coastal FCU (Raleigh, NC) was an early adopter of video teller technology, and in fact, was one of the first financial institutions in the world to implement the service across its entire branch network! Today, the $3.4 billion cooperative serves 270,000 members across 23 branches in central North Carolina[4], and its widespread deployment of Personal Teller Machines beginning in the early 2000swas a key to that growth.

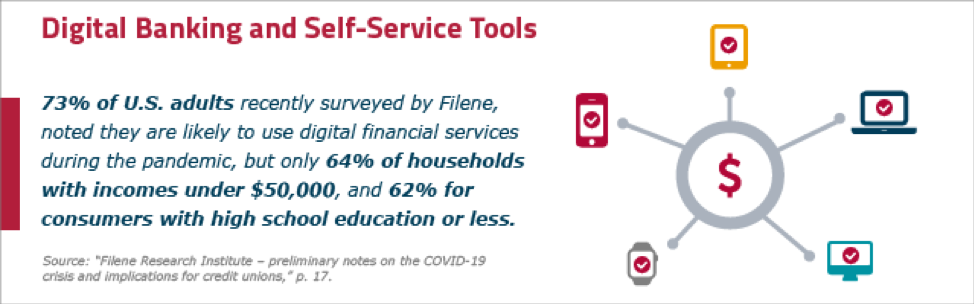

Of course, simply offering remote access technology is one thing. During a time of crisis, equitable access becomes even more critical.

To help ensure you’re reaching those most in need, it’s important to educate your members on how to use digital technology. Over three-quarters of financial institutions say they are providing additional education on the use of remote channels during the pandemic[5].

- Payments: As concerns increase around face-to-face commerce and hygiene during the pandemic, consumers are seeking out alternatives to paying with cash and physical cards. Fortunately, many options are available, including person-to-person (P2P) platforms, mobile wallets, registered prepaid cards and contactless payments.

To meet your members’ changing needs and expectations, now is the time to invest in and activate your digital payment strategy by offering a range of solutions, including contactless, P2P, prepaid, card controls and alerts and digital wallets.

- Branches: Pre-crisis, most consumers relied on multiple banking channels. According to a consumer study by Jefferies, nearly 75 percent of respondents visited physical branches at least once per month.[6]In the early weeks of the pandemic, some CUs across the country closed their branches to foot traffic, some leaving the drive-through as the only person-to-person point of access. Yet, many members still count on their branch even during these uncertain times. In fact, CO-OP Shared Branch transaction volume increased 20% on the day stimulus checks were announced.

As you consider reopening your branches, do it safely by following these protocols[7]:

-

- Increase janitorial services and do regular, deep cleaning every night.

- Maintain at least 6 feet of social distancing among employees and members. Some places of business are using painters tape to place markings six feet apart on the ground in areas where lines build up.

- Require all employees to wear gloves and masks. This goes for employees working in the drive-through, as well.

- Ensure you are regularly informing your members of the latest branch closings, re-openings and changes to service hours, as well as alternative ways to access credit union services. Post signage at all ATMs, branches and drive-through locations.

For those credit unions participating in CO-OP’s extensive Shared Branch network, remind your members they can easily locate a nearby branch using the CO-OP Shared Branch/ATM locator tool. (Note: Some Shared Branch locations may be temporarily unavailable. The Locator is frequently updated, but you may wish to contact the branch to confirm their status.)

- ATMs: Be sure your ATMs are cleaned regularly. The National ATM Council released a comprehensive set of guidelines for COVID-19 safety and spread prevention. Don’t forget to post signage at your branches and drive-thru ATMs to guest members notifying them of changes in your branch/ATM operations. And, if your credit union participates in the CO-OP ATM Network, remind your members to use the CO-OP Shared Branch/ATM locator tool to find an ATM near them. They can use the “Advanced Search” tab to find one of the 7,200+ ATMs that accept deposits or offer drive-through capabilities.

- Contact Centers: Expect call volumes to increase during this time. With many branches still closed to foot traffic and rising financial uncertainty, call centers are a critical lifeline for your members. If your agents have been displaced to remote facilities, ensure they’re being retrained to maintain the same level of service[8].

New Ways of Engagement

As businesses respond to the ongoing health and economic crisis, they are finding new ways to engage with their customers. By developing their own version of “curbside delivery”, credit unions can deliver peace of mind to their members while also driving engagement and loyalty - all of which goes a long way towards becoming your members’ Primary Financial Relationship.

If and when you need it, CO-OP has you covered with an ecosystem of products and services designed to help you own more member moments. Learn more.

[1] “Curbside pickup at retail stores surges 208% during coronavirus pandemic,” by Lauren Thomas, CNBC, April 27, 2020. https://www.cnbc.com/2020/04/27/coronavirus-curbside-pickup-at-retail-stores-surges-208percent.html

[2] “Financial literacy program moves to teaching online,” The News-Enterprise, May 5, 2020. https://www.thenewsenterprise.com/news/business/financial-literacy-program-moves-to-teaching-online/article_a3395d7f-a1c7-598d-9028-c2075449c887.html

[3] Affinity Plus Federal Credit Union. https://www.affinityplus.org/covid-19

[4] https://www.coastal24.com/CoastalCreditUnion/media/PDFs/Annual-Reports/2020-Member-and-Community-Impact-Report.pdf

[5] “Filene Research Institute – preliminary notes on the COVID-19 crisis and implications for credit unions,” p. 17.

[6]“Despite the rise of online banks, millennials are still visiting branches.” By Kate Rooney, CNBC, December 5, 2019. https://www.cnbc.com/2019/12/05/despite-the-rise-of-online-banks-millennials-still-go-to-branches.html

[7] “COVID 19 Best Practices” https://view.ceros.com/co-op/covid19-best-practices/p/2

[8] “CO-OP Moved Quickly as Calls Surged,” CUToday, May 3, 2020. http://www.cutoday.info/THE-boost/CO-OP-Moved-Quickly-As-Calls-Surged