Ease of use combined with the declining expense of many BA/BI packages is reducing the hurdles for purchasing a data analytics platform. These platforms provide the foundation for improved 1:1 marketing, reducing service delivery costs, and improvement of the overall member experience. So why is adoption of this functionality lagging?

It would seem a natural progression that credit unions begin making use of the large amount of data they have on-hand to improve the overall experience of their members. This data includes member demographics, the products and services they utilize and account balances and transaction histories. And if there is data you need but don’t have in-house you can purchase additional demographic and financial information from third parties that include wealth, income, family characteristics, and much more. If this is the case - why aren’t more jumping on the BA/BI bandwagon?

The short answer is: it’s not that simple. Research within the past year looked at the usage of analytic platforms by community banks and credit unions. The results of the survey revealed that only 20% of those financial institutions surveyed still have a workable BA/BI platform after 3 years. That doesn’t seem possible, but many credit unions and community banks jump into big data analytics without doing their homework. The changes analytics can bring to your organization are fundamental and possibly disruptive, if you’re not ready for the true impact this change will cause.

Integrating data analytics into your workflow is much more than just understanding the mechanics of the analytics themselves. It is the promise to improve your ability to offer the right product, to the right person, at the right time, on the right device, with the right price/offer. This new capability creates profound changes on your credit union’s organization and culture. There are several areas where implementing a big data analytics program might cause some “growing pains” at your institution. These growing pains manifest themselves in the changing of roles and responsibilities of manager within your organization.

When implementing a data analytics strategy the first critical step is to get all management stakeholders at the same table and then get them to agree on goals for this project. This will require everyone within the organization to recognize the business need for analytics in their own respective areas of responsibility. For example, Human Resources with the benefits of analytics can improve hiring practices, and provide insights that can help them manage people more effectively and efficiently throughout the branch system.

Marketing information at many credit unions has historically been antidotal, with the top branch personnel and the CEO articulating the organization’s “best members.” With even the introduction of a simple analytics function, marketing evolves from an events and promotions department into a strong sales support and possibly even a direct sales group. This begins to happen with the marketing department’s new ability to match customer behaviors with identifying demographics. This means the rest of the organization looks to the marketing department to answer questions like; which customer segment is the most profitable? Who should we be cross-selling? What product should we offer? What are the best types of new customers to go after? What product should we be selling them?

So in essence, marketing is now driving branch sales by being able to identify new customer and cross-sell segments, as well as, the product, pricing and messaging for these sales campaigns. And if that isn’t enough, marketing can also articulate the goals for these sales campaigns. It seems that branch personnel are now accountable not only through their branch management, but to the marketing department as well. Other departmental relationships within the organization will also continue to evolve; for example IT and Marketing will now compete for technology budgets and priorities.

These are all significant and for the most part unforeseen consequences of your credit union instituting a marketing analytics strategy. For those of you who can conquer the organizational hurdles of implementing a data strategy, the competitive advantages are significant. From recent studies almost 75% of credit unions and community banks do not have a data analytics strategy, by being able to do so, you can achieve a significant competitive advantage.

The part that isn’t really articulated here is the change that will be happening to your bank’s organization and culture as you introduce these new customer insights and responsibilities to your management team. At many analytics conferences the common theme is that analytics software alone will not change your credit union’s culture – management changes the culture and then the purchase of an analytics solution supports and grows that new culture. What we are doing here is educating your senior managers on the advantages of data analytics and now they are driving the implementation of your new capabilities.

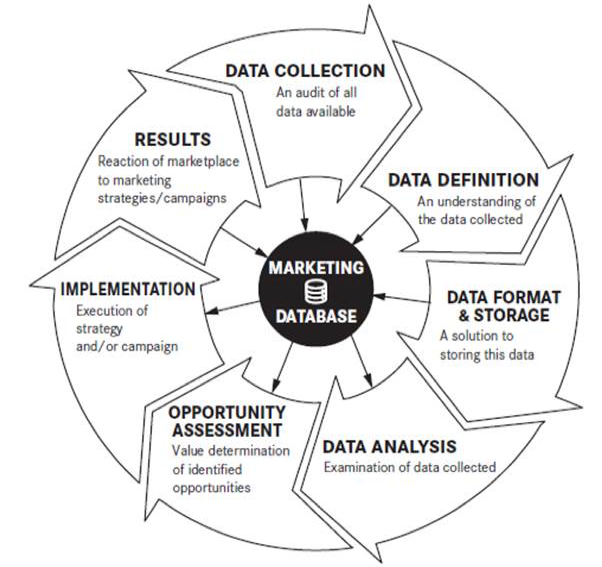

There is a template that has been used effectively and it is articulated in a new book called “The New Marketing Analytics.” The book is structured around the steps in what it calls the “Analytics Roadmap.” It is a high level step by step guide for senior marketers and/or their CEOs for implementing a data analytics platform. An over view of the Data Analytics Roadmap is below:

New Marketing Analytics Roadmap

The process starts out with identifying all sources of data throughout the credit union. Data exists everywhere; make sure you review this project with all departments that interact with members. Once all of your sources have been identified categorized and then a relative value assigned to each of them, the data needs to be warehoused. Most credit union customer files are relatively small so this is not a significant IT issue.

As the data is analyzed and reviewed by stakeholders, who most likely include senior management, customer service, sales and marketing - possible projects are listed and discussed. This list is then reviewed and prioritized by revenue and non-revenue factors. All projects have expenses and potential revenues attached and are incorporated into departmental budgets.

A critical point to the success of the entire data analytics project is to incorporate all campaign results back into your data. This will identify what is working and will drive the process of continuous improvement. Once this happens the process has completed one cycle and is ready to begin again.

It is possible for credit unions to launch into more sophisticated data driven marketing. However, to be successful, it takes a strong commitment by management and a willingness to evolve the organization to more closely align with this new technology. It is however, just as important for management to remember our roots and the original charter for credit unions when implementing a new analytics platform. A core objective for this new functionality must be to improve service to the underserved by creating more relevant products and reducing the cost of service delivery.