When it comes to supporting the latest payment forms on behalf of members, credit unions have several new options – each of which comes with its own set of challenges. Decades-old technology like checks, wire transfers and ACH are now working beside Visa Direct and Mastercard Send™ push payments. Every member with a smartphone has access to Venmo and some have access to Zelle. The Clearing House launched RTP®, a new real-time payment system, a little over two years ago. And even more recently, The Federal Reserve Bank announced it is developing a new service called FedNow that will allow all financial institutions in the U.S. to offer 24/7 real-time payment services as early as 2023 or 2024. Given all of these developments, what should a credit union do? The solution lies in what use cases the credit union is looking to satisfy.

The Meaning of “Faster Payments”

Credit and debit card transactions show up on a cardholder’s account as soon as the transaction is made, giving the appearance that transactions are occurring in real time. The actual settlement – or the movement of funds from the cardholder’s financial institution to that of the payee – actually takes place later. Settlement of ACH transactions, which includes bill pay and payments made using an account and routing number, can occur on the same day as the transaction is requested, sometimes within hours. These various payment “rails” suffice for most use cases today.

There is a growing need, however, for payments to take place even faster, with the settlement of funds occurring in seconds and minutes versus hours and days. Furthermore, ACH settlement only occurs on business days – and this is not fast enough for everyone. For example, businesses that need to move funds to a vendor, gig workers who need their paychecks, insurance customers getting a disbursement or two parties conducting a real estate transaction do not want to wait.

There are many different terms for “faster payments,” including faster, immediate, instant and real-time. Instant payments is the most accurate description of real-time messaging and settlement. This new payments method allows for the transmission of the payment message and the availability of “final” funds to the payee in real time or near-real time, on or close to a 24/7 basis.

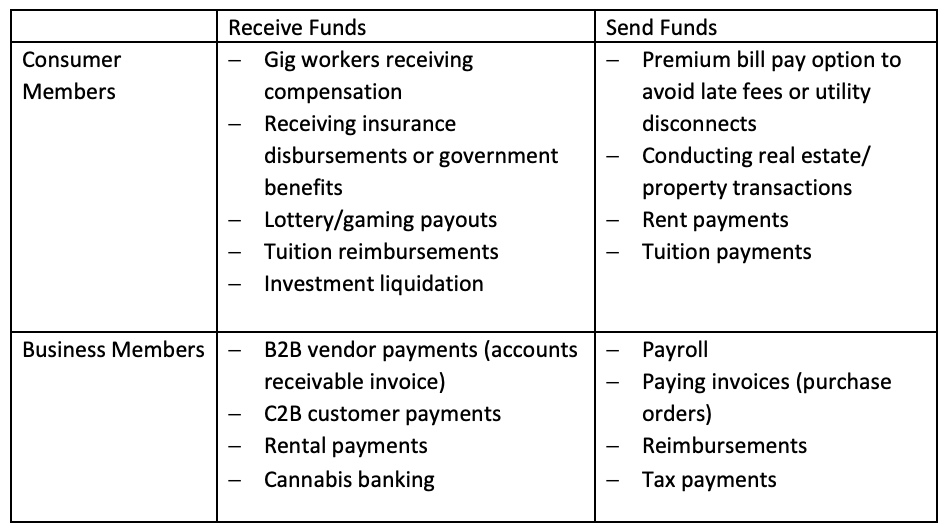

Use Cases for Instant Payments

There are two categories of potential use cases for instant payments: consumer and business, each of which have capabilities to receive funds (the minimum functionality) and send funds (origination). Here are a few examples:

For businesses, it is expected that disbursements will comprise the largest volume of transactions, especially for the insurance and mortgage industries. For consumers, last-minute bill pay activity, such as paying rent and utilities, is generally viewed as a driver for a credit union to offer faster payments to its members. Additionally, any use case that currently involves wire transfer, a manual and time-consuming service which is only available when the credit union is open, can easily be usurped by faster payments.

Next Steps for Credit Unions

Collaboration, something the industry is known for, is key as credit unions begin to explore faster payments and how it fits into their business and operating models. Conduct joint ideation with peer credit unions to determine what plans are being made or if any customer journey for faster payments has been mapped. Begin looking into requirements for technical integration and operational necessities. Leverage the resources, experience and scale of a trusted CUSO partner as you start establishing your real-time payments strategy. Educate yourself by attending webinars and other virtual events, reading white papers and articles from reputable sources like the U.S. Faster Payments Council, and follow the news about FedNow as it develops.

The continuous growth rate of ACH, Zelle and real-time payments commercial transactions indicates there is an increasing appetite and market for faster payments. Credit unions should consider the needs of their members, both consumer and business, to determine when and how they will participate.