Small credit unions continue to get gobbled up. Much has been written recently about this and the ongoing decline in the number of credit unions. Credit unions with assets less than $50M decreased by 229 to 2,582 over the past year and the trend is continuing. While these institutions face well-known significant headwinds, what is at the root of the struggle? In a word – relevancy.

Small credit unions are overall, well-capitalized but struggle to engage with and grow members and hence, eventually become irrelevant. What can be done to help small credit unions survive and thrive? Change the focus to member-facing growth initiatives, spend less time on back-office non-member facing tasks. More importantly, directors and management need to address some tough questions. This will require change but change that is necessary.

Let’s look quickly at what the data shows and then what can be done so small credit unions can survive and thrive.

What does the data show?

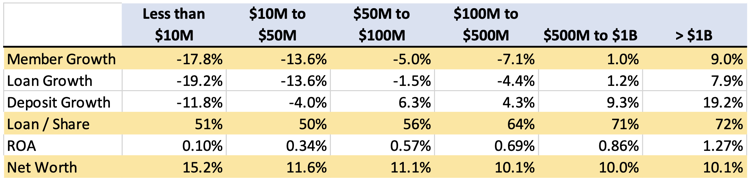

Year-over-year growth metrics for credit unions by asset size and other key ratios as of June 2021 are telling:

While the growth ratios are impacted by the shrinking number of smaller credit unions, they are very well-capitalized. They hold far more capital than larger credit unions as a percentage and far more than the “well-capitalized” threshold of 7%. Yet they do not generate the growth necessary to be relevant and grow in a financially sustainable manner.

What are the headwinds?

It is no secret the headwinds that face small credit unions:

- Regulations and compliance

- Resources to support member-focused growth initiatives

- Economies of scale

Precious time and resources spent on areas that do not help improve the relevancy of an institution leads to more mergers and the elimination of small institutions.

What can be done to become more relevant?

Strategizing and focusing on building relationships with our members and meeting their needs is of primary importance. Accomplish this in key areas:

- Loan production: Increasing loan production to generate earnings is a by-product of helping our members. Examine loan product penetrations and the credit risk within the portfolio. Focus on increasing loan product penetrations and consider taking additional risk by loaning to lower credit tiers. Higher risk usually means higher rewards. This will generate higher yields and your members may be married to your credit union for life for helping them in a time of need. Increasing the loan to share ratio by 10% for a $50M credit union can add .15%-.20% to ROA.

- Non-interest income: Likewise, increasing non-interest income to generate earnings is also a by-product of helping our members. Debit and credit cards, loan insurance products and checking related revenue are only some of the obvious examples that members need and can use. What your credit union has to offer is probably a better deal than your competitors. Pick one and focus on growing that product usage. Non-interest income reduces your dependance on the balance sheet for earnings and financial stability.

- Member growth: Not growing members is a death sentence. New members added today will provide the strong product usage the credit union will need in the future. Your existing members can only provide so much, and their needs will evolve and change over time. Replace this evolving need with new members. Focus on farming select employer groups (SEGs) for SEG based credit unions. Community credit unions need to be an integral part of the communities in which they operate.

Execution

If you agree with this so far, good! If you can’t execute, not so good. In the book, The 4 Disciplines of Execution, authors Covey, McChesney and Huling describe that the real enemy of execution is your day job. Referred to as the “whirlwind”, this is the massive amount of energy that’s necessary to keep your operation going on a day-to-day basis. It’s also the thing that makes it so hard to execute anything new. Discipline number 1 is to select one, maybe two extremely important goals to execute, instead of trying to improve everything all at once. They call these “wildly important goals”. The other disciplines are act on lead measure, keep a compelling scoreboard and accountability.¹

Change

Change is never easy. Stepping out of our comfort zones is never easy. Human nature is to revert back to doing what we are comfortable with. But if small credit unions are to survive and thrive, it will require directors and leaders to grow and execute on these core initiatives.

Directors, ask yourselves:

- Do you have the education and exposure you need to ensure you are meeting your fiduciary responsibility to represent your members?

- Have you worked with management to develop a clear, concise strategic plan that identifies the “wildly important goals” that will keep your credit union relevant? (Less is more).

- Are you supporting management and holding them accountable on achieving the strategic plan and monitoring a compelling scoreboard?

Management, ask yourselves:

- How much time are you spending in the “whirlwind” as opposed to the “wildly important goals”?

- Do you need to step out of your comfort zone and get the support you need to execute on the “wildly important goals"? (Help is available.)

- Are you differentiating your credit union by providing your members exceptional service?

None of this is rocket science. But face these challenging questions and do some rethinking. Help is available. For starters, reach out to Aux for non-member facing tasks: compliance, data analytics, and accounting and CFO consulting services. Smaller credit unions can survive and thrive and be an important part of the members and communities they serve.

¹The 4 Disciplines of Execution, Chris McChesney, Sean Covey, Jim Huling; 2012 FranklinCovey Co.