Consolidation, taxation and concentration in top credit union systems worldwide

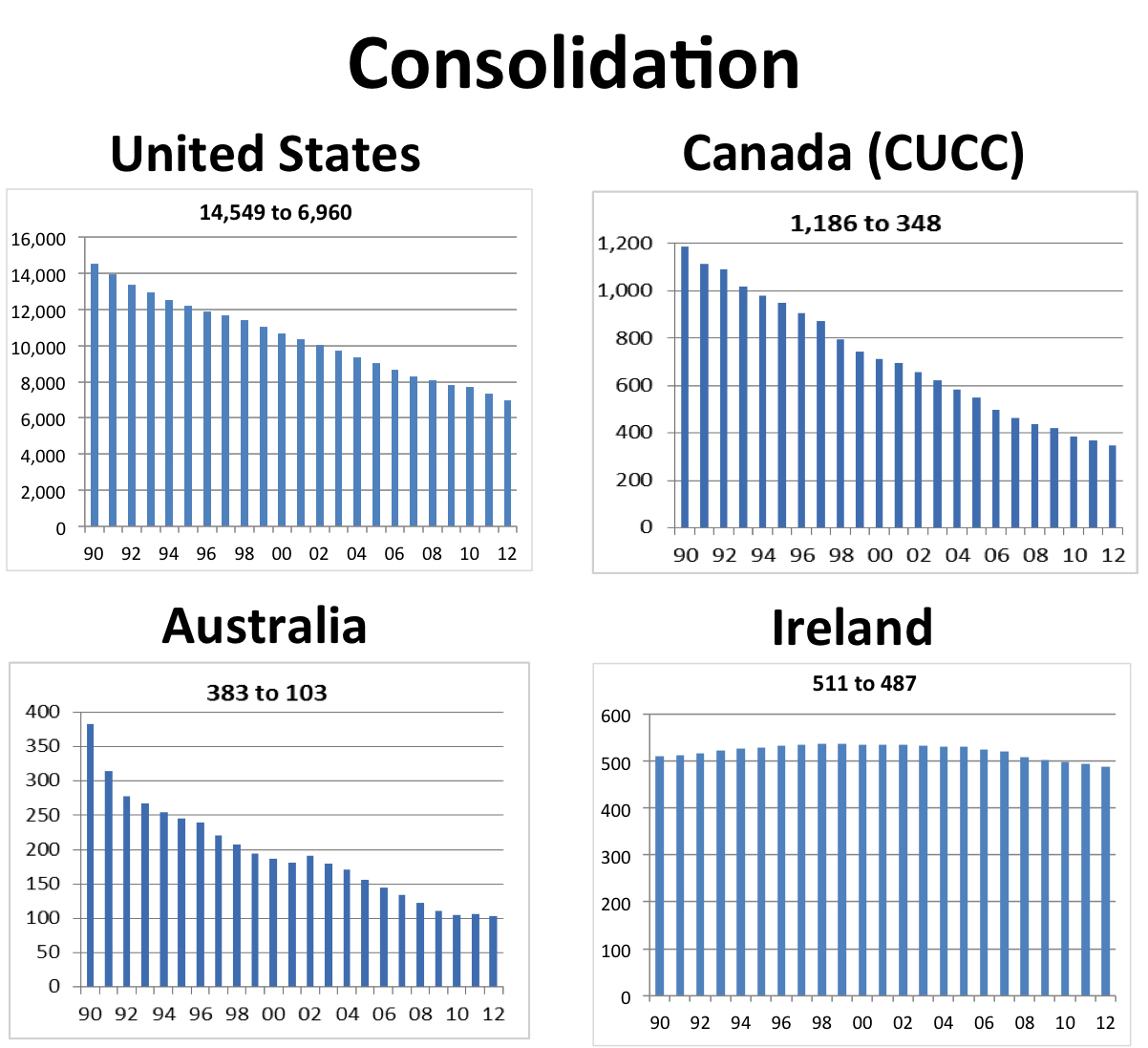

Consolidation. What drives this? What will the future look like? Where will this end? The United States, Canada and Australia have exhibited decreasing numbers of credit unions for years as the small ones merge into medium or large credit unions. At the end of 2012, there were 6,960 credit unions in the U.S., 348 credit unions in the Anglophone Canadian system, 103 mutuals in Australia and 487 credit unions in Ireland. The consolidation trend is now common across other countries around the world.

Consolidation is driven by increasing regulatory burden, technology investment, specialized personnel requirements and CEO retirement. Smaller credit unions remain robust where common bond niche groups are loyal and sponsor industries are strong. They remain robust where support services are available from leagues, centrals, national associations and credit union owned service organizations and where the regulator attitude toward small credit unions is proportional regulatory burden.

Consolidation leads to concentration. We divide credit unions into assets size peer groups: very small ($5 million), small ($5–$20 million), medium ($20–$100 million), large ($100–$500 million) and very large (<$500 million).

The U.S. has the largest percentage (22%) of remaining very small credit unions. In Canada, there are only 5% of the very small credit unions left, and in Australia fewer still: only 2% of the total number. In Ireland, 10% are in the very small group. Conversely, the number of large credit unions in the U.S. is still relatively low at 6% of the total number of credit unions. Australia has the largest share of very large credit unions (32%) followed by Canada (15%). Australia shows the highest degree of concentration, followed by Canada, then U.S. and lastly Ireland.

What differences might explain why such otherwise similar systems show such differences in concentration? While regulatory burden and technology costs drive merger consolidation everywhere, the degree of concentration of credit union systems into large size groups is also driven by universal regulatory application and taxation. With the U.S. tax exemption and specialized credit union regulator, U.S. credit unions have shown a gradual trend toward concentration while, with full corporate taxation and universal application of banking regulation, Australian credit unions have shown accelerated concentration. With small business rates, which are lower than full corporate taxation rates, and with provincial credit union regulation, Canadian credit unions have shown concentration trends somewhere in between those of U.S. and Australia. With the credit union tax increasing to the full corporate rate, the trend toward concentration is predicted to increase in Canada.

It is not all about external pressures. There are efficiencies in scale. Return on assets is highest for the largest credit unions. Larger credit union groups have higher levels of non-interest and fee income in the low interest rate environment, whereas the smaller credit unions continue to rely largely on interest income. The largest credit unions also account for most of membership growth. Members join those credit unions that offer the complete range of products as well as the convenience channels that members demand, particularly online and mobile access.

Is merging the only outcome to the challenge of small credit union sustainability? No. Next, let’s look at the collaboration approaches that countries take to allow their credit unions, small and large, to share platforms and offer the full range of products that consumers demand.